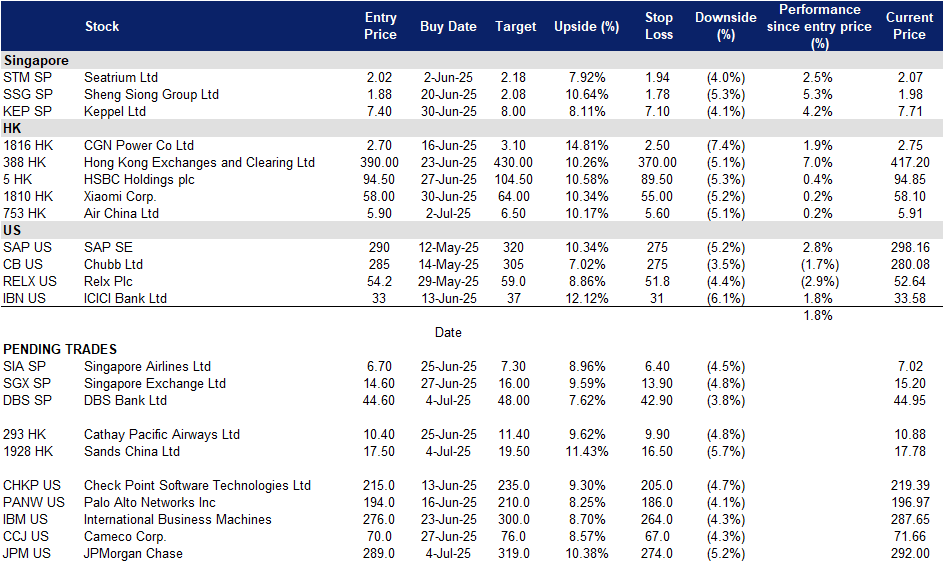

DBS Group Holdings Ltd (DBS SP): Boosting customer growth, one cashback at a time

BUY Entry – 44.6 Target – 48.0 Stop Loss – 42.9

DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

Safe-haven appeal and market volatility driving growth. DBS stands to benefit from Singapore’s growing status as a financial haven amid global uncertainties, including U.S. economic concerns, trade tensions and a weakening USD. The strengthening SGD, combined with an inverse correlation to the STI, makes Singaporean assets more attractive to international investors. DBS, with its dominant local presence, saw market trading activity more than double in Q1, its highest in 12 quarters, driven by FX, interest rate and equity derivatives. Ongoing macro volatility and capital inflows into Singapore will likely boost DBS’s trading and wealth management income.

Strengthening digital ecosystem and brand loyalty. Through its SG60 campaign, DBS/POSB is driving increased engagement and transaction volume with initiatives like the weekly S$3 cashback, S$0.60 and S$6 meal deals, and eVoucher rewards via PayLah! and POSB cards. Running from July to September, these offers aim to ease cost-of-living pressures and encourage digital payments at over 22,000 heartland merchants. This initiative not only reinforces DBS’s community presence but also deepens user adoption of its digital platforms and payment products, supporting fee-based income and customer retention.

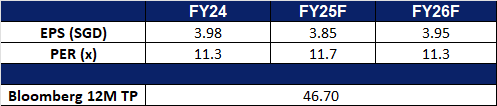

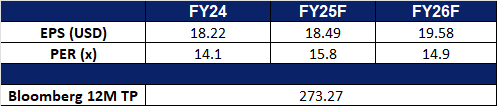

1Q25 Business Updates. Total income for 1Q25 rose 6% YoY to a record of S$5.91bn from broad-based business growth, while net profit fell 2% YoY to S$2.90bn, due to the impact of the 15% global minimum tax, with return on equity at 17.3%. The board declared a total dividend of S$0.75 per share for the first quarter.

Market consensus

(Source: Bloomberg)

Keppel Ltd (KEP SP): Powering a smart and greener future

Keppel Limited is an asset manager and operator. The Company focuses on sustainability solutions spanning the areas of energy and environment, urban development, and digital connectivity, as well as provides critical infrastructure and services through its investment platforms and asset portfolios. Keppel serves clients worldwide.

New 5-year partnership. Keppel’s partnership with the Asian Infrastructure Investment Bank (AIIB) to mobilize up to US$1.5bn for sustainable infrastructure projects across Asia-Pacific enhances its position as a leading asset manager in the region. The five-year collaboration will focus on green, technology-enabled, and connectivity-driven infrastructure, including renewable energy, urban services, and power transmission. This aligns with Keppel’s strategy to capitalize on rapid urbanization, digitalization, and energy transition in Asia. By leveraging AIIB’s financial strength and Keppel’s operational expertise, the partnership is expected to drive long-term growth in Keppel’s infrastructure fund portfolio.

