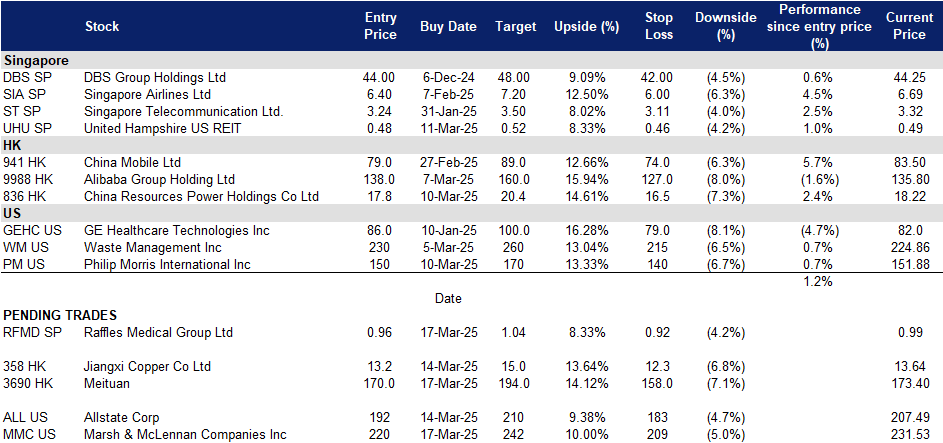

Raffles Medical Group Ltd (RFMD SP): Boosted by expansion opportunities

BUY Entry – 0.96 Target– 1.04 Stop Loss – 0.92

Raffles Medical Group Limited is a health care provider. The Company operates medical clinics, imaging centers, and medical laboratories. Raffles provides general and specialized medical, medical evacuation, medical advisory, and dental treatment services.

Improved confidence and optimistic growth outlook. Raffles Medical Group has demonstrated increased shareholder confidence by revising its dividend policy to distribute at least 50% of its sustainable earnings annually and announcing plans to repurchase up to 100 million shares over the next two years. The company reported a 4.3% increase in net profit to S$31.6 million in the second half of 2024, alongside a 14.8% growth in revenue to S$385.9 million. Despite a 31% decline in full-year net profit due to the cessation of Covid-19 services and reduced government grants, Raffles Medical remains optimistic about its profitability in 2025. The company anticipates continued expansion into new markets and meeting the rising demand for personalized healthcare, supported by its hospitals in Beijing, Shanghai, and Chongqing, which are positioned to drive future growth. Regional revenue in 2024 grew 10.1% to S$65.3 million, bolstered by the growing recognition of the Raffles Hospital brand in China. This demonstrates the company’s resilience and long-term potential in the rapidly expanding healthcare market.

Advantage from China’s policy support. China’s recent policy shift, allowing foreign healthcare providers to fully own hospitals in key regions like Beijing, Shanghai, and Guangzhou, presents a significant opportunity for Raffles Medical Group. This policy change aligns with Raffles Medical’s strategy to expand its footprint in China, capitalizing on its expertise to provide high-quality, personalized healthcare services tailored to both local and expatriate populations. By establishing wholly-owned facilities in China’s growing economic zones, Raffles Medical can strengthen its position in a competitive market, addressing the increasing demand for advanced medical services. However, the group must also navigate regulatory requirements, such as the mandate that at least 50% of healthcare professionals in these hospitals must be from mainland China. By ensuring compliance and integrating international care standards, Raffles Medical can continue its expansion while maintaining high levels of service and reinforcing its brand presence in the Chinese healthcare sector.

Partnership with AIA. Raffles Hospital and AIA Singapore recently signed a memorandum of understanding (MoU) to improve access to healthcare services. Through this collaboration, more than 90 Raffles Hospital specialists will join the AIA Quality Healthcare Partners panel, expanding the network to nearly 700 specialists for AIA HealthShield Gold Max customers. Additionally, both organizations will share quality indicators and patient outcomes to support a value-based healthcare model. The partnership also includes joint management of hospitalization bills for AIA policyholders, ensuring alignment with the Ministry of Health’s fee benchmarks. This initiative is expected to enhance healthcare quality, improve patient access, and provide Raffles Medical with a larger base of AIA HealthShield Gold Max customers, driving higher patient volume.

2H24 results review. Revenue increased by 14.8% YoY to S$385.9 million, primarily driven by strong performance from its hospital services division. Net profit rose 4.3% to S$31.6 million. The hospital services division saw a 4.6% revenue increase to S$345.7 million, while the healthcare services division grew 4.1% to S$295.1 million, though profitability declined. The board proposed a final dividend of 2.5 cents per share, up from 2.4 cents for the year-ago period.

