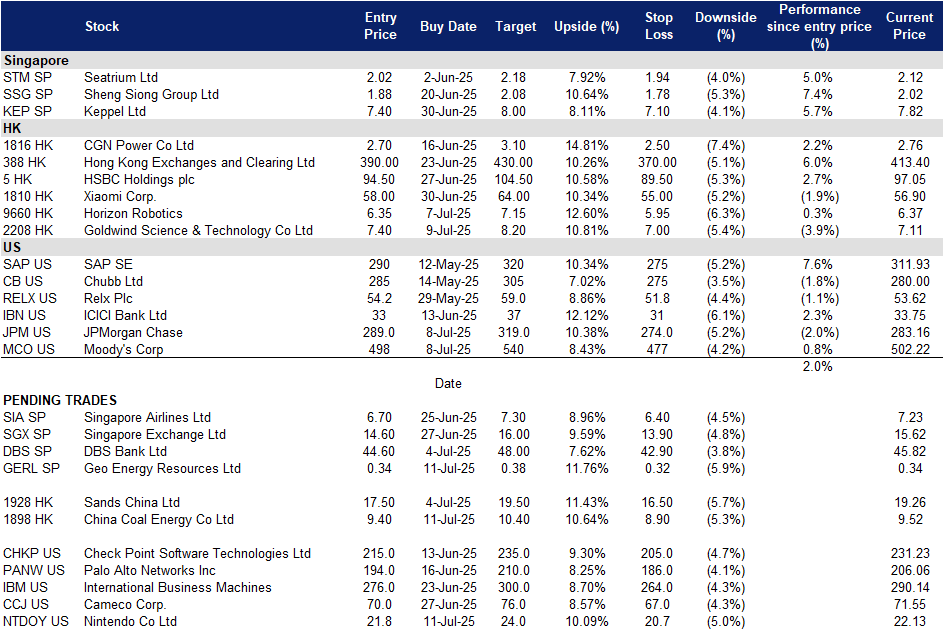

Geo Energy Resources Ltd (GERL SP): Heatwave spurring energy demand

BUY Entry – 0.34 Target – 0.38 Stop Loss – 0.32

Geo Energy Resources Limited is an integrated coal mining specialist. The Company owns and operates coal mines, offers mine contracting services to third party mine owners, and sells coal to both coal traders and coal export companies.

Heatwave-driven power demand supports coal outlook. China’s ongoing heatwave is triggering record-breaking electricity demand, with temperatures exceeding 40°C in several regions. The National Energy Administration reported that national power load hit a historic high of 1.465 billion kilowatts, up 200 million kilowatts from late June and nearly 150 million kilowatts YoY. This surge in power usage is expected to boost seasonal demand for thermal coal, providing near-term tailwinds for producers like Geo Energy.

Resilient performance amid shifting coal trade flows. Geo Energy Resources has demonstrated strong operational resilience despite macro shifts in global coal demand, particularly from top importers China and India, which are reducing lower-calorific coal imports in favour of higher-energy alternatives. While overall Indonesian coal exports have declined, falling over 12.3% to China and 14.3% to India between January to May, Geo Energy remains insulated from volume risk due to its long-term offtake agreements. In Q1, the company reported a 94% YoY increase in sales volume to 3.5Mt, generating US$166.4 million in revenue and US$14.1 million in net profit, even amid softer ICI4 prices. With a stable sales pipeline and strong operational leverage, Geo Energy is well-positioned to weather pricing volatility and maintain performance amid broader market shifts.

1Q25 business updates. Geo Energy reported 1Q25 revenue of US$166.4mn, a 68% YoY increase from 1Q24 revenue of US$99.0mn due to an increase in production and sales volume, offsetting the decline in average selling price. Net profit rose 63% YoY to US$14.1mn. Its cash profit declined from US$13.18/tonne to US$11.16/tonne. The 0.25 S-cent per share interim dividend is 25% higher YoY and implies a dividend payout ratio of 19%, the company maintains committed to its dividend policy of 30% for the full year, reinforcing management’s confidence in long-term growth.

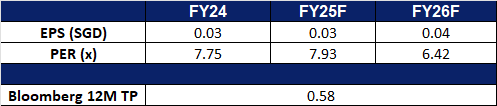

We have fundamental coverage with a BUY recommendation and a TP of S$0.69. Please read the full report here.

