Zixin Group Holdings Ltd (ZXGH SP): Plenty of growth potential

BUY Entry – 0.028 Target– 0.031 Stop Loss – 0.026

Zixin Group Holdings Limited is a holding company. The Company, through its subsidiaries, operates sweet potato biotech-focused value chain focuses on cultivation and supply, product innovation and snacks production, brand building, marketing, and distribution.

Further expansion into Hainan. Zixin Group is expanding its sweet potato value chain from Liancheng County, Fujian, to Lingao County, Hainan, through a Revitalisation Project covering 8,961.33 hectares across 12 villages. This new land in Hainan is significantly larger than their original area in Fujian, offering substantial replication potential. Although currently in the initial stages, the group anticipates realizing profits from this expansion starting in FY2027. This strategic move marks Zixin’s first replication of its model outside Fujian, demonstrating its growth ambitions in the agricultural sector.

Breakthrough in new snack products. Zixin Group recently announced that it has achieved a breakthrough in the production of sweet potato chips and fries snack products. The company has begun to deliver the substantial orders received in February 2025 for these new products from its network of distributors. These products have also received significant demand, and Zixin has ramped up its production capacity at its existing snack manufacturing facility.

Improving margins. Zixin Group saw an improvement in margins YoY in FY2024. The company’s gross profit margin (GPM) rose to 32.0% in FY24, largely attributed to higher sales and lowered costs due to economies of scale. The company also recorded an operating profit margin (OPM) of 6.9% and a net profit margin (NPM) of 4.2%, highest in over 5 years, largely attributed to lower costs relative to revenue. These improving margins showcased the initial results of Zixin Group’s integrated industrial value chain, which includes the supporting industry of cold storage warehousing services, enabling the company to recover from the post-Covid crisis and return to profitability.

1H25 financial results. Zixin Group Holdings reported total revenue of RMB156.7mn in 1H25, representing a 33.1% YoY increase, compared with a revenue of RMB117.8mn in 1H24. The company continues to make strong progress on its integrated circular economy industrial value chain across business operations, driving significant and organic growth in financial performance. Net profit after tax increased to RMB7.73mn in 1H25, compared to a net loss after tax of RMB3.40mn in 1H24. The group’s basic EPS was 0.54 RMB cents in 1H25, compared to a loss per share of 0.25 RMB cents in 1H24.

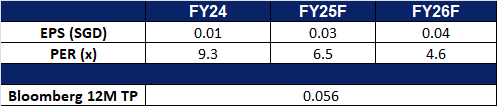

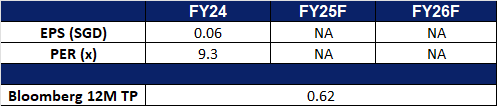

We have fundamental coverage with a BUY recommendation and a TP of S$0.060. Please read the full report here.

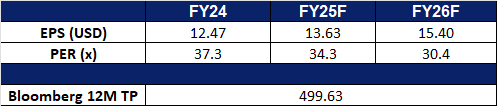

Market Consensus.

(Source: Bloomberg)

Wee Hur Holdings Ltd (WHUR SP): Rate cut expectations

Wee Hur Holdings Ltd provides building construction services and acts as the management or main contractor in construction projects for both private and public sectors. The Company’s clients from the private sector include property owners and developers, and those from the public sector comprise government bodies and statutory boards.

Rate cut expectations. The U.S. bond market is signaling that the Federal Reserve may need to begin cutting interest rates, as evidenced by 2-year Treasury yields falling below the Fed’s policy rate. The spread between the Fed funds rate and 2-year yields—a key market gauge of future monetary policy—has steadily widened over the past two months. This shift reflects a growing consensus among fixed-income investors that the Fed will lower rates by a full percentage point this year, twice the most recent median forecast from Fed officials, amid signs of economic strain linked to President Trump’s escalating tariffs. Markets now anticipate a rate cut as early as June, with additional cuts likely in July or September, totaling three to four reductions by year-end. For Wee Hur Holdings, this environment of declining interest rates presents a potential tailwind: lower borrowing costs could enhance profitability and cash flow, while also creating opportunities to refinance existing debt at more favorable terms, further reducing financial expenses.