District cooling system expansion into healthcare. Keppel is exploring the integration of its upcoming district cooling system (DCS) plant in Jurong Lake District with Ng Teng Fong General Hospital and Jurong Community Hospital. If implemented, it would mark Singapore’s first DCS deployment in a healthcare redevelopment, enhancing energy efficiency, operational resilience, and freeing up critical space for patient care. This positions Keppel as a frontrunner in sustainable infrastructure for mission-critical sectors, with potential to scale DCS solutions regionally amid rising demand for low-carbon urban utilities.

Strategic energy partnership with Huawei. Keppel Infrastructure’s collaboration with Huawei aims to co-develop solar PV and battery energy storage solutions across Southeast Asia, targeting interconnected power grids, data centres, and industrial parks. With real-time system monitoring and a smart demand response programme, the initiative enhances grid stability and renewable energy efficiency. As Southeast Asia accelerates its energy transition, this partnership strengthens Keppel’s position as a regional leader in smart, low-carbon energy infrastructure with long-term growth potential.

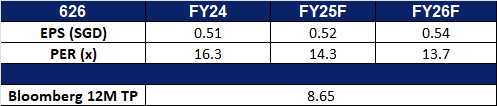

1Q25 Business Updates. Keppel reported 25% YoY growth in net profit, excluding legacy O&M assets, driven by strong and steady performance in the infrastructure segment, higher contributions from the real estate segment, and stronger performance in asset management. Recurring income made up more than 80% of Keppel’s 1Q25 net profit, excluding legacy assets. Asset management fees rose 9% YoY to S$96 million, from S$88 million in 1Q24.

Market consensus

(Source: Bloomberg)

Sands China Ltd. (1928 HK): Summer and concert crowd

BUY Entry – 17.5 Target – 19.5 Stop Loss – 16.5

Sands China Ltd is an investment holding company principally engaged in the development and operation of resorts. The Company operates its business through six segments. The Venetian Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Londoner Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Parisian Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Plaza Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Sands Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering and others. The Ferry and Other Operations segment is engaged in the provision of ferry, shuttle bus and other services.

Anticipated Surge in Macau Tourism. China is gearing up for a record-breaking summer travel season, with over 900 million railway journeys expected between July and August. Macau is well-positioned to benefit from this surge, as June casino revenues rose 19% year-over-year amid robust visitor traffic. This momentum is likely to continue through the summer, supported by a strong lineup of premium entertainment events, including Jacky Cheung’s concert in July and G-Dragon’s performance in early August. Increased visitor traffic, particularly in the premium segment, is expected to positively impact Sands China.

Enhanced Brand Visibility Through Strategic Marketing. Sands China is leveraging its multi-year partnership with the NBA to bolster brand presence. As part of the agreement, two preseason NBA games will be held annually at the Venetian Arena in Macau over the next five years. The company will host the 2025 games in October and has launched the “2025 NBA China Games Experience Package,” offering five accommodation tiers at The Londoner Macao. The top-tier packages include exclusive backstage access and dining experiences with NBA Legends. These initiatives are designed to drive traffic and elevate Sands China’s hotel and retail offerings through the global appeal of the NBA brand.

Strategic Partnership to Develop Health Tourism. Sands China has signed a memorandum of understanding with Guangdong-Macau Traditional Chinese Medicine Technology Industrial Park Development Co. Ltd. to position Macau and Hengqin as a leading destination for health tourism. The partnership aims to integrate tourism, traditional Chinese medicine (TCM), and MICE (meetings, incentives, conferences, and exhibitions), in line with the Macau SAR government’s “1+4” economic diversification strategy. This collaboration is expected to support long-term growth in visitor numbers and broaden Macau’s tourism appeal beyond gaming.

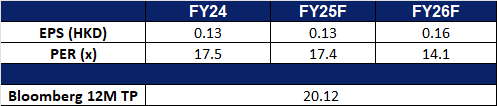

FY24 results review. FY24 revenue rose by 8.36% to US$7.08bn, compared to US$6.53bn in FY23. Net profit rose by 51.0% to US$1.05bn in FY24, compared to US$692mn in FY23. Basic EPS rose to 12.91 US cents in FY24, compared to 8.56 US cents in FY23.

