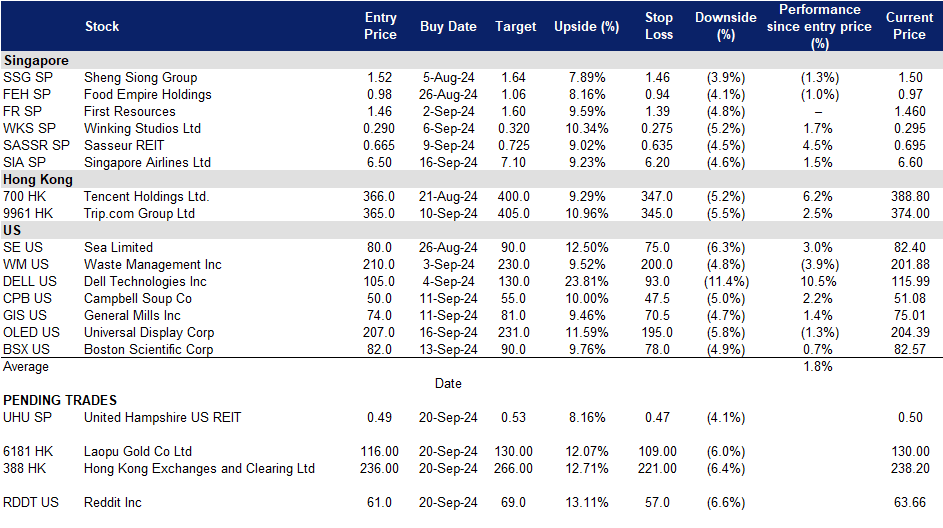

20 September 2024: Singapore Airlines Ltd (SIA SP), Laopu Gold Co Ltd (6181 HK), Universal Display (OLED US)

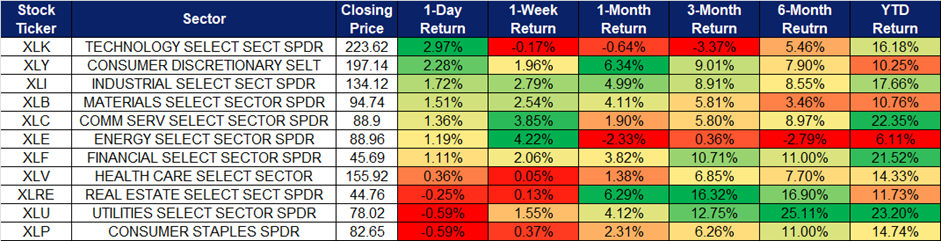

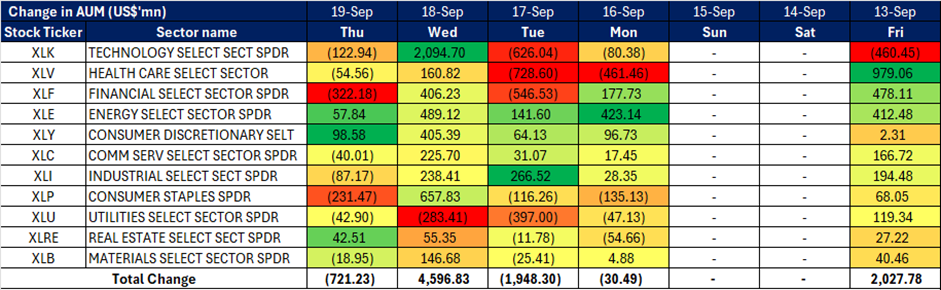

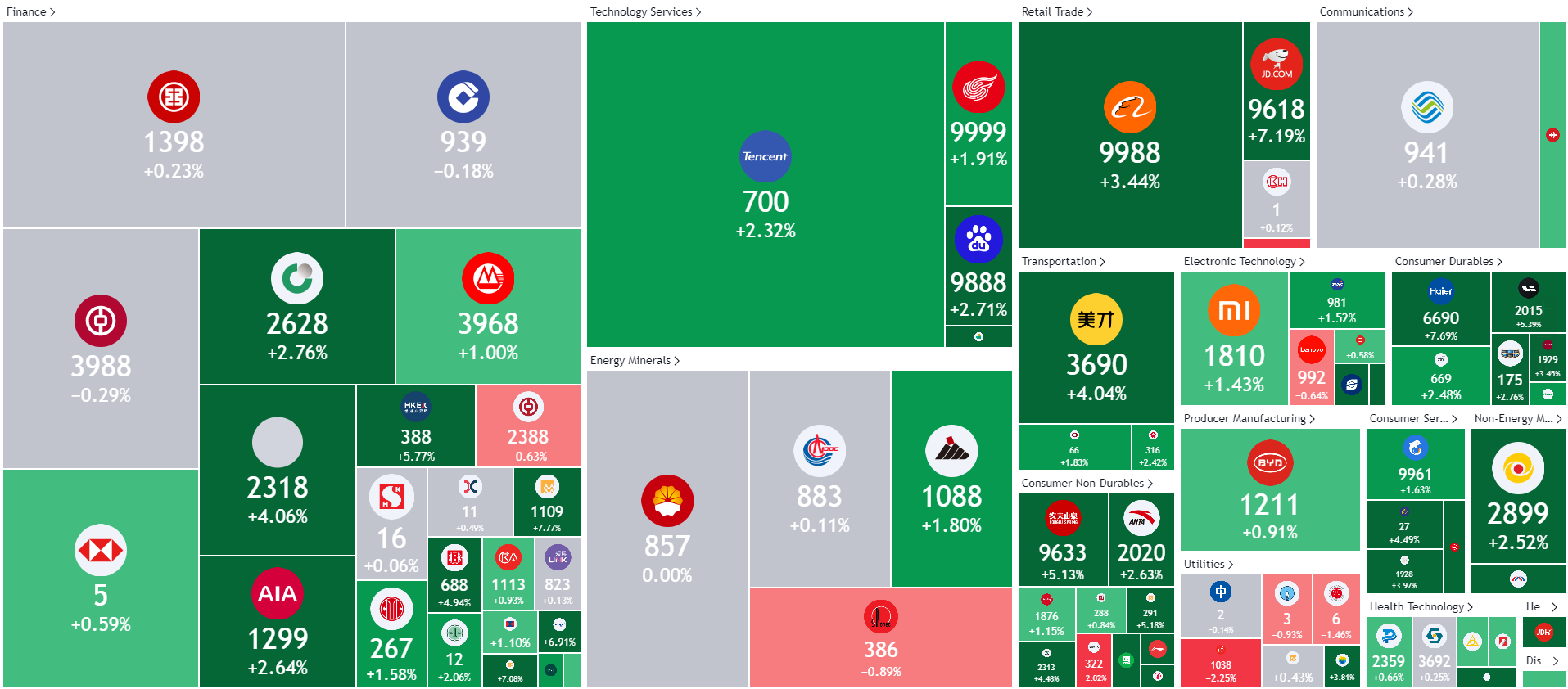

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