Increased construction demand in Singapore. As a BCA-registered A1-grade contractor, Wee Hur is well-positioned to tender for public projects of unlimited value, spanning residential, commercial, industrial, and conservation projects, further solidifying its expertise in the construction sector. The recent sale of its Australian PBSA portfolio has provided the company with additional capital flexibility, enabling it to focus on core segments like construction and dormitories. With Singapore’s construction demand projected to reach S$47bn to S$53bn in 2025, fuelled by major projects such as Changi Airport Terminal 5 and public housing developments, Wee Hur is poised to capitalize on these opportunities. Its diversified capabilities, including expertise in new constructions, refurbishments, and heritage restoration, further enhance its versatility and competitive edge in the market. These strengths position Wee Hur to thrive amid Singapore’s growing infrastructure and construction needs.

Capitalising on sale of assets. Wee Hur Holdings sold its Australian student accommodation assets for A$1.6bn to Greystar, generating S$320mn in cash and retaining a 13% stake worth A$200mn in the new venture. The portfolio, comprising over 5,500 beds, has benefited from high occupancy rates and rising rental income. Wee Hur intends to allocate the proceeds toward expanding its construction and engineering business and exploring alternative investment opportunities. The sale also enabled the company to clear associated debt, strengthening its financial position. Additionally, Wee Hur continues to advance other key projects, including the development of new worker dormitories and student accommodations. Looking ahead, investors are optimistic about the potential for special dividends once the company receives the net proceeds from the transaction, further enhancing shareholder value.

FY24 results review. Total revenue for FY24 fell by 10.7% YoY to S$200.8mn from S$224.8mn. Gross profit for FY24 rose to S$83.0mn, an increase of 54.9% YoY from S$53.6mn in FY23. Profit from continuing operations for FY24 was S$57.0mn, compared to S$160.2mn the year before.

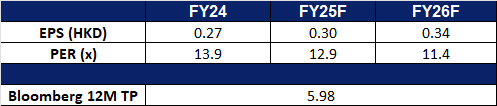

Market Consensus.

(Source: Bloomberg)

AviChina Industry & Technology Co Ltd. (2357 HK): Credibility in China’s defense technology

BUY Entry – 4.05 Target – 4.55 Stop Loss – 3.80

AviChina Industry & Technology Co Ltd is a China-based company principally engaged in the research, development, manufacture and sale of aviation products and relevant engineering services. The Company operates its businesses through three segments. The Aviation Entire Aircraft segment mainly includes providing helicopters, trainer aircraft, general-purpose aircraft and regional jets for domestic and overseas customers. The Aviation Ancillary System and Related Business segment mainly includes avionics products, mechanical electronics, connectors and its accessories. The Aviation Engineering Services segment mainly includes providing planning, design, consultation, construction, operation and other services. The Company mainly operates its businesses in the domestic market.

Increasing conflicts between Pakistan and India. Pakistan and India recently saw an increase in conflicts after a terrorist attack near Pahalgam, Kashmir. This has resulted in an Indian airstrike, followed by a clash between the countries’ fighter jets. The confrontation marks the latest escalation of a decadeslong conflict over Kashmir, which is wedged between the two nuclear-armed nations. This conflict would increase both countries’ defense spending, benefiting aerospace and defense companies in the region, which include China based’s AviChina Industry & Technology.

Strength of China’s aerospace and defense technology. Pakistan’s Deputy Prime Minister Ishaq Dar confirmed that J-10C fighter jets, acquired from China, were deployed in response to recent Indian airstrikes. His remarks follow speculation about the involvement of Chinese-made military hardware in the clashes, during which Pakistan claimed to have downed five Indian aircraft. The reported operational use of the J-10C in active combat marks a significant milestone, enhancing the aircraft’s appeal in the global defense market. A “battle-tested” designation is a notable advantage for military exports, lending credibility and boosting demand. This development also enhances the reputation of China’s defense industry. AviChina, a key player within the broader AVIC (Aviation Industry Corporation of China) ecosystem, stands to benefit indirectly from heightened international interest and improved perceptions surrounding Chinese military aviation technologies.

FY24 results review. Revenue increased by 2.62% YoY to RMB87.0bn in FY24, compared with RMB84.8bn in FY23. Net profit declined by 10.6% to RMB2.19bn in FY24, compared to RMB2.45bn in FY23. Basic EPS fell to RMB0.274 in FY24, compared to RMB0.311 in FY23.

JL Mag Rare-Earth Co Ltd is a China-based company mainly engaged in the manufacture and sale of high-performance NdFeB magnets. The Company is engaged in the research and development, production and sale of high-performance NdFeB permanent magnet materials, magnetic components and the recycling and comprehensive utilization of rare earth permanent magnet materials. The Company’s products are used in new energy vehicles and auto parts, energy-saving variable frequency air conditioners, wind power generation, 3C, robots and industrial servo motors, energy-saving elevators, rail transportation and other fields.