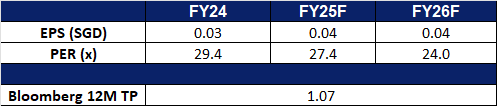

Market consensus

(Source: Bloomberg)

United Hampshire US REIT (UHU SP): Continued growth and expansion

United Hampshire US REIT operates as a real estate investment trust. The Company owns and operates shopping, storage, grocery, and necessity-based retail properties.

Favorable interest rate environment. The Federal Reserve cut interest rates by 25bps in December 2024, bringing the target range to 4.25% to 4.50%. Lower borrowing costs are expected to enhance United Hampshire US REIT’s financial flexibility and support growth. Projections for the Fed funds rate indicate a range of 3.50% to 3.75% by the end of 2025 and 3.25% to 3.50% by the end of 2026.

Strategic divestments. United Hampshire US REIT successfully divested properties, including Lowe’s and Sam’s Club in 2H24 and Supermarket at Albany in January 2025, at over 4% above valuation, demonstrating strong capital recycling efforts.

Strong demand for grocery-anchored strip centers amid limited new supply. Grocery-anchored retail properties remain highly resilient, with grocery store foot traffic increasing 12% from 2019 to 2024, according to Green Street. Service-based tenants, such as coffee shops, salons, and medical centers, further boost footfall, reinforcing the sector’s long-term stability. Hybrid work arrangements have also shifted consumer behavior, increasing demand for localized shopping experiences. Market rent growth for strip centers remained above historical averages in 2024, with a projected 3% annual growth from 2025 to 2029. Investment activity underscores confidence in the sector, Blackstone made its largest retail investment since 2011, acquiring 90 shopping centers for US$4bn, while CBRE expects US$10bn in open-air retail transactions in 2025. Despite strong demand, new strip mall construction remains constrained due to high costs, requiring a 65% rent increase to justify development. This gives existing landlords, including UHU REIT, strong pricing power to negotiate rent increases, securing long-term income growth. With a 97.5% committed occupancy rate and WALE of 8.1 years, UHU REIT is well-positioned to capitalize on these market dynamics.

2H24 results review. Revenue increased 0.4% YoY to US$36.4mn, while net property income dipped 1.6% to US$24.4mn, mainly due to divestments and higher property expenses. DPU declined 4.2% to 2.05 US cents, reflecting higher finance costs.

We have fundamental coverage with a BUY recommendation and a TP of S$0.60. Please read the full report here.

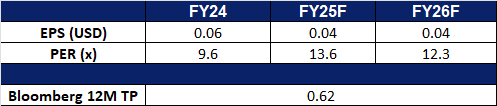

Market Consensus.

(Source: Bloomberg)

Meituan (3690 HK): To benefit from more consumption policies

BUY Entry – 170 Target – 194 Stop Loss – 158

Meituan is an investment holding company mainly engaged in technology retail, providing daily necessities and services through technology and retail fields, including food delivery, in-store, hotel and travel reservations, other services and sales. The Company operates its businesses through two segments. The Core Local Commerce segment includes food delivery, Meituan Instashopping, in-store services, and hotel and travel related businesses. New Initiatives segment includes Meituan Select, Xiaoxiang Supermarket, B2B food distribution and among others. The Company distributes its products within domestic market.

More support for consumption. China’s financial regulator last friday urged institutions to boost support for consumption, promising to properly relax consumer credit quotas and loan terms as it offers long-term backing to make available large sums. It pledged to increase financing support to service industries such as retail, accommodation, catering, tourism, education and healthcare. The National Financial Regulatory Administration (NFRA) also added that it encouraged financial institutions to provide loan renewal support to eligible borrowers of personal consumption loans. These policies are expected to boost China’s consumption level in the near term, and has also improved investors confidence towards China’s consumer market.

Gaining market share. Meituan has established its strong market presence in China, and this has allowed the company to expand aggressively, with growing operations across Asia and the Middle East where it typically enters markets with steep discounts. The company’s subsidiary, KeeTa, also launched in Hong Kong in 2023 and quickly took market share through heavy promotions. The company is also expanding beyond Asia, including to Saudi Arabia, where it’s also upending the market. Furthermore, Deliveroo, one of Meituan’s Keeta competitors in the Hong Kong market, announced that it will close its Hong Kong business due to stiff competition and price wars in Hong Kong from Foodpanda and KeeTa. This further re-emphasize KeeTa’s dominance in the Hong Kong market.