Air China Ltd is a China-based company principally engaged in the provision of air passenger transportation, freight transportation, postal transportation and maintenance services in Mainland China, Hong Kong, Macau and foreign regions. The Company operates its businesses through two segments. Airline Operations segment mainly comprises the provision of air passenger and air cargo services. Other Operations segment comprises the provision of aircraft engineering and other airline-related services. The Company is also engaged in domestic and international business aviation businesses, plane business, aircraft maintenance, airlines business agents, ground and air express services related to main businesses, duty free on boards, retail business on boards and aviation accident insurance sales agent business. The Company mainly conducts its businesses in the domestic market and overseas markets.

Summer Travel Season Set to Drive Demand. As China’s 2025 summer travel season kicks off on July 1 and runs through August 31, the tourism sector is bracing for a sharp upswing. Major airports are preparing for a surge in passenger traffic, with outbound travel orders reportedly rising over 50% year-on-year, according to travel agencies. In Shanghai, Pudong and Hongqiao airports are expected to handle 150,000 flights during the two-month period, a 5% increase from last year. Passenger throughput is projected to reach 24.55 million trips, with daily volumes averaging 396,000 — up 7% YoY. Trip.com Group noted visa applications for summer travel have climbed approximately 10% YoY to a three-year high, with demand for destinations such as Italy, Norway, and Germany jumping more than 80%. As a leading Chinese carrier, Air China stands to benefit meaningfully from this robust travel momentum.

Strategic Partnership with Emirates to Broaden Global Reach. Air China has signed a Memorandum of Understanding (MoU) with Emirates to expand their reciprocal interline cooperation. Under this strategic framework, the two airlines will explore reciprocal codeshare arrangements on key trunk routes between China and the UAE, as well as additional destinations beyond Beijing and Dubai. The MoU also includes potential collaboration in cargo operations and frequent flyer programs, aiming to deliver enhanced connectivity and value to both leisure and business travelers. This alliance positions Air China to strengthen its international footprint and capture incremental traffic through synergistic network expansion.

Expanded European Services Amid Soaring Demand. In response to surging demand for European travel, Air China is increasing its capacity to the region for summer 2025. From July 22 to August 26, the airline will boost its Beijing–Geneva route from five to six weekly flights, operated with modern Airbus A350-900 aircraft. Service to Rome will also see increased frequencies. This strategic move aligns with broader efforts among Chinese carriers to rebuild and grow their European networks. Trip.com reports a significant rise in European travel interest, with visa applications up more than 80% YoY. Air China’s expanded service offering is well-timed to capture this seasonal upswing in outbound tourism to Europe.

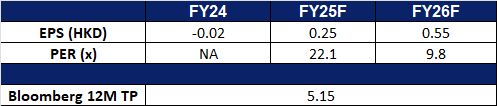

1Q25 results review. 1Q25 revenue fell marginally by 0.11% to RMB40.02bn, compared to RMB40.06bn in 1Q24. Net loss was RMB2.13bn in 1Q25, compared to a net loss of RMB1.71bn in 1Q24. Basic EPS fell to RMB(0.12) in 1Q25, compared to RMB(0.11) in 1Q24.

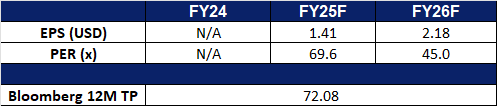

Market consensus.

(Source: Bloomberg)

JPMorgan Chase & Co (JPM US): No stress

BUY Entry – 289 Target – 319 Stop Loss – 274

JPMorgan Chase & Co. provides global financial services and retail banking. The Company provides services such as investment banking, treasury and securities services, asset management, private banking, card member services, commercial banking, and home finance. JP Morgan Chase serves business enterprises, institutions, and individuals.

Strengthened capital return program. JPMorgan Chase has announced a planned dividend increase to US$1.50 per share, up from US$1.40 and authorized a substantial US$50bn share repurchase program following its successful completion of the Federal Reserve’s 2025 stress test. This robust capital return strategy reflects JPMorgan’s strong financial position, continued regulatory compliance and ongoing commitment to returning value to shareholders. The move also reinforces investor confidence in the bank’s operational resilience and disciplined capital management amid broader macroeconomic uncertainty.

Continued resilience of large U.S. banks. Despite a less stringent stress-testing framework in 2025 due to a weaker global economy, all 22 major U.S. banks, including JPMorgan, remained well above regulatory capital thresholds, reaffirming the sector’s resilience. JPMorgan in particular stands out with a strong first quarter CET1 ratio of 15.4% and US$1.5tn in liquidity, enabling it to comfortably absorb economic shocks. While the Fed’s scenario excluded some systemic risks like private credit exposure, the results still validate JPMorgan’s financial robustness and support its continued dividend increases and share repurchases, further demonstrating its ability to navigate an uncertain economic environment.

