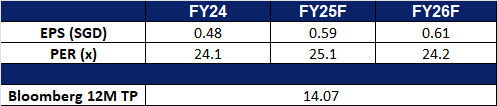

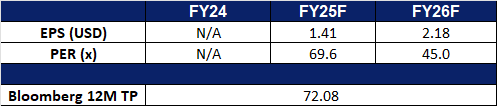

Keppel Limited is an asset manager and operator. The Company focuses on sustainability solutions spanning the areas of energy and environment, urban development, and digital connectivity, as well as provides critical infrastructure and services through its investment platforms and asset portfolios. Keppel serves clients worldwide.

New 5-year partnership. Keppel’s partnership with the Asian Infrastructure Investment Bank (AIIB) to mobilize up to US$1.5bn for sustainable infrastructure projects across Asia-Pacific enhances its position as a leading asset manager in the region. The five-year collaboration will focus on green, technology-enabled, and connectivity-driven infrastructure, including renewable energy, urban services, and power transmission. This aligns with Keppel’s strategy to capitalize on rapid urbanization, digitalization, and energy transition in Asia. By leveraging AIIB’s financial strength and Keppel’s operational expertise, the partnership is expected to drive long-term growth in Keppel’s infrastructure fund portfolio.

District cooling system expansion into healthcare. Keppel is exploring the integration of its upcoming district cooling system (DCS) plant in Jurong Lake District with Ng Teng Fong General Hospital and Jurong Community Hospital. If implemented, it would mark Singapore’s first DCS deployment in a healthcare redevelopment, enhancing energy efficiency, operational resilience, and freeing up critical space for patient care. This positions Keppel as a frontrunner in sustainable infrastructure for mission-critical sectors, with potential to scale DCS solutions regionally amid rising demand for low-carbon urban utilities.

Strategic energy partnership with Huawei. Keppel Infrastructure’s collaboration with Huawei aims to co-develop solar PV and battery energy storage solutions across Southeast Asia, targeting interconnected power grids, data centres, and industrial parks. With real-time system monitoring and a smart demand response programme, the initiative enhances grid stability and renewable energy efficiency. As Southeast Asia accelerates its energy transition, this partnership strengthens Keppel’s position as a regional leader in smart, low-carbon energy infrastructure with long-term growth potential.

1Q25 Business Updates. Keppel reported 25% YoY growth in net profit, excluding legacy O&M assets, driven by strong and steady performance in the infrastructure segment, higher contributions from the real estate segment, and stronger performance in asset management. Recurring income made up more than 80% of Keppel’s 1Q25 net profit, excluding legacy assets. Asset management fees rose 9% YoY to S$96 million, from S$88 million in 1Q24.

Market consensus

(Source: Bloomberg)

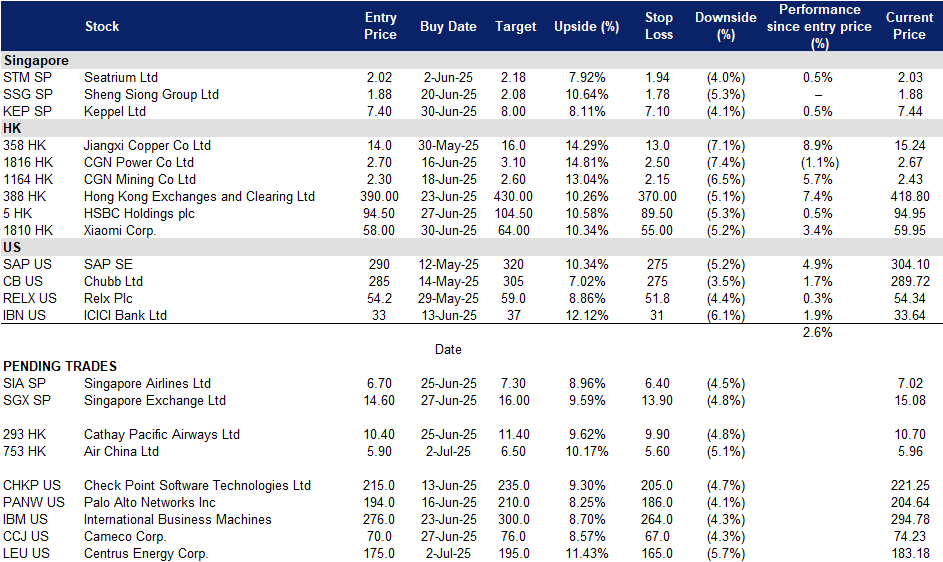

Singapore Exchange Ltd (SGX SP): Improving trading volume and fee income potential

Singapore Exchange Limited owns and operates Singapore’s Securities and derivatives exchange and their related clearing houses. The Company also provides ancillary securities processing and information technology services to participants in the financial sector.

