Centurion Corporation Limited provides purpose-built workers and student accommodation services. Centurion owns, develops, and manages quality and purpose-built workers accommodation assets. Centurion serves customers worldwide.

Expanding global footprint. As of 31 March 2025, Centurion operated 69,929 beds across 37 assets with AUM of S$2.6 billion. Revenue from PBWAs rose 15% to S$53.4 million, while PBSAs grew modestly by 2% to S$15 million. The group’s new Build-to-Rent asset in China began operations, with occupancy at 48% and expected to increase. Centurion is actively expanding its footprint, with dormitory redevelopments in Singapore and Malaysia, and PBSA developments underway in Australia. Despite occupancy softness in Malaysia and Australia, the company remains confident in sustaining performance through strategic management of rental rates and occupancy.

REIT listing exploration. Centurion is exploring a potential REIT structure comprising stabilized PBWA and PBSA assets in mature markets like Singapore, Malaysia, and the UK. This could unlock asset value, enhance capital recycling, and deliver stable income for shareholders via a potential dividend-in-specie.

1Q25 results review. Revenue increased 13% YoY to S$69.0 million from S$61.1 million in 1Q24, attributable to higher contributions from positive rental revisions across all PBSAs and PBWAs and strong financial occupancies in both Singapore and the United Kingdom, partially offset by lower occupancy in Malaysia and Australia assets.

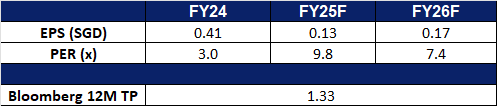

We have fundamental coverage with a BUY recommendation and a TP of S$1.38. Please read the full report here.

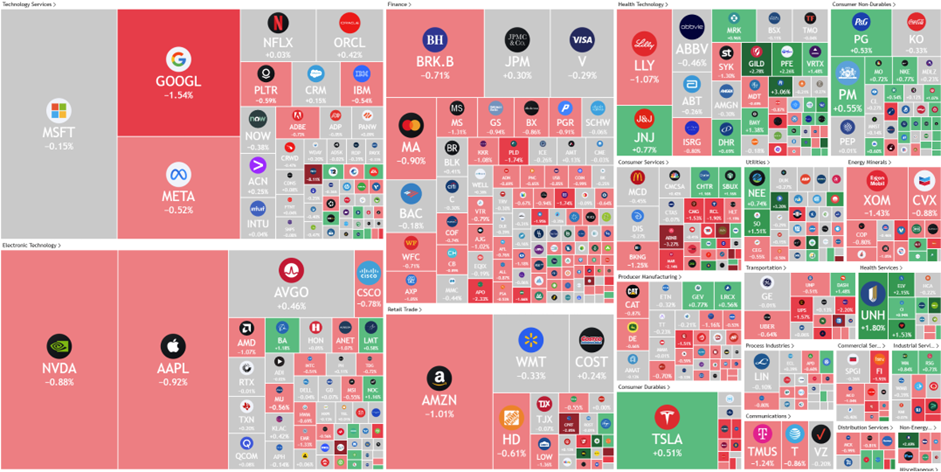

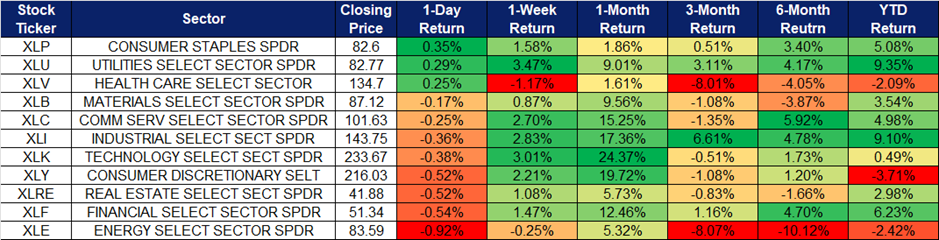

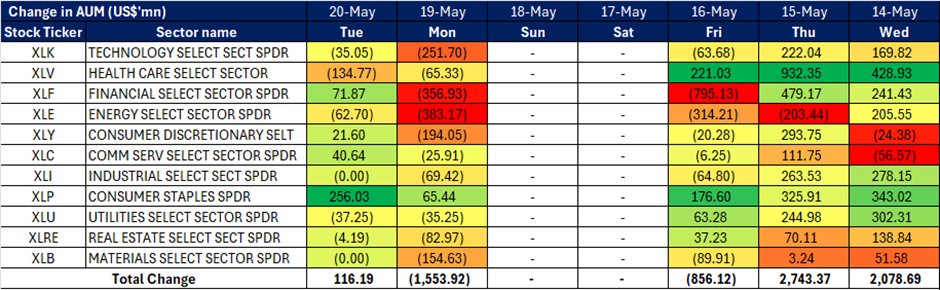

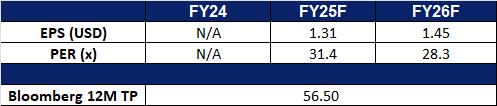

Market consensus

(Source: Bloomberg)