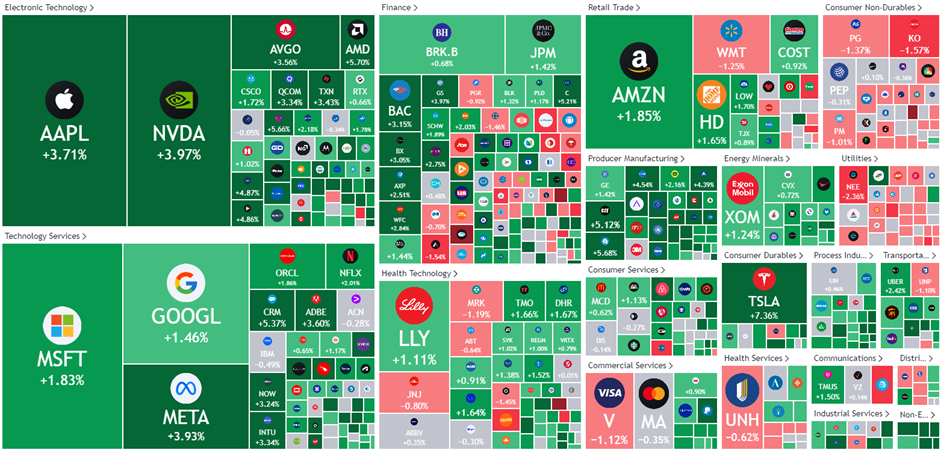

United States

Hong Kong

United Hampshire US REIT (UHU SP): More rate cuts to come

- BUY Entry – 0.49 Target– 0.53 Stop Loss – 0.47

- United Hampshire US REIT operates as a real estate investment trust. The Company owns and operates shopping, storage, grocery, and necessity-based retail properties.