Growing SDR market. The Singapore Exchange (SGX) is seeing strong growth in its Singapore Depository Receipts (SDR) platform, which simplifies access to foreign-listed blue-chip stocks by allowing local investors to trade them in Singapore dollars. With six new SDRs added on 23 June, three from Hong Kong and three from Thailand, the total shelf now covers 21 securities, representing about 50% of the Hang Seng Index and SET50 by weight. Retail interest has surged, with daily turnover hitting a record S$5.4mn in May and total assets under management surpassing S$100mn, over 60% of which is held by more than 7,000 retail investors. The low entry cost and ease of access continue to drive adoption, positioning SGX to benefit from increased trading activity, custody fees and platform engagement, especially among the retail segment. The SDR initiative strengthens SGX’s strategic positioning and enables it to diversify its revenue streams in a scalable way.

Supportive government policies driving growth. The Singapore government, through the Monetary Authority of Singapore (MAS), introduced a series of initiatives to enhance the attractiveness and competitiveness of the local stock market. These include the $5bn Equity Market Development Programme (EQDP), which will partner with fund managers to invest in Singapore equities and streamlined regulations to make the listing process more efficient. Additionally, tax incentives and expanded research grants under the Grant for Equity Market Singapore (GEMS) aim to attract quality IPOs and boost liquidity. These comprehensive measures, coupled with a focus on fostering innovation and sustainability sectors, position the Singapore Exchange as a prime destination for both retail and institutional investors, fostering long-term growth and resilience.

Safe-haven for investors. The weakening of the USD, coupled with tensions in the middle east and global trade uncertainty, has triggered capital inflow to emerging markets like Singapore.Positioned as a safe-haven financial hub, Singapore offers a unique combination of high dividend yields, economic resilience, and a robust regulatory framework. Its ability to weather global economic instability makes the Singapore Exchange a sweet spot for investors looking for stability and capital preservation amidst current market volatility.

1H25 results review. Singapore Exchange Ltd reported 1H25 revenue of S$682.2mn a 15.2% increase from S$592.2mn in the previous period. Its net profit of S$340mn for 1H25, a 20.7% incline YoY, compared to S$281.6mn in 1H24. Earnings per share (EPS) stood at S$0.318, up from S$0.263 in the year-ago period. Due to the Group’s strong performance, the Board of Directors declared an interim quarterly dividend of S$0.09 per share, up from the S$0.085-per-share payout in the previous corresponding period, bringing total dividends for 1H25 to S$0.18 per share.

Market consensus

(Source: Bloomberg)

Air China Ltd. (753 HK): Summer Seasonality

BUY Entry – 5.90 Target – 6.50 Stop Loss – 5.60

Air China Ltd is a China-based company principally engaged in the provision of air passenger transportation, freight transportation, postal transportation and maintenance services in Mainland China, Hong Kong, Macau and foreign regions. The Company operates its businesses through two segments. Airline Operations segment mainly comprises the provision of air passenger and air cargo services. Other Operations segment comprises the provision of aircraft engineering and other airline-related services. The Company is also engaged in domestic and international business aviation businesses, plane business, aircraft maintenance, airlines business agents, ground and air express services related to main businesses, duty free on boards, retail business on boards and aviation accident insurance sales agent business. The Company mainly conducts its businesses in the domestic market and overseas markets.

Summer Travel Season Set to Drive Demand. As China’s 2025 summer travel season kicks off on July 1 and runs through August 31, the tourism sector is bracing for a sharp upswing. Major airports are preparing for a surge in passenger traffic, with outbound travel orders reportedly rising over 50% year-on-year, according to travel agencies. In Shanghai, Pudong and Hongqiao airports are expected to handle 150,000 flights during the two-month period, a 5% increase from last year. Passenger throughput is projected to reach 24.55 million trips, with daily volumes averaging 396,000 — up 7% YoY. Trip.com Group noted visa applications for summer travel have climbed approximately 10% YoY to a three-year high, with demand for destinations such as Italy, Norway, and Germany jumping more than 80%. As a leading Chinese carrier, Air China stands to benefit meaningfully from this robust travel momentum.

Strategic Partnership with Emirates to Broaden Global Reach. Air China has signed a Memorandum of Understanding (MoU) with Emirates to expand their reciprocal interline cooperation. Under this strategic framework, the two airlines will explore reciprocal codeshare arrangements on key trunk routes between China and the UAE, as well as additional destinations beyond Beijing and Dubai. The MoU also includes potential collaboration in cargo operations and frequent flyer programs, aiming to deliver enhanced connectivity and value to both leisure and business travelers. This alliance positions Air China to strengthen its international footprint and capture incremental traffic through synergistic network expansion.

