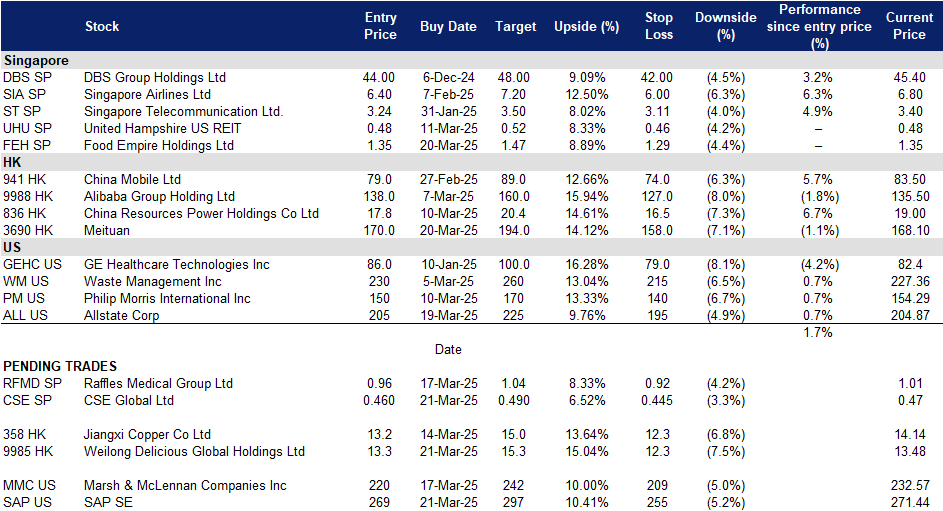

CSE Global Ltd (CSE SP): Fundamentals still strong

BUY Entry – 0.460 Target– 0.490 Stop Loss – 0.445

CSE Global Limited provides systems integration and information technology solutions, computer network systems, and industrial automation. The Company also designs, manufactures, and installs management information systems. CSE Global develops, manufactures, and sells electronic and micro processor monitoring equipment.

Strong top-line growth in the electrification business. CSE Global reported strong topline growth for its electrification business in FY24, rising from S$334.5mn in FY23, to S$434.8mn in FY24, representing a 30.0% YoY growth. The company’s automation business saw growth of 14.3% YoY, while its communications business saw a growth of 5.2% YoY. The ongoing AI trend is likely to positively impact demand for data centres and continue contributing to strong demand for the company’s electrification business.

Continued stable order books. CSE Global’s order book remained stable at S$672.6mn in FY24,which will be robust to drive revenue growth in FY25. On the other hand, order intake declined by 19.1% YoY, largely due to lower new projects orders in 2H24, as the U.S. Presidential Election approached. While uncertainties still remains in the United States, which is CSE Global’s largest market, the company still expects strong orders to come in amidst ongoing global trends, pushing demand for energy and communication services higher.

Recurring businesses to sustain growth. In addition to providing clients with engineering solutions across different industries and different markets, CSE Global also provides their existing clients with other services, such as routine checks and maintenance for their infrastructures. This business model creates a layer of revenue drivers for the company, allowing it to derive recurring revenue from each project with their clients through maintenance and checks after the initial projects are completed, while simultaneously maintaining stable cash flow. The company’s recurring business makes up 68.9% of the company’s revenue.

FY24 financial results. The company reported total revenue of S$861.2mn for FY24, increasing by 18.8% YoY, compared to S$725.1mn in FY23. The growth was mainly attributed to strong growth in its electrification business, which experienced a growth of 30.0%. Net profit attributable to equity owners increased by 16.9% YoY to S$26.3mn, despite a one-time exceptional loss of S$10.4mn, compared to S$22.5mn in FY23. The group’s EPS was 3.91 Scents in FY24, compared to 3.66 Singapore cents in FY23. CSE Global announced a final dividend of 1.15 Scents for 2H24, a decline from the previous years’ final dividends of 1.5 Scents. This brings the company’s FY24 dividend to 2.4 Scents, lower than FY23 total dividend of 2.75 Scents.

We have fundamental coverage with a BUY recommendation and a TP of S$0.60. Please read the full report here.

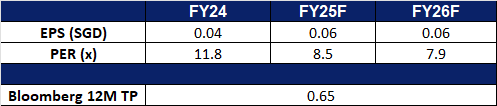

Market consensus

(Source: Bloomberg)

Food Empire Holdings Ltd (FEH SP): Strong growth to be continued in FY25

Food Empire Holdings Limited operates as a food and beverage manufacturing and distribution company. The Company offers beverages and snacks including classic and flavoured coffee mixes and cappuccinos, chocolate drinks, fruit-flavoured and bubble teas, cereal blends, and crispy potato snacks. Food Empire Holdings serves customers worldwide.