- Optimism surrounding US Federal Interest rate cuts. The US Federal Reserve cut interest rates by 0.5% on 18 September, marking its first reduction in over four years, ahead of the November presidential election. Fed Chairman Jerome Powell cited slowing inflation and the need to maintain labour market strength as key reasons for the cut. The Fed aims to prevent a significant economic slowdown, particularly as unemployment has slightly increased. Projections indicate further rate cuts through 2026, with the benchmark rate expected to drop to 2.75% to 3%. While there were concerns over reigniting inflation, the Fed emphasized its readiness to adjust policy if needed to meet its goals of stable prices and maximum employment. Economic growth is projected to remain steady, with inflation approaching the Fed’s 2% target by 2025. These further rate reductions are poised to benefit United Hampshire US REIT by lowering borrowing costs, enhancing financial flexibility, and potentially attracting higher investor interest. This favourable interest rate environment aligns with the REIT’s growth strategy, positioning it for increased profitability and value creation in the upcoming quarters.

- Organic growth to drive upside in profitability. United Hampshire US REIT expects organic growth to drive profitability, leveraging built-in rental escalation in the majority of long-term tenant contracts and shorter-term leases in prime self-storage properties. These factors contribute to potential revenue growth and enhanced operational performance.

- Better positioning for active management. If the Federal Reserve implements rate cuts, United Hampshire US REIT stands to benefit in the coming year, enabling proactive portfolio management through strategic acquisitions and divestments. This flexibility underscores the REIT’s capability to adapt to changing market conditions and optimize its asset base.

- 1H24 results review. Revenue for 1H24 increased by 2.4% YoY to US$36.8mn, compared to US$36.0mn in 1H23. Net profit declined by 25.4% YoY to US$9.67mn in 1H24, compared to US$12.96mn in 1H23, mainly due to high interest rates. It also divested a Freestanding Lowe’s and Freestanding Sam’s Club Property within Hudson Valley Plaza for a divestment consideration of US$36.5mn.

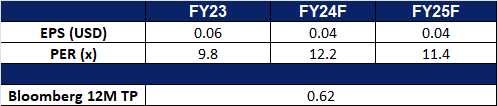

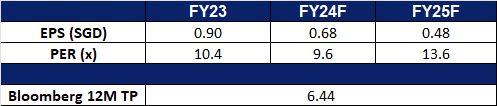

- We have fundamental coverage with a BUY recommendation and a TP of S$0.60. Please read the full report here.

- Market Consensus.

(Source: Bloomberg)

Singapore Airlines Ltd (SIA SP): Improved margins

- RE-ITERATE BUY Entry – 6.5 Target– 7.1 Stop Loss – 6.2

- Singapore Airlines Limited provides air transportation, engineering, pilot training, air charter, and tour wholesaling services. The Company’s airline operation covers Asia, Europe, the Americas, South West Pacific, and Africa.