Partnership with Walmart. At the end of 2024, Meituan entered into a new strategic partnerhips with Walmart. The partnership would help Walmart to accelerate its e-commerce business, which currently accounts for nearly half of its China sales. Stores in China have already been connected to Meituan’s delivery ecosystem. In addition to Walmart stores, Walmart China has opened 50 Sam’s Club stores in China, which have benefitted from Chinese consumers increasingly seeking out membership stores. This partnership would also increase delivery volume as well as expand Meituan’s retail offerings for its customers. By integrating Walmart’s stores, including Sam’s Club locations, into its delivery ecosystem, Meituan gains a substantial increase in delivery orders. The partnership allows Meituan to expand its offerings beyond food delivery, incorporating a wider range of retail goods from Walmart. This diversifies Meituan’s platform and attracts a broader customer base, translating to higher transaction volumes and revenue.

3Q24 results review. Revenue increased by 22.4% YoY to RMB93.6bn in 3Q24, compared with RMB76.5bn in 3Q23. Adjusted net profit increased by 124.0% to RMB12.8bn in 3Q24, compared to RMB5.73bn in 3Q23. Number of on-demand delivery transactions also rose by 14.5% to 7.08bn in 3Q24, compared to 6.18bn in 3Q23.

Jiangxi Copper Co Ltd is a China-based company mainly engaged in the mining, smelting and processing of copper and gold. The Company mainly conducts businesses through two segments. The Copper-related Industry segment is mainly engaged in the production and sales of copper and copper-related products. The Gold-related Industry segment is mainly engaged in the production and sales of gold and gold-related products. The Company’s products mainly include cathode copper, gold, silver, sulfuric acid, copper rods, copper tubes, copper foil, selenium, tellurium, rhenium and bismuth. The Company’s products are mainly used in electrical, electronic, light industry, machinery manufacturing, construction, transportation, military industry and other industries. The Company principally conducts its businesses in the domestic market.

Rising copper prices amidst tariffs plays. Copper futures held rangebound around $4.8 per pound recently, hovering near the highest levels since May last year. The announcement of a potential 25% tariff on copper imports by the United States has led to a significant surge in Comex copper prices and increased market volatility. Global copper inventory levels are rising, with a notable increase in Comex stocks due to arbitrage opportunities and anticipation of tariffs, while LME and SHFE inventories show varying trends. Economic uncertainties, including recession fears in the US and deflation in China, are adding to the risks in the copper market, despite ongoing demand from sectors like renewables and technology. The rise in global copper prices is bound to benefit Jiangxi Copper positively.

Copper Prices (1-year)

(Source: Bloomberg)

Expectations of higher copper exports in China. China recently issued more licenses allowing copper smelters to export metal tax-free, aiding local producers and paving the way for greater overseas sales at a time of upheaval in the global market.The license issuances mean that more than a dozen of major Chinese smelters have now been approved for the tolling trade, which involves exporting refined copper that’s been made from imported ore with tax exemptions. Furthermore, with Trump’s announcement of a potential 25% tariff on copper imports by the United States, companies are looking to import more copper before the tariffs kicks in. This is bound to increase copper demand in the near term.

More stake in SolGold and potential access to strategic assets. Jiangxi Copper recently acquired about 157mn shares in SolGold. Following the investment, Jiangxi Copper, through its subsidiary Jiangxi Copper (Hong Kong) Investment Company Limited, would increase its holding in SolGold from 6.95% to 12.19% of the company’s total issued share capital.By increasing its stake in SolGold, Jiangxi Copper gains a larger ownership share and consequently, more influence over SolGold’s decisions. This is particularly important concerning the Cascabel project, a major copper/gold asset. This strategic increase in ownership aligns with JCC’s objective of securing access to vital copper resources.

3Q24 results review. Revenue fell by 6.63% YoY to RMB123.3bn in 3Q24, compared with RMB132.0bn in 3Q23. Net profit fell 13.64% to RMB1.37bn in 3Q24, compared to RMB1.58bn in 3Q23. Basic EPS fell to RMB0.40 in 3Q24, compared to RMB0.46 in 3Q23.

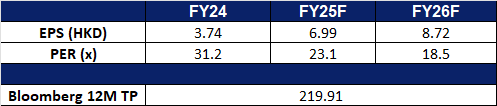

Market consensus.

(Source: Bloomberg)

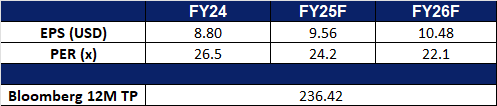

Marsh & McLennan Companies Inc (MMC US): Growth and expansion in focus

BUY Entry – 220 Target – 242 Stop Loss – 209

Marsh & McLennan Companies, Inc. is a professional services firm providing advice and solutions in the areas of risk, strategy, and human capital. Marsh & McLennan offers analysis, advice, and transactional capabilities to clients worldwide.

Rising demand for insurance and risk planning. In the new global trade war macro environment, rising trade costs will prompt businesses to optimize their insurance expenditures, with particular attention to the adverse effects of tariff changes and supply chain disruptions on operations. At the same time, there is an increasing demand for risk control, particularly in geopolitical risk assessment. This benefits the company’s insurance brokerage and risk management services business. The global insurance brokerage industry was valued at US$259.7bn in 2022 and is expected to grow to US$628.3bn by 2032, with a compound annual growth rate (CAGR) of 9.3%.