Sustained Growth in SouthEast Asia to Drive Topline Expansion. Food Empire continues to experience robust revenue growth in its Southeast Asian markets, with Vietnam standing out as a key growth driver. The region’s revenue surged by 27.3%, reaching US$129.4 million, fueled by strategic investments in brand development and a strong market demand. In Vietnam, the Group is focused on enhancing its brand presence and accelerating consumer acquisition, ensuring sustainable growth in a market poised for significant expansion. The country’s coffee market is projected to grow at a CAGR of 8.13% over the next five years, and Food Empire is well-positioned to capitalize on this growth. In Malaysia, the Group is focused on expanding its production capabilities. These initiatives are expected to continue driving strong growth in Southeast Asia in FY25. The company also reported solid growth across its other key markets. South Asia delivered a 24.9% revenue increase, while markets in Ukraine, Kazakhstan, and the CIS saw a 12.6% YoY growth. The Russian market experienced a slight 1.1% YoY decline. Notably, in local currency terms, the company saw both revenue and volume growth across all its major markets, demonstrating strong consumer demand despite ongoing geopolitical challenges and a high-interest-rate environment.

Driving more capacity for the group. The group is expanding its snack production capacity in Malaysia with the construction of a second factory, set for completion in 1Q25 and expected to be operational by 2Q25. This new facility will significantly enhance the group’s snack production capabilities. Additionally, the group is building its first coffee mix production facility in Central Asia, located in Kazakhstan. Scheduled for completion by the end of 2025, the facility is expected to increase coffee mix production capacity by approximately 15%, supporting future growth and revenue expansion. Meanwhile, the group is in the pre-construction phase of a new freeze-dried soluble coffee facility in Vietnam. Located in Binh Dinh province, this will be the group’s second freeze-dried plant and is slated for completion in early 2028. Once operational, it will strengthen Food Empire’s ingredients business and solidify its position as a leading producer of freeze- and spray-dried soluble coffee in the region.

Defensive F&B industry globally. The global food and beverage industry is inherently defensive, driven by stable demand for essential consumer goods rather than discretionary spending. This resilience provides a natural hedge during economic downturns, as consumers continue to prioritize necessities. Food Empire further strengthens its position through its diversified distribution network, which helps mitigate regional economic risks and ensures a steady revenue stream. While industry challenges such as supply chain fluctuations and rising operational costs persist, the company’s strategic focus on core product categories and efficient supply chain management reinforces its stability. As a result, Food Empire remains well-positioned within the globally defensive F&B sector, offering investors a degree of protection against economic volatility.

2H24 results review. Total revenue for 2H24 increased by 10.4% YoY to US$251.1mn from US$227.5mn in 2H23, led by strong growth in its South-East Asia, South Asia, as well as Ukraine, Kazakhstan and Commonwealth of Independent States segments. Its net profit fell 3.2% to US$28.9mn for 2H24, from US$29.8mn in the same period the year before. EPS for the period stood at US$0.0549, down from US$0.0567. The group proposed a dividend per share of S$0.08, comprising a final dividend of S$0.06 and a special dividend of S$0.02. This also marks the third consecutive year of an increase in dividends (excluding special dividends).

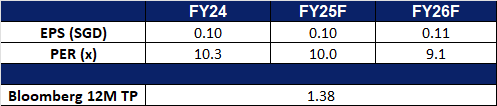

Market consensus

(Source: Bloomberg)

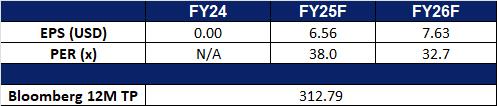

Weilong Delicious Global Holdings Ltd. (9985 HK): Plans to boost consumption

Weilong Delicious Global Holdings Ltd is a China-based holding company principally engaged in the production and sales of spicy snack foods. The Company operates in three segments: Seasoned Flour Products segment, Vegetable Products segment and Bean-based and Other Products segment. The Seasoned Flour Products segment mainly includes Big Latiao, Mini Latiao, Spicy Hot Stick, Mini Hot Stick and Kiss Burn. The Vegetable Products segment mainly includes Konjac Shuang and Fengchi Kelp. The Bean-based and Other Products segment mainly includes Soft Tofu Skin, 78° Braised egg and meat products.