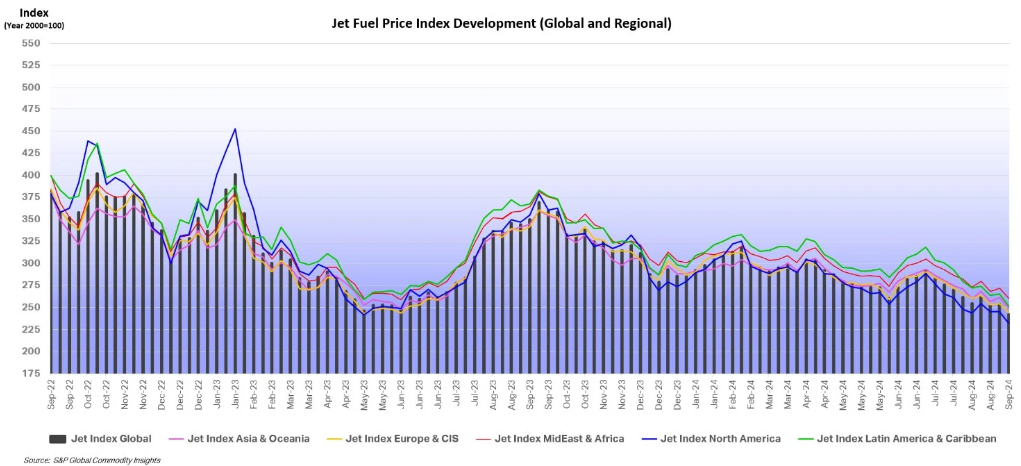

- Continued strong travel demand. According to the International Air Transport Association (IATA) in July 2024, global air passenger demand increased by 8%, reaching a record high, with capacity up 7.4% and a load factor of 86%. International travel grew by 10.1%, while domestic demand rose 4.8%, despite disruptions like the CrowdStrike IT outage. Asia-Pacific saw the highest demand growth at 19.1%, though some routes remain below pre-pandemic levels, while Europe and Latin America also posted strong gains. North America had the highest load factor at 89.4%. IATA highlighted the need to resolve supply chain issues to maintain accessibility and affordability in air travel. With declining jet fuel prices and sustained demand, Singapore Airlines will continue to benefit from improved margins.

Jet Fuel Price Trend

(Source: International Air Transport Association)

- Potential growth in Indian travel market. India has approved Singapore Airlines’ foreign direct investment into the merged Air India-Vistara entity, clearing the final hurdle for the merger. SIA will hold a 25.1% stake in the new carrier with an initial investment of ₹20.6 billion, expected to increase to ₹50.2 billion after completion. Vistara flights will be operated by Air India starting in November 2024. The merger, delayed from its original March target, is expected to close by the end of 2024, giving SIA a significant foothold in India’s rapidly growing travel market.

- 1Q25 results review. Total revenue for Q1 increased by 5.3% YoY to S$4,718mn from S$4,479mn in 1Q24. Passenger flown revenue grew 4.1% to S$3.8bn, supported by a 13.8% increase in passengers carried and strong load factors. Net profit saw a 38.4% YoY decline to S$452mn, due to weaker operating performance, a reduction in net interest income, lower surplus on disposal of aircrafts and spare engines, and a lower share of profit from its associated companies.

- Market Consensus.

(Source: Bloomberg)

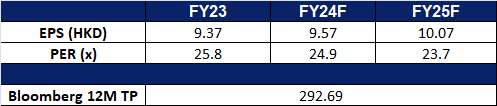

Hong Kong Exchanges and Clearing Ltd (388 HK): Expecting more fund inflows

- BUY Entry – 236 Target 266 Stop Loss – 221

- Hong Kong Exchanges and Clearing Limited (HKEX) is principally engaged in the operation of stock exchanges. The Company operates through five business segments. The Cash segment includes various equity products traded on the Cash Market platforms, the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The Equity and Financial Derivatives segment includes derivatives products traded on Hong Kong Futures Exchange Limited (HKFE) and the Stock Exchange of Hong Kong Limited (SEHK) and other related activities. The Commodities segment includes the operations of the London Metal Exchange (LME). The Clearing segment includes the operations of various clearing houses, such as Hong Kong Securities Clearing Company Limited, the SEHK Options Clearing House Limited, HKFE Clearing Corporation Limited, over the counter (OTC) Clearing Hong Kong Limited and LME Clear Limited. The Platform and Infrastructure segment provides users with access to the platform and infrastructure of the Company.

- Lower interest rates to drive fund flow. Hong Kong’s central bank lowered its interest rate by 50 basis points to 5.25% yesterday, mirroring the U.S. Federal Reserve’s move. This rate cut is expected to boost business confidence and stimulate consumer spending in Hong Kong. Lower rates are also likely to encourage a shift of funds from safe assets into the stock market, enhancing market liquidity and trading volumes. As a result, HKEX is well-positioned to benefit from increased capital inflows into the stock market.