Expanded European Services Amid Soaring Demand. In response to surging demand for European travel, Air China is increasing its capacity to the region for summer 2025. From July 22 to August 26, the airline will boost its Beijing–Geneva route from five to six weekly flights, operated with modern Airbus A350-900 aircraft. Service to Rome will also see increased frequencies. This strategic move aligns with broader efforts among Chinese carriers to rebuild and grow their European networks. Trip.com reports a significant rise in European travel interest, with visa applications up more than 80% YoY. Air China’s expanded service offering is well-timed to capture this seasonal upswing in outbound tourism to Europe.

1Q25 results review. 1Q25 revenue fell marginally by 0.11% to RMB40.02bn, compared to RMB40.06bn in 1Q24. Net loss was RMB2.13bn in 1Q25, compared to a net loss of RMB1.71bn in 1Q24. Basic EPS fell to RMB(0.12) in 1Q25, compared to RMB(0.11) in 1Q24.

Xiaomi Corp is an investment holding company primarily engaged in the research and development and sales of smartphones, the Internet of Things (IoT) and consumer products. The Company conducts its businesses primarily through four segments. The Smartphone segment is primarily engaged in the sales of smartphones. The IoT and lifestyle products segment primarily sells other in-house products (including smart TVs, laptops, artificial intelligence (AI) speakers and smart routers), ecological chain products (including IoT and other smart hardware products) and some consumer products. The Internet Services segment provides advertising services and Internet value-added services such as online games and fintech businesses. The Other segment provides hardware product repair services. The Company is also engaged in smart electric vehicles and other related businesses.

Strong Pre-Orders for Xiaomi’s YU7 SUV. Xiaomi recently announced that its first-ever sports utility vehicle, the five-seater YU7, received approximately 289,000 pre-orders within just the first hour of launch. Starting at 253,500 yuan (around US$35,000), the YU7 has generated strong interest, driven by its competitive pricing—positioned slightly below Tesla’s Model Y—while offering superior specifications and performance. The top-tier variant is priced at 329,900 yuan and features a range of up to 756 km on a single charge, with acceleration from 0 to 100 km/h in just 3.23 seconds. All models come equipped with nine color options, an advanced LiDAR system for enhanced driver-assistance features, and an 800V platform enabling ultra-fast charging. The overwhelming demand is expected to strengthen Xiaomi’s foothold in China’s premium EV segment and contribute positively to the company’s topline growth in the near term.

Expansion of Product Portfolio. In addition to the YU7 launch, Xiaomi has expanded its product lineup with the introduction of AI Glasses in China, priced from 1,999 yuan. Powered by Xiaomi’s proprietary operating system and a Snapdragon AR chipset, the glasses include a high-resolution 12MP camera for capturing real-world content, real-time text translation, and voice-based assistance. This launch underscores Xiaomi’s ongoing push into wearable technology and further enriches its connected device ecosystem. The company also unveiled other new products at its recent Beijing event, including the MIX Flip 2 smartphone and the Xiaomi Pad 7S Pro tablet.

Ongoing Global Expansion. Xiaomi has also made a strategic entry into the South Korean market by opening its first physical retail store at IFC Mall in Seoul. The 200-square-meter outlet showcases a wide range of products, including smartphones, TVs, and robot vacuum cleaners. Despite not being officially open at the time, the store was already attracting strong foot traffic. Located in a high-profile area alongside brands like Dyson, Apple, and near a Samsung Electronics store, this marks a significant milestone following the establishment of Xiaomi’s Korean subsidiary in January. The company plans to further expand its retail presence across South Korea, including new locations in the Gyeonggi region.

1Q25 results review. 1Q25 revenue rose by 47.4% to RMB111.3bn, compared to RMB75.5bn in 1Q24. Profit after tax was RMB10.9bn in 1Q25, up 161.0% YoY, compared to RMB4.17bn in 1Q24. Basic EPS rose to RMB0.44 in 1Q25 from RMB0.17 the same period last year.

Market consensus.

(Source: Bloomberg)

Centrus Energy Corp. (LEU US): Having a competitive advantage

BUY Entry – 175 Target – 195 Stop Loss – 165

Centrus Energy Corp supplies nuclear fuel and services to the nuclear energy industry. The company operates through its Low-Enriched Uranium and Technical Solutions segments. The Low-Enriched Uranium segment consists of two components: sales of separative work units and uranium. The Technical Solutions segment provides engineering, design, and manufacturing services to government and private sector clients. Most of the company’s revenue comes from the Low-Enriched Uranium segment, with significant business operations in the U.S. and other countries, primarily generating revenue from the U.S.