ISOTeam Ltd (ISO SP): Leveraging public sector demand and sustainability tailwinds

ISOTeam Ltd. is a building maintenance and estate upgrading company experienced in implementing eco-driven solutions through R&R and A&A services to the public and private sector. The Company has extensive experience in upgrading, retrofitting and maintenance of buildings and facilities in Singapore, and reshapes and rejuvenates public housing landscape, amenities, and environment.

Robust and diversified order book. As of February 2025, ISOTeam’s outstanding order book stood at S$188.7mn, providing clear revenue visibility through FY29. The Group is well positioned to capture recurring demand from upgrading, sustainability retrofits, and infrastructure enhancement projects.

Technology driven productivity gains. ISOTeam is on track to commercialise autonomous facade cleaning and painting drones by end-2025 via ISOTeam BuildTech. With 18 drones targeted and Civil Aviation Authority of Singapore (CAAS) permits pending, this first-mover advantage is set to enhance efficiency and reduce labour reliance in maintenance works.

Structural tailwinds underpin multi-year growth visibility. ISOTeam is well-positioned to capitalise on Singapore’s sustained public sector upgrading and green initiatives. Its core Repairs & Redecoration (R&R) and Addition & Alteration (A&A) services align with recurring programmes like the Home Improvement Programme (HIP), Neighbourhood Renewal Programme (NRP) and the planned launch of over 50,000 BTO flats from 2025-2027. These works, typically recurring every five to ten years, underpin long-term revenue visibility. ISOTeam has also expanded into sustainability-linked projects, such as solar installations with Singapore’s 2 GWp by 2030 target. Its Coating & Painting (C&P) segment also supports HDB initiatives to mitigate the Urban Heat Island (UHI) effect through heat-reflective coatings. The Group’s early adoption of robotics, drones, and AI-powered painting solutions enhances productivity and mitigates labour constraints. Backed by its robust order book, ISOTeam offers clear earnings visibility and sustained multiyear growth potential.

1H25 financial results. ISOTeam delivered a strong performance in 1H25, with revenue rising by 4.2% YoY to S$65.4mn, up from S$62.7mn in 1H24. This growth was driven by higher contributions from its Addition & Alteration (A&A) segment, which saw a 61.6% YoY jump in revenue to S$30.3mn in 1H25, up from S$18.7mn in 1H24. Gross profit rose 18.4% YoY to S$9.9mn in 1H25, reflecting improved margins from projects secured post-COVID-19. Additionally, the company reported a net profit attributable to shareholders of S$1.9mn, a 36.5% increase compared to S$1.4mn in 1H24.

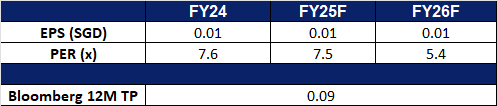

We have fundamental coverage with a BUY recommendation and a TP of S$0.100. Please read the full report here.

BYD Co Ltd is a China-based company mainly engaged in the manufacture and sales of transportation equipment. The Company’s main businesses include automobile business mainly based on new energy vehicles, mobile phone components and assembly business, secondary rechargeable batteries and photovoltaic business. The Company’s passenger car brands include two major series of products, ‘Dynasty’ and ‘Ocean’. The Company conducts its business in the domestic market and overseas markets.

Expansion in the European market. BYD has announced plans to establish its European headquarters in Hungary, reinforcing its commitment to expanding in the region. As part of a strategic cooperation agreement signed with the Hungarian government on May 15, the company will relocate its European base from the Netherlands to Hungary. BYD will invest HUF 100 billion (€250 million) to set up a business and development centre in Budapest, with the Hungarian government contributing a HUF 20 billion grant. The initiative will launch with two key projects: one focused on integrating intelligent technologies into modern mobility solutions, and another aimed at advancing next-generation electromobility technologies. This move underscores BYD’s ongoing efforts to strengthen its presence in the European market.