- To benefit from increasing IPO activities. Hong Kong’s IPO market is poised for growth, with positive signals suggesting more mega deals on the horizon. According to Chan, CEO of HKEX, the market expects increased IPO activity and sustained momentum. Medea’s recent IPO on the HKEX raised HK$31.01 billion, marking the city’s largest listing in over three years. So far this year, Hong Kong has raised approximately HK$51 billion through 45 IPOs and is expected to see continued robust activity through year-end. Alongside IPOs, the city’s secondary fundraising market is also gaining traction, with over US$20 billion raised through follow-on offerings to date. This surge in IPO and fundraising activity is set to significantly benefit HKEX.

- 1H24 earnings. Revenue rose marginally by 0.4% YoY to HK$10.6bn in 1H24, compared to HK$10.8bn in 1H23. Net profit fell by 3.0% YoY to HK$6.12bn in 1H24, from HK6.31bn in 1H23. Basic and diluted earnings per share was HK$4.84 in 1H24, compared to HK$4.99 in 1H23.

- Market consensus.

(Source: Bloomberg)

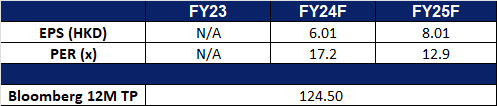

Laopu Gold Co Ltd (6181 HK): Gold rush in China

- BUY Entry – 116 Target 130 Stop Loss – 109

- Laopu Gold Co., Ltd. produces and sells jewelry products. The Company produces pendants, bracelets, bracelets, collectibles, ornaments, and other products. Laopu Gold also operates import and export businesses.

- Gold demand to remain high. China’s central bank paused gold purchases for the fourth consecutive month in August, despite the value of its gold reserves rising to US$182.98bn, driven by a 21% surge in gold prices this year. This rise is fuelled by expectations of US rate cuts and increased safe-haven demand amid global geopolitical and economic uncertainties. While the People’s Bank of China (PBOC) was the largest gold buyer in 2023, its recent pause has tempered domestic investor demand. However, analysts anticipate the PBOC will eventually resume purchases to reduce its reliance on the US dollar as a reserve asset. In July, China’s net gold imports via Hong Kong increased by 17% from the previous month, with total imports rising by over 6%, signalling growing demand. Despite weak demand for gold jewellery due to economic uncertainty, Chinese banks have received new gold import quotas, reflecting expectations of rising demand. Interest in gold coins and bars remains steady, and with ongoing economic instability and concerns over currency depreciation, gold demand is expected to remain strong in the coming months.

- Gold jewellery still shining. Laopu Gold, renowned for its traditionally crafted gold jewellery, has strategically positioned itself as a luxury brand, with fixed pricing for its pieces rather than pricing by weight, earning it the nickname “Hermès of Gold.” Leveraging its first-mover advantage in the heritage gold jewellery industry, Laopu focuses on product innovation, design, and quality customer service. Laopu is well-placed to capitalize on the booming gold jewellery market in China, where culturally resonant designs are attracting younger buyers. The “guochao” (China chic) trend, which celebrates Chinese identity, combined with gold’s rising value as a safe-haven asset, presents a significant growth opportunity. Young consumers are increasingly valuing the purchasing experience, craftsmanship, and cultural stories behind their jewellery, reshaping the market and positioning Laopu to capture this growing demand.

- 1H24 earnings. Revenue rose by 148.3% YoY to RMB3,520.19mn in 1H24, compared to RMB1,417.51mn in 1H23. Net profit rose by 198.8% YoY to RMB587.81mn in 1H24, from RMB196.75mn in 1H23, due to expansion of brand awareness, including both online and offline channels; the continuing optimization, promotion and iteration of the Group’s products; customers’ preference for high-quality heritage gold products with significant cultural and product value resulting from the changes in consumer consumption attitudes and upgrading of consumption concepts; and six new boutiques and expanded one boutique which resulted in an increased revenue contribution. Basic and diluted earnings per share was RMB4.11 an increase from RMB1.44 in 1H23.

- Market consensus.