Rare earth export restrictions from China. In the ongoing trade conflict between the U.S. and China, China has made a strategic move by targeting a critical area where the West remains vulnerable: rare earth elements. Apart from tariffs, China has also suspended import licenses for products from six American companies and is tightening its grip on rare earth exports. Rare earth elements (REEs), including neodymium, dysprosium, and terbium, are indispensable in modern technology. They are used in electric vehicle motors, wind turbines, smartphones, semiconductors, and critical military systems such as guided missiles and radar. China currently controls approximately 90% of the global rare earth production, making it a significant player in the supply chain. This dominant position gives China substantial leverage in trade and diplomatic disputes. Furthermore, the export ban could tighten supply for non-U.S. customers as well, allowing JL Mag to command higher prices in markets like Europe, Japan, or Southeast Asia.

Strengthened Domestic Demand and Market Position. China’s recent suspension of exports for seven heavy rare earth metals and rare earth magnets, effective April 3, 2025, has significantly impacted global supply chains, especially in the U.S., which relies heavily on these imports for industries like technology, electric vehicles, aerospace, and defense. This move has redirected demand towards domestic suppliers, bolstering companies like JL Mag. Furthermore, with more policies to drive economic growth in China, demand for rare earth elements domestically is likely to grow as well, benefitting companies like JL Mag.

Ongoing construction of rare earth magnetic materials plant. JL Mag Rare-Earth announced earlier this year plans to invest RMB 1.0bn (USD 143.6mn) in building a new facility in Baotou, Inner Mongolia, dedicated to the production of high-performance rare earth permanent magnetic materials. The plant will support rising demand from emerging sectors such as humanoid robotics and new energy vehicles. Designed with an annual capacity of 20,000 tons, the new factory will increase the company’s total production capacity by 50% to 60,000 tons per year. Construction is expected to take approximately two years.

1Q25 results review. Revenue increased by 14.2% YoY to RMB1.75bn in 1Q25, compared with RMB1.54bn in 1Q24. Net profit increased by 57.9% to RMB160.5mn in 1Q25, compared to RMB101.7mn in 1Q24. Basic EPS increased to RMB0.12 in 1Q25, compared to RMB0.08 in 1Q24.

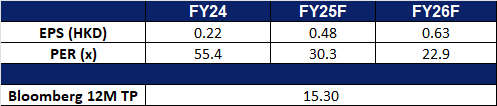

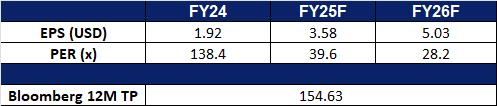

Market consensus.

(Source: Bloomberg)

Moody’s Corp (MCO US): Stable, scalable and diversified

BUY Entry – 460 Target – 500 Stop Loss – 440

Moody’s Corporation is a credit rating, research, and risk analysis firm. The Company provides credit ratings and related research, data and analytical tools, quantitative credit risk measures, risk scoring software, and credit portfolio management solutions and securities pricing software and valuation models.

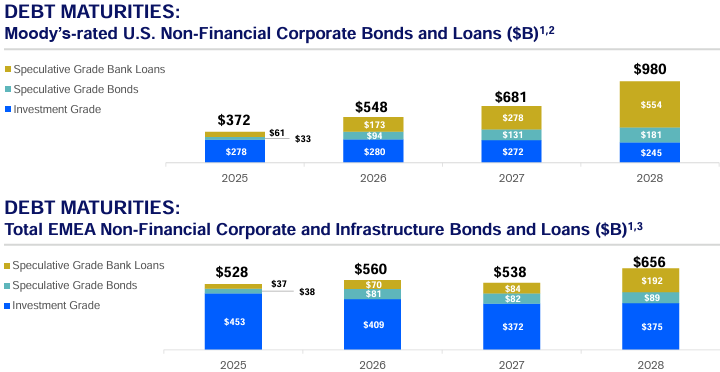

Robust issuance pipeline. More than US$4 trillion in debt maturities expected across the U.S. and EMEA between 2025-2028 will likely fuel refinancing and new issuance activity, providing a steady flow of business for Moody’s.