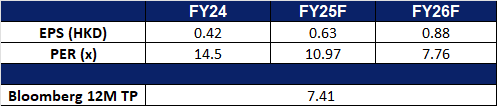

Market consensus

(Source: Bloomberg)

DBS Group Holdings Ltd (DBS SP): Boosting customer growth, one cashback at a time

DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

Safe-haven appeal and market volatility driving growth. DBS stands to benefit from Singapore’s growing status as a financial haven amid global uncertainties, including U.S. economic concerns, trade tensions and a weakening USD. The strengthening SGD, combined with an inverse correlation to the STI, makes Singaporean assets more attractive to international investors. DBS, with its dominant local presence, saw market trading activity more than double in Q1, its highest in 12 quarters, driven by FX, interest rate and equity derivatives. Ongoing macro volatility and capital inflows into Singapore will likely boost DBS’s trading and wealth management income.

Strengthening digital ecosystem and brand loyalty. Through its SG60 campaign, DBS/POSB is driving increased engagement and transaction volume with initiatives like the weekly S$3 cashback, S$0.60 and S$6 meal deals, and eVoucher rewards via PayLah! and POSB cards. Running from July to September, these offers aim to ease cost-of-living pressures and encourage digital payments at over 22,000 heartland merchants. This initiative not only reinforces DBS’s community presence but also deepens user adoption of its digital platforms and payment products, supporting fee-based income and customer retention.

1Q25 Business Updates. Total income for 1Q25 rose 6% YoY to a record of S$5.91bn from broad-based business growth, while net profit fell 2% YoY to S$2.90bn, due to the impact of the 15% global minimum tax, with return on equity at 17.3%. The board declared a total dividend of S$0.75 per share for the first quarter.

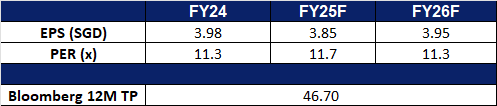

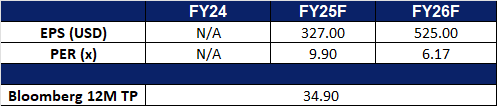

Market consensus

(Source: Bloomberg)

China Coal Energy Co. Ltd. (1898 HK): Feeling the heat

BUY Entry – 9.40 Target – 10.40 Stop Loss – 8.90

China Coal Energy Company Limited is a China-based company principally engaged in the coal production and distribution businesses. The Company’s coal businesses mainly include the production and distribution of steam coal and coking coal. The coking businesses mainly include the production and distribution of metallurgy cokes and forging cokes. The coal related equipments businesses mainly include the manufacture of hydraulic supports, scraper conveyors, loaders, boring machines, shearers and mining electrical motors, among others. The other businesses mainly include the production of electrolytic aluminum and coal gas. The Company mainly distributes its products in domestic and overseas markets.

Heatwave-Driven Power Demand. China is currently grappling with severe heatwaves across multiple regions, with temperatures exceeding 40°C in some areas. These extreme conditions have triggered yellow heat alerts and public health warnings, while also pushing electricity demand to unprecedented levels. The National Energy Administration (NEA) reported that sustained high temperatures have driven the national power load to a record 1.465 billion kilowatts last Friday—an increase of 200 million kilowatts from late June and nearly 150 million kilowatts year-on-year. This surge in electricity usage is expected to boost seasonal coal demand, benefiting major suppliers such as China Coal Energy.

Increasing coal-fired power capacity in China. Despite accelerating investments in renewable energy, China remains committed to expanding its coal-fired power capacity through at least 2027. According to recently published government guidelines, new coal plants will be developed to meet peak electricity demand and support grid stability, particularly in high-demand regions. The China Coal Association also noted that rising coal usage in the power and chemical sectors will help offset declining demand from the steel and construction materials industries.

Continued Dependence on Coal. Coal is expected to remain a dominant energy source in the near term, accounting for 57% of China’s power generation in 2025, followed by hydro, solar, and onshore wind, according to S&P Global. Coal consumption is projected to peak in 2029 and then decline by 4% by 2030 compared to 2025 levels. This underscores the continued strategic importance of coal in ensuring energy security and grid reliability in mainland China.

1Q25 results review. 1Q25 operating revenue fell by 15.4% to RMB38.4bn, compared to RMB45.4bn in 1Q24. Net profit fell by 20.0% to RMB3.98mn in 1Q25, compared to RMB4.97mn in 1Q24. Basic EPS fell to RMB0.30 in 1Q25, compared to RMB0.37 in 1Q24.

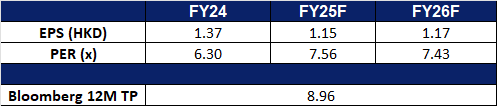

Market consensus.