High-assay low-enriched uranium is a bottleneck for nuclear energy. High-Assay Low-Enriched Uranium (HALEU) is uranium fuel with a concentration of 5% to 20% U-235, offering higher energy output while reducing nuclear waste compared to traditional low-enriched uranium. HALEU is suitable for next-generation advanced reactor designs, particularly small modular reactors. The innovation and efficiency improvements in the nuclear industry rely on the application of HALEU, with several countries promoting its research and development. The application for HALEU production licenses is stringent, involving technical, production equipment, and facility factors. The company is the only one licensed by the U.S. Nuclear Regulatory Commission to produce HALEU, which is its competitive advantage.

Backlog Orders Until 2040. As of Q1 2025, the company has a total backlog of US$3.8bn, with delivery deadlines extending to 2040. This includes low-enriched uranium sales agreements worth US$2.1bn and US$900mn in technical support services.

1Q25 results. Revenue increased by 67.3% YoY to US$73.1mn, exceeding expectations by US$498mn. The GAAP earnings per share were US$1.60.

Market consensus

(Source: Bloomberg)

Cameco Corp. (CCJ US): Long-term tailwinds for nuclear power and uranium supply

Cameco Corporation explores, develops, mines, refines, converts, and fabricates uranium. The Company offers uranium for sale as fuel for generating electricity in nuclear power reactors. Cameco operates worldwide.

Surging U.S. electricity demand. U.S. electricity consumption is projected to hit all-time highs in 2025 and 2026, driven by explosive demand from AI and crypto-powered data centers, as well as rising residential, commercial and industrial usage, according to the U.S. Energy Information Administration (EIA). With fossil fuels facing regulatory headwinds and renewables limited by intermittency, nuclear energy remains the only scalable, zero-emission baseload option. As the grid grows increasingly power-hungry, utilities will require long-term uranium supply to maintain reliability. This structural demand shift toward power generation and uranium production in the U.S. will benefit Cameco Corp.

Rising international demand for nuclear. As the global nuclear energy boom accelerates, Cameco is positioned to benefit not just from uranium production, but also from the international commercialization of advanced reactor technology through its 49% stake in Westinghouse. As countries reduce dependence on Russian and Chinese nuclear technology, demand is shifting to Western suppliers. Recent deals, including a Czech AP1000-based reactor project is expected to add US$170mn in Q2 adjusted EBITDA, highlight the earnings power of Cameco’s international exposure. Additional agreements, such as with Finland’s Fortum Corporation, further support long-term value creation. As global demand for clean, secure energy grows and more nations invest in long-term nuclear infrastructure, Cameco stands to realize value across both fuel supply and reactor technology, reinforcing its position in the nuclear value chain.

Renewed U.S. commitment to nuclear development. The announcement of a new 1GW nuclear plant in New York, the first in over 15 years, marks a turning point in U.S. energy policy, reinforcing recognition of nuclear’s role in grid stability and decarbonization. Federal actions to streamline nuclear permitting, paired with soaring private sector interest from technological giants like Microsoft, Amazon and Google, signal a multi-decade nuclear buildout. Cameco stands to benefit directly through rising uranium demand, backed by its strategic exposure across the fuel cycle and its ownership in Westinghouse.

Uranium price upside and supply leverage. Uranium prices have climbed to approximately US$78.5/lb, driven by resurgent demand, policy support and constrained supply. The Sprott Physical Uranium Trust’s recent US$200mn purchase, U.S. efforts to restore domestic enrichment capacity and ongoing supply shortfalls from Kazatomprom underscore a tightening market. Cameco is positioned to capture pricing upside and deliver earnings leverage as the uranium cycle strengthens.

Uranium Spot Price

(Source: Bloomberg)

1Q25 results. Revenue grew 24.4% to US$789mn. Non-GAAP earnings per share were US$0.16. For FY25, Cameco Corp plans to produce 18mn pounds (100% basis) at each of Cigar Lake and McArthur River/Key Lake, and 13mn to 14mn kgU in its fuel services segment, as well as continued work to extend the mine life at Cigar Lake. It now expects adjusted EBITDA from its equity investment in Westinghouse to increase by approximately US$170mn. Over the next five years, it expects adjusted EBITDA to grow at a compound annual growth rate of 6% to 10%.

Trading Dashboard Update: Take profit on OUE Real Estate Investment Trust (OUEREIT SP) at S$0.30. Add Xiaomi Corp (1810 HK) at HK$58 and Keppel Ltd (KEP SP) at S$7.40.