Launch of independent risk assessments. MSCI and Moody’s have announced a strategic partnership to deliver the first large-scale, independent risk assessment solution for private credit investments. Leveraging MSCI’s extensive private capital data and Moody’s EDF-X credit risk models, will provide transparent, third-party risk assessments at both the company and facility level. As private credit markets expand, the collaboration aims to offer investors standardized tools to benchmark credit risk, inform investment decisions, and monitor portfolios more effectively, while increasing transparency and consistency in the market. The launch is well-timed to capture rising investor demand for private markets.

Resilient, diversified revenue streams. Despite a slightly lowered full-year outlook, Moody’s Q1 highlight the strength of its diversified, service-centric model. Both Moody’s Analytics’s (MA) recurring revenue, which accounts for 96% of its total revenue, grew 9% YoY, underpinned by 12% growth in Decision Solutions and 8% overall revenue growth, demonstrating the success of its strategic pivot toward subscription-based offerings. Annualized recurring revenue (ARR) rose to US$$3.3bn, reflecting continued demand for data-driven risk and decision solutions. Simultaneously, Moody’s Investors Service (MIS) posted its highest-ever quarterly revenue of US$1.1bn, driven by an 8% rise in transactional revenue and strong momentum in investment-grade corporate finance and structured finance, particularly in private credit-related transactions. As investor appetite for high-quality and private credit assets persists, Moody’s resilient revenue base, anchored by recurring subscriptions and broad market exposure, positions it well to navigate macro uncertainty and sustain long-term growth.

1Q25 results. Moody’s Corp delivered an 8% increase in revenue to US$1.92bn, beating estimates by US$40mn. Non-GAAP Earnings per share was US$3.83, beating estimates by US$0.29. The company lowered its full-year 2025 guidance with expectations of revenue growth in the mid-single digits and an adjusted operating margin between 49% and 50%. It anticipates adjusted diluted EPS for the year to range from US$13.25 to US$14.00. Moody’s also plans to repurchase at least US$1.3bn in shares and expects free cash flow between US$2.3bn and US$2.5bn.

Market consensus

(Source: Bloomberg)

Sea Ltd (SE US): Capitalising on Southeast Asia’s e-commerce boom

Sea Limited offers information technology services. The Company provides online personal computer and mobile digital content, e-commerce, and payment platforms. Sea serves customers worldwide.

Capital flowing to emerging markets. The recent weakness in U.S. stocks and the dollar reflects declining confidence in the “American exceptionalism” narrative, with capital gradually flowing into emerging markets. Southeast Asia has become a key beneficiary of this trend. As a leader in the region’s digital economy, the company is well-positioned to capitalize on the benefits of this capital reallocation. In a weaker dollar environment, non-dollar assets become more attractive, and the company’s deep roots in Southeast Asia give it a relative advantage. Additionally, Southeast Asia enjoys structural tailwinds such as a young population, increasing digital penetration, and inflows of foreign capital. These factors make the company’s growth story closely aligned with the capital reallocation trend, positioning it as a standout in the “post-American exceptionalism” era.

Rising tariff pressure to drive Southeast Asian e-commerce growth. As U.S.-China trade tensions intensify, global manufacturers, especially Chinese exporters, are increasingly shifting their focus from the U.S. to Southeast Asia as an alternative market. The U.S. has imposed tariffs of up to 145% on most Chinese imports, forcing Chinese producers to divert surplus goods to regional markets. This has further increased the supply and diversity of goods in Southeast Asia, encouraging consumers to turn to platforms like Shopee. Shopee, as the core business of the company, contributed more than two-thirds of the group’s total revenue in 2024, with annual GMV growing 28% year-on-year to $100.5 billion and total orders increasing by 33%. As global trade dynamics gradually shift away from the U.S., Shopee is well-positioned to capture opportunities arising from this supply-demand restructuring. Management anticipates that GMV will grow by another 20% in 2025, driven by improved profitability and a favorable regional trade environment.

4Q24 results. Sea Ltd delivered a 36.7% increase in revenue to US$4.95bn, beating estimates by US$320mn. GAAP Earnings per share was US$0.39, missing estimates by US$0.05. For FY24, all three businesses delivered strong double-digit growth, exceeding the company’s guidance. For FY25, the company expects Shopee’s full-year GMV to grow around 20% in 2025, with continued profitability improvements. SeaMoney’s loan book is projected to grow meaningfully faster than Shopee’s GMV in 2025, with further SPayLater penetration both on and off Shopee in markets like Indonesia and the Philippines. Garena expects double-digit growth in bookings and user base for 2025, supported by the sustained popularity of Free Fire and new content collaborations.