(Source: Bloomberg)

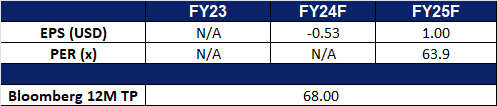

Reddit Inc (RDDT US): Small and mid-cap upcycle kick starts

- BUY Entry – 61 Target – 69 Stop Loss – 57

- Reddit, Inc. operates as a network of communities. The Company offers a social networking platform where anyone can join a community to learn from one another, engage in authentic conversations, explore passions, research new hobbies, exchange goods and services, create new communities, and find belonging. Reddit serves customers worldwide.

- More rate cuts in the pipeline. Following the Federal Reserve’s 50-basis point rate cut in September, small and mid-cap stocks are poised to significantly benefit. With anticipated continued rate reductions of 50 basis points in the remainder of 2024, 100 basis points in 2025, and an additional 50 basis points in 2026, small and mid-cap companies will enjoy lower financing costs. This, combined with increased fund volume in the market due to lower interest rates, will provide a favourable environment for these companies. Moreover, the rate cuts signal the Fed’s confidence in the global economy, which bodes well for the advertising space and, consequently, Reddit’s revenue growth.

- Growth in advertising revenue, narrowing losses. Reddit’s strategic partnerships with major sports leagues such as NFL, NBA, MLB, NASCAR, and PGA Tour, and OpenAI have significantly bolstered its position in the digital advertising market. By leveraging these collaborations, Reddit has not only enhanced its ad offerings but has also fostered stronger community dynamics, driving substantial growth in ad revenue. This is exemplified by the impressive 41% YoY increase in ad revenue, coupled with a 51% surge in daily active users. Reddit’s commitment to refining its advertising technology and expanding its market reach positions it for continued success and sustained growth in the digital advertising landscape. Moreover, the company’s ongoing development of dynamic product ads (DPA) demonstrates its dedication to delivering highly personalized ad experiences to users, which is expected to further contribute to revenue growth in the future.

- 2Q24 earnings review. Revenue rose by 53.6% YoY to US$281.2mn, beating estimates by US$27.32M. GAAP EPS was -US$0.06, beating estimates by US$0.24. In Q3 revenue is expected to be range between US$290mn to US$310mn vs US$282.34mn consensus and adjusted EBITDA in the range of US$40mn to US$60mn.

- Market consensus.

(Source: Bloomberg)

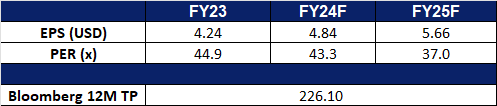

Universal Display (OLED US): OLED gadgets in demand

Universal Display (OLED US): OLED gadgets in demand

- RE-ITERATE BUY Entry – 207 Target – 231 Stop Loss – 195

- Universal Display Corporation is a member of the United States Display Consortium. The Consortium is a cooperative industry and government effort aimed at developing an infrastructure to support a North American flat panel display infrastructure. The Company and its partners are developing high-resolution, full color, light weight Organic Light Emitting Diode (OLED) technology.

- Demand for notebook and tablet OLED products is growing. OLED adoption is rapidly expanding in mobile PCs. Omdia forecasts a 37% compound annual growth rate in demand for OLED panels in laptops and tablets from 2023 to 2031. This surge reflects a growing number of brands investing in high-end notebooks with OLED displays. Market penetration is accelerating shipments of OLED screen tablets and laptops are projected to reach 12 million and 5 million units, respectively, in 2024. By 2027, these figures are expected to increase to 21 million and 28 million units.

- Strong cash position. As of the second quarter of 2024, the company held US$530.5mn in cash and equivalents, significantly exceeding its total debt of US$24.7mn. This robust cash position demonstrates the company’s strong financial health and ability to generate cash. Free cash flow in the second quarter reached US$57.89mn, approaching the historical peak of US$66.38mn.

- 2Q24 earnings review. Revenue rose by 8.1% YoY to US$158.5mn, missing estimates by US$1.44M. GAAP EPS was US$1.10, missing estimates by US$0.05.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Boston Scientific Corp (BSX US) at US$82.