Volatility driven trading tailwinds. Ongoing global market volatility has significantly benefited JPMorgan’s trading business, with Q1 Markets revenue surging to a record US$9.7bn, driven by exceptionally strong equities performance. As geopolitical risks escalate, particularly with the recent Middle East tensions and the U.S. set to reimpose steep tariffs on 9 July, market fluctuations are likely to persist throughout the year. This backdrop positions JPMorgan to continue capturing elevated trading activity and capital markets demand, further boosting its fee-based income and reinforcing its role as a market leader in volatile environments.

1Q25 results. Revenue increased by 9.7% YoY to US$46bn, exceeding expectations by US$1.86bn. The non-GAAP earnings per share were US$4.91 beating expectations by US$0.27. It expects net interest income for the full year 2025 to be approximately US$94.5bn.

Market consensus

(Source: Bloomberg)

Cameco Corp. (CCJ US): Long-term tailwinds for nuclear power and uranium supply

Cameco Corporation explores, develops, mines, refines, converts, and fabricates uranium. The Company offers uranium for sale as fuel for generating electricity in nuclear power reactors. Cameco operates worldwide.

Surging U.S. electricity demand. U.S. electricity consumption is projected to hit all-time highs in 2025 and 2026, driven by explosive demand from AI and crypto-powered data centers, as well as rising residential, commercial and industrial usage, according to the U.S. Energy Information Administration (EIA). With fossil fuels facing regulatory headwinds and renewables limited by intermittency, nuclear energy remains the only scalable, zero-emission baseload option. As the grid grows increasingly power-hungry, utilities will require long-term uranium supply to maintain reliability. This structural demand shift toward power generation and uranium production in the U.S. will benefit Cameco Corp.

Rising international demand for nuclear. As the global nuclear energy boom accelerates, Cameco is positioned to benefit not just from uranium production, but also from the international commercialization of advanced reactor technology through its 49% stake in Westinghouse. As countries reduce dependence on Russian and Chinese nuclear technology, demand is shifting to Western suppliers. Recent deals, including a Czech AP1000-based reactor project is expected to add US$170mn in Q2 adjusted EBITDA, highlight the earnings power of Cameco’s international exposure. Additional agreements, such as with Finland’s Fortum Corporation, further support long-term value creation. As global demand for clean, secure energy grows and more nations invest in long-term nuclear infrastructure, Cameco stands to realize value across both fuel supply and reactor technology, reinforcing its position in the nuclear value chain.

Renewed U.S. commitment to nuclear development. The announcement of a new 1GW nuclear plant in New York, the first in over 15 years, marks a turning point in U.S. energy policy, reinforcing recognition of nuclear’s role in grid stability and decarbonization. Federal actions to streamline nuclear permitting, paired with soaring private sector interest from technological giants like Microsoft, Amazon and Google, signal a multi-decade nuclear buildout. Cameco stands to benefit directly through rising uranium demand, backed by its strategic exposure across the fuel cycle and its ownership in Westinghouse.

Uranium price upside and supply leverage. Uranium prices have climbed to approximately US$78.5/lb, driven by resurgent demand, policy support and constrained supply. The Sprott Physical Uranium Trust’s recent US$200mn purchase, U.S. efforts to restore domestic enrichment capacity and ongoing supply shortfalls from Kazatomprom underscore a tightening market. Cameco is positioned to capture pricing upside and deliver earnings leverage as the uranium cycle strengthens.

Uranium Spot Price

(Source: Bloomberg)

1Q25 results. Revenue grew 24.4% to US$789mn. Non-GAAP earnings per share were US$0.16. For FY25, Cameco Corp plans to produce 18mn pounds (100% basis) at each of Cigar Lake and McArthur River/Key Lake, and 13mn to 14mn kgU in its fuel services segment, as well as continued work to extend the mine life at Cigar Lake. It now expects adjusted EBITDA from its equity investment in Westinghouse to increase by approximately US$170mn. Over the next five years, it expects adjusted EBITDA to grow at a compound annual growth rate of 6% to 10%.

Trading Dashboard Update: Take profit on Jiangxi Copper Co Ltd (358 HK) at HK$16 and CGN Mining Co Ltd (1164 HK) at HK$2.60. Add Air China Ltd (753 HK) at HK$5.90 and Centrus Energy Corp (LEU US) at US$175. Cut loss on Centrus Energy Corp (LEU US) at US$165.