(Source: Bloomberg)

Goldwind Science & Technology Co Ltd. (2208 HK): Ramping up renewable energy capacity

Goldwind Science & Technology Co Ltd is a China-based company principally engaged in the wind turbine manufacturing, wind power services, and wind farm investment and development. The Company operates four segments. The Wind Turbine Generator Manufacturing and Sale segment is primarily engaged in the research and development, manufacturing, and sales of wind turbine generators and spare parts. The Wind Power Services segment primarily provides wind power-related consulting, wind farm construction, maintenance, and transportation services. The Wind Farm Development segment is primarily engaged in wind farm development and operations. Other segment is primarily engaged in water treatment development and operations, financial investments, and other businesses. The Company mainly conducts its businesses in the domestic market and overseas markets.

China set to ramp up renewables amid rising AI-driven power demand. China is expected to add a record 500 gigawatts (GW) of renewable energy capacity to its national grid this year, driven in part by surging electricity demand from AI-powered data centres. According to the State Grid Energy Research Institute, wind power alone will account for 140 GW of new capacity — a 77% increase from last year, marking the first time new renewable installations could exceed 500 GW in a single year. This rapid capacity expansion supports China’s dual carbon goals of peaking emissions before 2030 and achieving carbon neutrality by 2060. The significant growth in wind power is likely to benefit domestic turbine manufacturers like Goldwind Science & Technology, positioning the company to capture greater market share.

China supports Europe’s green energy goals. As Europe accelerates its shift toward clean energy to reduce reliance on fossil fuel imports, Chinese new energy companies are becoming key partners, especially in the solar and wind sectors. With the EU targeting 42.5% renewables in final energy consumption by 2030 (up from the current 32%) and facing limited domestic production capacity, cooperation with China is increasingly vital. Chinese firms, known for their advanced technology and scale, are helping meet this demand. Companies like TotalEnergies have already integrated Chinese-made solar panels and wind turbines into projects across Europe and beyond. This growing collaboration enhances export opportunities for Chinese wind turbine makers such as Goldwind, reinforcing its global expansion strategy.

Goldwind anticipates strong shipment growth in 2025. Goldwind Science & Technology expects wind turbine shipments to surge in 2025, supported by a 56% year-on-year increase in outstanding orders, which reached 47,404 MW by the end of 2024. While offshore wind remains a strategic focus, the company expects onshore projects to continue dominating demand. Its large-capacity turbines (6 MW and above) were a key growth driver last year, accounting for 61% of total sales with a 59% volume increase. The moderation in the size escalation of onshore units is seen as beneficial for long-term product quality and industry sustainability. With international revenue up 15.5% and new orders secured across eight countries, Goldwind is well-positioned for continued growth both at home and abroad.

1Q25 results review. 1Q25 operating revenue rose by 35.7% to RMB9.47bn, compared to RMB6.98bn in 1Q24. Net profit rose by 70.8% to RMB568.2mn in 1Q25, compared to RMB332.6mn in 1Q24. Basic EPS rose to RMB0.1299 in 1Q25, compared to RMB0.0726 in 1Q24.

Market consensus.

(Source: Bloomberg)

Nintendo Co Ltd (NTDOY US): Switch 2, I choose you!

BUY Entry – 21.8 Target – 24.0 Stop Loss – 20.7

Nintendo Co., Ltd. develops, manufactures, and sells household leisure equipment. The Company produces home use video game hardware and software products. Nintendo markets its products across worldwide.

Switch 2 sets record pace amidst supply strain. Nintendo’s Switch 2 has become the fastest-selling console launch in history, outperforming both the original Switch and Sony’s PlayStation 5 in its first month despite significant supply constraints. With an estimated 6 million units shipped at launch and projections reaching 18-20 million by March 2026, Nintendo is clearly capitalizing on sustained global demand. The lottery-based sales in Japan and invitation-only listings on Amazon, is further fuelling interest and pricing power. As Nintendo expands production capacity and improves flexibility, the company is well-positioned to meet pent-up demand heading into FY26, supporting strong top-line momentum. The Switch 2 also commands a higher price point, reflecting increased hardware value, enabling Nintendo to grow margins while maintaining its mass-market appeal.

Pokémon IP remains a revenue powerhouse for Nintendo. The Pokémon franchise continues to deliver significant value across gaming and merchandise. Co-owned by Nintendo, Game Freak, and Creatures, Pokémon Scarlet & Violet have sold approximately 27 million copies, becoming the second best-selling titles in the franchise’s history, despite early technical challenges. Support from Switch 2 optimizations and the continued popularity of the Pokémon card market, including Pokémon TCG Pocket, have reinforced the brand’s momentum. The Pokémon Company’s multigenerational appeal and sustained demand, generates a high-margin and recurring revenue stream for Nintendo, contributing to earnings visibility even as hardware cycles and platform dynamics evolve.