Increasing popularity of BYD cars. BYD has recently achieved notable sales growth across multiple international markets, emerging as a top-selling brand in several countries. In Singapore, BYD became the best-selling car brand in early 2025, overtaking Toyota for the first time, according to government data—highlighting its growing appeal as a leading electric vehicle (EV) manufacturer. In April 2025, BYD also outperformed Tesla in key European markets, including Spain, Italy, France, the UK, and Germany. Across 14 European countries, BYD recorded sales of 11,123 units, significantly ahead of Tesla’s 6,253 units. In Australia, the BYD Sealion 7 surpassed the Tesla Model Y to become the country’s best-selling electric vehicle. This growing international market share underscores BYD’s rising popularity among consumers and reflects its successful strategy to accelerate global expansion in the EV segment.

Launch of the new BYD e7. BYD is set to officially launch its new all-electric sedan, the e7, this Saturday, targeting the shared mobility and taxi service market. Designed with commercial use in mind, the e7 features a long 2,820 mm wheelbase and a 100 kW (134 hp) electric motor, offering a top speed of 150 km/h. The vehicle will be available with two battery options—48 kWh and 57.6 kWh—providing CLTC ranges of up to 450 km and 520 km, respectively. With its spacious design and practical range, the BYD e7 is expected to attract strong demand from corporate and fleet customers, further supporting the company’s growth in the commercial EV segment.

1Q25 earnings. Operatingrevenue rose by 36.4% YoY to RMB170.4bn in 1Q25, compared to RMB124.9bn in 1Q24. Profit attributable to equity shareholders was RMB9.15bn in 1Q25, up by 100.4% YoY from RMB4.57bn in 1Q24. Basic earnings per share was RMB3.12 in 1Q25, compared to a basic earnings per share of RMB1.57 in 1Q24.

China Mobile Ltd is a company mainly engaged in the provision of communication and information services. The Company’s businesses include customer market business, home market business, business market business and new market business. The customer market business mainly provides fifth-generation mobile communication technology (5G) mobile services and brand differentiated service operations. The home market business mainly provides home wired broadband services, mobile housekeeping smart services and smart home value-added services. The business market business is engaged in the research and development and sales of cloud computers and Internet of Things card services. The new market business includes international business, equity investment, digital content and financial technology.

AI integration. Earlier this year, China Mobile, along with other major Chinese telecom companies, announced the integration of DeepSeek’s artificial intelligence (AI) models into their services and products. The move follows a broader trend among the country’s top tech firms, including Alibaba Group, Tencent Holdings and Baidu Inc, which have ramped up support for DeepSeek’s latest AI models on their respective platforms. While these telecom giants have been developing their own large language models (LLMs) over the past two years amid a global AI boom spurred by OpenAI, they primarily leverage DeepSeek’s models for cloud-based applications. China Mobile, in particular, has incorporated DeepSeek’s full suite of models—from DeepSeek-V1 to the latest DeepSeek-R1—into its computing platform. This enables businesses of all sizes to access the models, deploy application programming interfaces (APIs), and build new AI agents on its platform.

Growth in smart devices and 5G adoption. China’s mobile phone market experienced robust growth in 2024, with total shipments increasing by 8.7% to 314 million units. Notably, December 2024 saw a significant YoY surge of 22.1%, reaching 34.53 million units. 5G smartphones dominated the market, accounting for 88.1% of December shipments and 86.6% of total annual shipments. This trend is supported by China’s rapidly expanding 5G infrastructure, which now includes over 4.25 million 5G base stations and serves more than 1 billion 5G users. The rise in smart device adoption, particularly 5G-enabled phones, is expected to drive an expansion of China Mobile’s customer base, as more users seek high-speed connectivity and advanced mobile services.

Strategic cooperation agreement to deepen AI development. China Mobile recently announced a strategic cooperation agreement with Chengdu City to deepen collaboration across multiple sectors. Under this agreement, the two parties will enhance infrastructure development in AI, 5G-A, and next-generation networks, drive technological innovation and commercialization, and strengthen partnerships in areas such as supply chains, industrial investment, and intelligent hardware. They will also explore opportunities in smart cities, the data industry, 5G-powered industrial internet applications, and the low-altitude economy, fostering high-quality growth in Chengdu’s electronic information and audio-entertainment industries. This initiative is expected to further position China Mobile to capitalize on China’s expanding AI landscape.

9M24 earnings. Revenue rose by 2.0% YoY to RMB791.5bn in 9M24, compared to RMB775.6bn in 9M23. Profit attributable to equity shareholders was RMB110.9bn, up by 5.1% YoY from RMB105.5bn. Basic earnings per share was RMB5.18 in 9M24, compared to a basic earnings per share of RMB4.94 in 9M23.