Plans to Boost Consumption. China has unveiled a “Special Action Plan to Boost Consumption”, reinforcing its commitment to stimulating domestic demand. The plan aims to drive consumption growth, expand household spending power, and enhance purchasing capacity by raising incomes and reducing financial burdens. This follows Premier Li Qiang’s recent government work report, which identified consumption growth as the country’s top economic priority for the year. Key measures include employment support initiatives, enhanced unemployment benefits, and targeted income-boosting efforts for both urban and rural residents, including farmers. Beyond short-term stimulus, the plan signals China’s resolve to tackle structural challenges such as stagnant wage growth, negative wealth effects from property and stock market downturns, and an inadequate social safety net. The expected rise in consumer spending could have a positive impact on Weilong Delicious Global Holdings, as stronger domestic demand may support the company’s growth.

Partnership with KFC. Earlier this year, Weilong Delicious has partnered with KFC to launch a co-branded “Spicy Strip Flavor Large Chicken Strips,” capitalizing on the fast-food chain’s popular “Crazy Four” promotion to engage young consumers. This collaboration follows previous partnerships with Pizza Hut and Xiaolongkan Hotpot, reinforcing Weilong’s strategy of leveraging fast-food platforms to enhance brand visibility and product appeal. By prioritizing genuine product innovation and aligning with fast-food consumption trends, Weilong aims to translate marketing buzz into sustained consumer engagement. This approach reflects shifting dynamics in China’s consumer market, where brands must focus on core customer segments and product differentiation rather than broad, awareness-driven marketing campaigns to drive long-term growth.

1H24 results review. Revenue increased by 26.3% YoY to RMB2.94bn in 1H24, compared with RMB2.33bn in 1H23. Net profit increased by 38.9% to RMB621.2mn in 1H24, compared to RMB447.1mn in 1H23. EPS rose from RMB0.19 in 1H23 to RMB0.27 in 1H24.

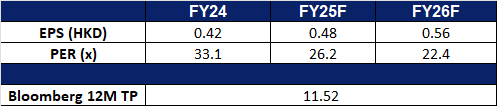

Market consensus.

(Source: Bloomberg)

Meituan (3690 HK): To benefit from more consumption policies

Meituan is an investment holding company mainly engaged in technology retail, providing daily necessities and services through technology and retail fields, including food delivery, in-store, hotel and travel reservations, other services and sales. The Company operates its businesses through two segments. The Core Local Commerce segment includes food delivery, Meituan Instashopping, in-store services, and hotel and travel related businesses. New Initiatives segment includes Meituan Select, Xiaoxiang Supermarket, B2B food distribution and among others. The Company distributes its products within domestic market.

More support for consumption. China’s financial regulator last friday urged institutions to boost support for consumption, promising to properly relax consumer credit quotas and loan terms as it offers long-term backing to make available large sums. It pledged to increase financing support to service industries such as retail, accommodation, catering, tourism, education and healthcare. The National Financial Regulatory Administration (NFRA) also added that it encouraged financial institutions to provide loan renewal support to eligible borrowers of personal consumption loans. These policies are expected to boost China’s consumption level in the near term, and has also improved investors confidence towards China’s consumer market.

Gaining market share. Meituan has established its strong market presence in China, and this has allowed the company to expand aggressively, with growing operations across Asia and the Middle East where it typically enters markets with steep discounts. The company’s subsidiary, KeeTa, also launched in Hong Kong in 2023 and quickly took market share through heavy promotions. The company is also expanding beyond Asia, including to Saudi Arabia, where it’s also upending the market. Furthermore, Deliveroo, one of Meituan’s Keeta competitors in the Hong Kong market, announced that it will close its Hong Kong business due to stiff competition and price wars in Hong Kong from Foodpanda and KeeTa. This further re-emphasize KeeTa’s dominance in the Hong Kong market.

Partnership with Walmart. At the end of 2024, Meituan entered into a new strategic partnerhips with Walmart. The partnership would help Walmart to accelerate its e-commerce business, which currently accounts for nearly half of its China sales. Stores in China have already been connected to Meituan’s delivery ecosystem. In addition to Walmart stores, Walmart China has opened 50 Sam’s Club stores in China, which have benefitted from Chinese consumers increasingly seeking out membership stores. This partnership would also increase delivery volume as well as expand Meituan’s retail offerings for its customers. By integrating Walmart’s stores, including Sam’s Club locations, into its delivery ecosystem, Meituan gains a substantial increase in delivery orders. The partnership allows Meituan to expand its offerings beyond food delivery, incorporating a wider range of retail goods from Walmart. This diversifies Meituan’s platform and attracts a broader customer base, translating to higher transaction volumes and revenue.