Positive synergies. The company acquired insurance brokerage and risk management provider McGriff for US$7.75bn, which is expected to generate significant positive synergies. With McGriff’s annual revenue of approximately US$1.2bn, the integration will provide Marsh with more cross-selling opportunities and expand its client base. By leveraging McGriff’s extensive client network and expertise, the company expects overall revenue to grow by 3-5% in the first-year post-acquisition. Excluding amortization, McGriff’s earnings should fully offset the additional interest costs, ensuring a neutral impact on cash flow. Additionally, operational efficiencies and revenue growth from the acquisition are projected to drive long-term earnings accretion of 2-3% annually.

4Q24 results. Revenue rose 9.9% YoY to US$6.1 billion, beating expectations by US$140 million. Non-GAAP earnings per share were US$1.87, beating expectations by US$0.11. The board of directors declared a quarterly dividend of US$0.815 per share on outstanding common stock, payable on 15 May to stockholders of record on 3 April. For FY25, the company expects mid-single-digit underlying revenue growth, with continued margin expansion. It anticipates that the McGriff acquisition will be modestly accretive to adjusted EPS in 2025 and more significantly in 2026. Planned capital deployment for 2025 is set at US$4.5bn.

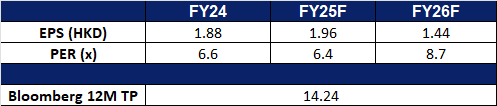

Market consensus

(Source: Bloomberg)

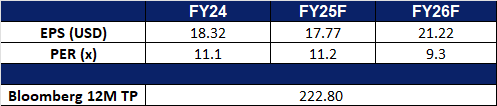

Allstate Corp (ALL US): Active management amid tariff impact

The Allstate Corporation provides property-liability insurance solutions. The Company sells private passenger automobile and homeowners insurance through independent and specialized brokers, as well as life insurance, annuity, and group pension products through agents. Allstate serves customers in the United States and Canada.

Increased concerns about a U.S. recession benefiting defensive sectors. Recent U.S. macroeconomic data shows that inflation remains high, while the labour market is beginning to cool, and consumer spending and confidence are declining. Trump’s tariff policy has triggered a global trade war, and the U.S. stance on the Russia-Ukraine issue has been questioned by its allies. With the concentration of negative factors, the market is averse to uncertainty, so major growth sectors have seen significant corrections, and funds have rotated to stronger defensive sectors.

Tariffs to benefit. Allstate Protection Auto Insurance continues to strengthen margins, with earned premiums rising 9.1% YoY, driven by rate increases. The auto combined ratio improved to 93.5 in 4Q24, reflecting higher premiums and better loss performance. Trump’s tariffs on steel and aluminium could further benefit Allstate by increasing vehicle prices, leading to higher insured values and premiums. Additionally, as consumers hold onto older vehicles longer, insurers may adjust rates to cover rising repair costs, further boosting Allstate’s profitability in the auto insurance sector.

Unlocking value. Allstate continues to optimize its portfolio by divesting non-core businesses and adjusting insurance pricing. The company announced estimated catastrophe losses of US$1.08bn for January, largely due to California wildfires. To streamline operations, Allstate has agreed to sell its Group Health business to Nationwide for US$1.25bn, marking another step in its plan to exit non-core segments. Combined with the earlier sale of Employer Voluntary Benefits, total expected proceeds from these divestitures will reach US$3.25bn, generating an estimated US$1bn financial book gain in 2025. Meanwhile, Allstate is actively adjusting insurance pricing to mitigate risk exposure and improve profitability. In California, homeowners insurance rates rose by an average of 34% in November, with another 30% increase for condo insurance planned in April. Similarly, Illinois homeowners saw about a 14% premium hike in February. These rate adjustments will help Allstate navigate increasing claims costs while bolstering its financial position.

4Q24 results. Revenue rose 11.3% YoY to US$16.51 billion, beating expectations by US$280 million. Non-GAAP earnings per share were US$7.67, beating expectations by US$1.39. The board of directors approved a quarterly common stock dividend of US$1.00, an increase of US$0.08 or 8.7% per share compared to the previous quarter. Additionally, they also authorised a US$1.5bn share repurchase program of outstanding common stock, which will remain in effect through 30 September 2026.

Trading Dashboard Update: Take profit on Zijin Mining Group Co Ltd (2899 HK) at HK$17 and People’s Insurance Company Group of China (1339 HK) at HK$4.35. Cut loss on Geo Energy Resources Ltd (GERL SP) at S$0.30.