RELX PLC is a global provider of information and analytics for professional and business customers across industries. The Group serves customers in more than 180 countries and has offices in about 40 countries.

AI-driven product innovation. Relx actively integrates artificial intelligence into its product lines, such as Elsevier’s ScienceDirect AI, which can quickly summarize millions of research articles, and Lexis+AI, which assists legal professionals with case summarization and document drafting, enhancing user efficiency.

Stable subscription revenue model. Approximately 54% of the company’s revenue comes from subscription services, covering fields such as academic publishing, legal information, and risk analytics, providing stable cash flow and a profit margin of up to 34%. The Legal and Science, Technical, and Medical (STM) divisions contribute over half of the group’s revenue, with only around 20% and 25% of revenue from one-time transactions in these divisions, respectively, while the remainder comes from long-term contracts or subscriptions.

Active stock buybacks. The company spent £1 billion on share buybacks in 2024 and plans to increase this to £1.5 billion in 2025.

FY24 results. Revenue rose 7% YoY to £9,434mn from £9,161mn in FY23. Adjusted EPS increased 5% to 120.1p (9% growth in constant currency) from 114.0p. RELX declared a semi-annual dividend of $0.5586 per share, payable on 25 June to shareholders of record as of 9 May. The company also announced a £1.5bn share buyback for 2025, exceeding market expectations, which ranged between £1.05bn and £1.4bn.