3Q24 results review. Revenue increased by 22.4% YoY to RMB93.6bn in 3Q24, compared with RMB76.5bn in 3Q23. Adjusted net profit increased by 124.0% to RMB12.8bn in 3Q24, compared to RMB5.73bn in 3Q23. Number of on-demand delivery transactions also rose by 14.5% to 7.08bn in 3Q24, compared to 6.18bn in 3Q23.

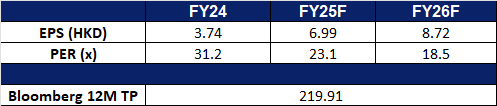

Market consensus.

(Source: Bloomberg)

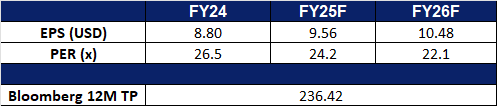

SAP SE (SAP US): SAP conquers

BUY Entry – 269 Target – 297 Stop Loss – 255

SAP SE is a multinational software company. The Company develops business software, including e-business and enterprise management software, consults on organizational usage of its applications software, and provides training services. SAP markets its products and services worldwide.

Improving automation process. SAP SE announced new generative AI features and an expanded partnership with American Express at SAP Concur Fusion. Joule, SAP’s AI copilot, will be integrated into Concur solutions to automate travel and expense management. Additionally, SAP Concur and American Express introduced real-time authorization data for corporate card transactions. SAP Concur remains the market leader in travel and expense management, with further integrations planned with Mastercard and American Express Global Business Travel. By deepening partnerships with financial services providers and expanding automation capabilities, SAP aims to enhance user experience, drive compliance, and improve cost efficiencies for businesses. Future developments in AI-powered expense processing and travel planning will likely strengthen its competitive advantage and customer adoption.

Capital inflow. Rising capital inflows into European markets, driven by Germany’s fiscal stimulus and increased defence spending, are fuelling a shift from US to European equities. With 60% of investors expecting stronger European growth, sectors like financials, industrials, and small caps are gaining momentum, with Germany as the preferred market. As Europe’s economy strengthens, businesses will accelerate digital transformation. SAP, as the region’s leading enterprise software provider, is well-positioned to capitalize on increased corporate investment in technology and cloud-based solutions.

4Q24 results. Revenue rose 10.7% YoY to €9.38 billion, beating expectations by €240 million. Non-GAAP earnings per share were €1.40, missing expectations by €0.05. The company declared dividend of €2.35/share annual dividend, 6.8% increase from prior dividend of €2.20/share, payable on 16 May.

Market consensus

(Source: Bloomberg)

Marsh & McLennan Companies Inc (MMC US): Growth and expansion in focus

Marsh & McLennan Companies, Inc. is a professional services firm providing advice and solutions in the areas of risk, strategy, and human capital. Marsh & McLennan offers analysis, advice, and transactional capabilities to clients worldwide.

Rising demand for insurance and risk planning. In the new global trade war macro environment, rising trade costs will prompt businesses to optimize their insurance expenditures, with particular attention to the adverse effects of tariff changes and supply chain disruptions on operations. At the same time, there is an increasing demand for risk control, particularly in geopolitical risk assessment. This benefits the company’s insurance brokerage and risk management services business. The global insurance brokerage industry was valued at US$259.7bn in 2022 and is expected to grow to US$628.3bn by 2032, with a compound annual growth rate (CAGR) of 9.3%.

Positive synergies. The company acquired insurance brokerage and risk management provider McGriff for US$7.75bn, which is expected to generate significant positive synergies. With McGriff’s annual revenue of approximately US$1.2bn, the integration will provide Marsh with more cross-selling opportunities and expand its client base. By leveraging McGriff’s extensive client network and expertise, the company expects overall revenue to grow by 3-5% in the first-year post-acquisition. Excluding amortization, McGriff’s earnings should fully offset the additional interest costs, ensuring a neutral impact on cash flow. Additionally, operational efficiencies and revenue growth from the acquisition are projected to drive long-term earnings accretion of 2-3% annually.

4Q24 results. Revenue rose 9.9% YoY to US$6.1 billion, beating expectations by US$140 million. Non-GAAP earnings per share were US$1.87, beating expectations by US$0.11. The board of directors declared a quarterly dividend of US$0.815 per share on outstanding common stock, payable on 15 May to stockholders of record on 3 April. For FY25, the company expects mid-single-digit underlying revenue growth, with continued margin expansion. It anticipates that the McGriff acquisition will be modestly accretive to adjusted EPS in 2025 and more significantly in 2026. Planned capital deployment for 2025 is set at US$4.5bn.