Strategic approach to game development. In response to rising development costs and longer production timelines, Nintendo is adopting a more disciplined, cost-aware approach to software creation. By exploring shorter development cycles and more focused project scopes, the company aims to preserve its creativity while mitigating financial risk. Rather than relying solely on price increases to offset higher costs, Nintendo is investing in development efficiency and resource optimization, allowing it to deliver innovative games that remain accessible to a broad player base. This value-driven model helps avoid ballooning budgets that could strain margins, ensuring the company maintains both profitability and creative flexibility.

FY25 results. Nintendo’s profit for FY25 through March totalled 278.8 billion yen (US$1.9 billion), down from 490 billion yen the previous fiscal year. Annual sales slipped 30% to 1.16 trillion yen. Nintendo forecast a 300 billion yen (US$2.1 billion) profit for FY26, up nearly 8% YoY, on sales of 1.9 trillion yen.

Market consensus

(Source: Bloomberg)

Moody’s Corp (MCO US): Stable, scalable and diversified

Moody’s Corporation is a credit rating, research, and risk analysis firm. The Company provides credit ratings and related research, data and analytical tools, quantitative credit risk measures, risk scoring software, and credit portfolio management solutions and securities pricing software and valuation models.

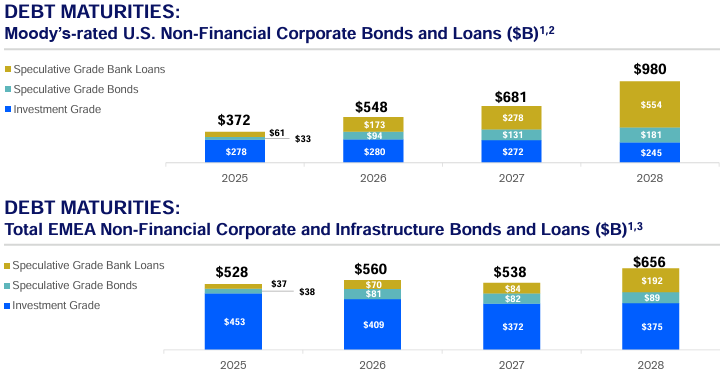

Strong prospects for bond issuance. From 2025 to 2028, over US$4 trillion in debt is expected to mature across the United States, Europe, the Middle East, and Africa. This large-scale wave of debt maturities is expected to drive refinancing and new debt issuance activities, providing Moody’s with a stable and predictable source of business, which is likely to support the continued growth of its credit rating and financial analysis services.

(Source: Moody’s)

Rate cuts create a favorable macroeconomic environment. According to the CME FedWatch tool, the market currently anticipates a 67.8% probability that the Federal Reserve will cut interest rates by 25 basis points in September 2025, indicating a general expectation that monetary policy will begin to shift towards easing.

Resilient, diversified revenue streams. Despite a slightly lowered full-year outlook, Moody’s Q1 highlight the strength of its diversified, service-centric model. Both Moody’s Analytics’s (MA) recurring revenue, which accounts for 96% of its total revenue, grew 9% YoY, underpinned by 12% growth in Decision Solutions and 8% overall revenue growth, demonstrating the success of its strategic pivot toward subscription-based offerings. Annualized recurring revenue (ARR) rose to US$$3.3bn, reflecting continued demand for data-driven risk and decision solutions. Simultaneously, Moody’s Investors Service (MIS) posted its highest-ever quarterly revenue of US$1.1bn, driven by an 8% rise in transactional revenue and strong momentum in investment-grade corporate finance and structured finance, particularly in private credit-related transactions. As investor appetite for high-quality and private credit assets persists, Moody’s resilient revenue base, anchored by recurring subscriptions and broad market exposure, positions it well to navigate macro uncertainty and sustain long-term growth.

1Q25 results. Moody’s Corp delivered an 8% increase in revenue to US$1.92bn, beating estimates by US$40mn. Non-GAAP Earnings per share was US$3.83, beating estimates by US$0.29. The company lowered its full-year 2025 guidance with expectations of revenue growth in the mid-single digits and an adjusted operating margin between 49% and 50%. It anticipates adjusted diluted EPS for the year to range from US$13.25 to US$14.00. Moody’s also plans to repurchase at least US$1.3bn in shares and expects free cash flow between US$2.3bn and US$2.5bn.

Trading Dashboard Update: Add Goldwind Science & Technology Co Ltd (2208 HK) at HK$7.40, JPMorgan Chase (JPM US) at US$289 and Moody’s Corp (MCO US) at US$498. Cut loss on Air China Ltd (753 HK) at HK$5.6.

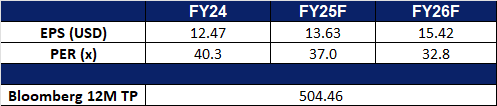

(Source: Bloomberg)

(Source: Bloomberg)

(Source: Bloomberg)

(Source: Bloomberg)