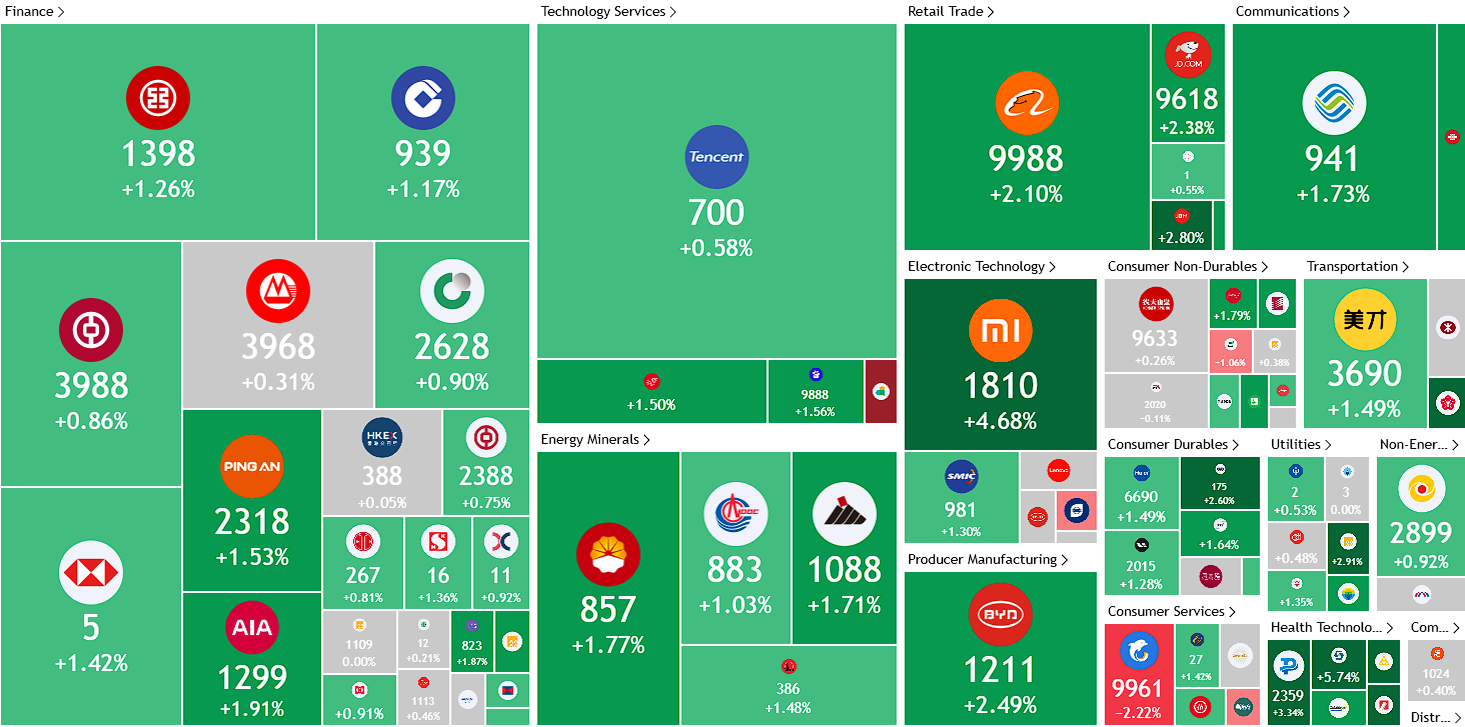

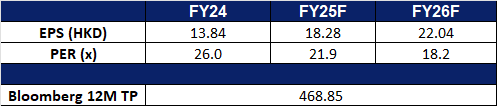

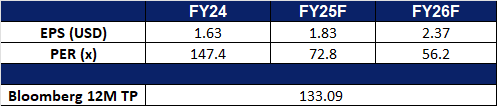

Market consensus

(Source: Bloomberg)

Arm Holdings PLC. (ARM US): Benefitting from a big deal

ARM Holdings PLC operates as a holding company. The Company, through its subsidiaries, designs and manufactures semiconductor technology and other related products such as computer processors, memory controllers, internet protocol system, graphic processor, security, and storage devices. ARM Holdings serves automotive, infrastructure, and consumer technologies markets worldwide.

Tailwinds of accelerating AI demand. Arm is central to the AI and cloud computing revolution, with its energy-efficient architecture gaining adoption among hyperscalers like Google and Microsoft. By 2025, nearly half of all new server chips are expected to be Arm-based, underscoring its growing role in data centers, edge AI, and automotive systems. The recent US$600bn deal, announced during President Trump’s Middle East visit, fuelled a rally across AI infrastructure stocks. Arm stands to benefit indirectly from AI partnership initiatives with Saudi Arabia, as a key IP supplier to AI chipmakers. Combined with resilient enterprise tech demand and strong recurring revenue from partners like Nvidia and Amazon, Arm is well-positioned for multi-year growth amid rising global AI capex.

High-margin royalty and licensing expansion drive profitability. Arm’s record royalty and licensing revenue, each surpassing US$600mn last quarter, highlight the scalability of its asset-light, high-margin business model. New multi-year licensing deals, including in the automotive sector, and accelerating uptake of Armv9 CPUs and Compute Subsystems position the company to expand its market share and profitability across growth verticals like IoT, automotive, and AI.

4Q25 results. Revenue rose 33.6% YoY to US$1.24bn, above estimates by US$10mn. Its non-GAAP EPS of US$0.55 beat estimates by US$0.03. The company forecasts first quarter revenue of US$1.0bn to US$1.1bn, with a midpoint below analysts’ average estimate of US$1.1bn. Arm expects adjusted profit of US$0.30 to US$0.38 per share for the first quarter, compared with estimates of US$0.42.

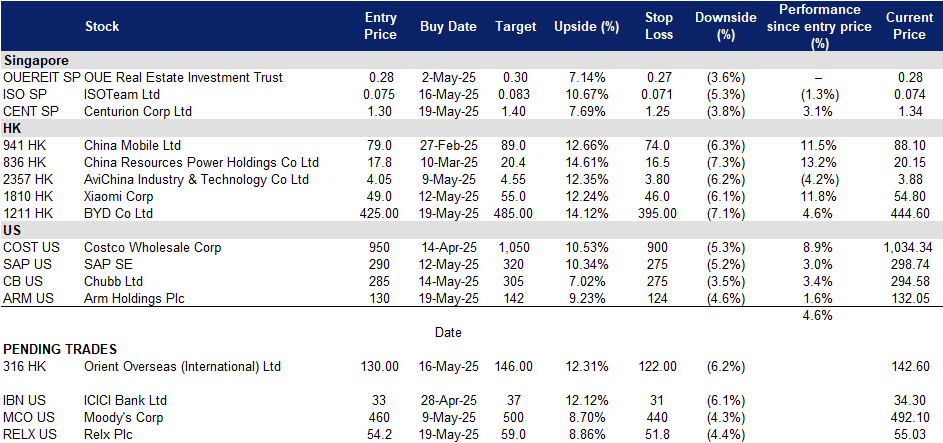

Trading Dashboard Update: Take profit on Zixin Group Holdings Ltd (ZXGH SP) at S$0.033. Add BYD Co Ltd (1211 HK) at HK$425, Centurion Corp Ltd (CENT SP) at S$1.30 and Arm Holdings Plc (ARM US) at US$130. Cut loss on JL Mag Rare Earth Co Ltd (6680 HK) at HK$14.1.