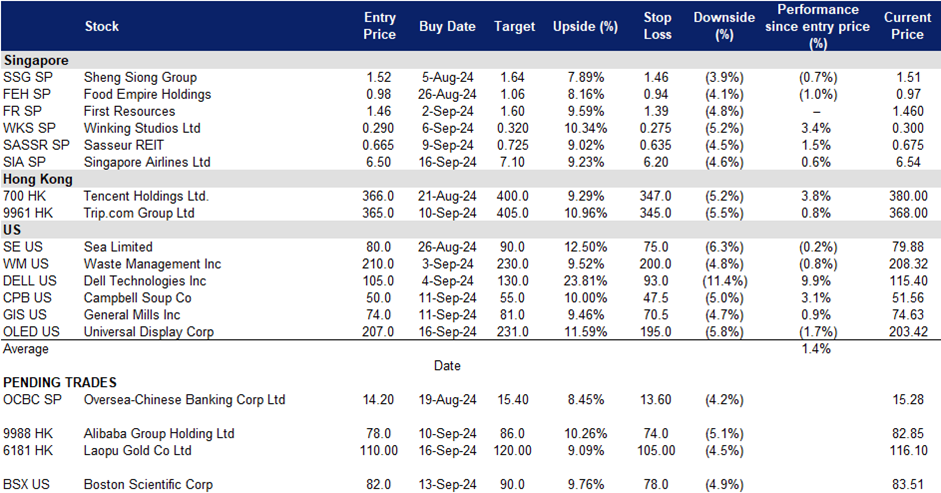

18 September 2024: Singapore Airlines Ltd (SIA SP), Laopu Gold Co Ltd (6181 HK), Universal Display (OLED US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

Singapore Airlines Ltd (SIA SP): Improved margins

- BUY Entry – 6.5 Target– 7.1 Stop Loss – 6.2

- Singapore Airlines Limited provides air transportation, engineering, pilot training, air charter, and tour wholesaling services. The Company’s airline operation covers Asia, Europe, the Americas, South West Pacific, and Africa.

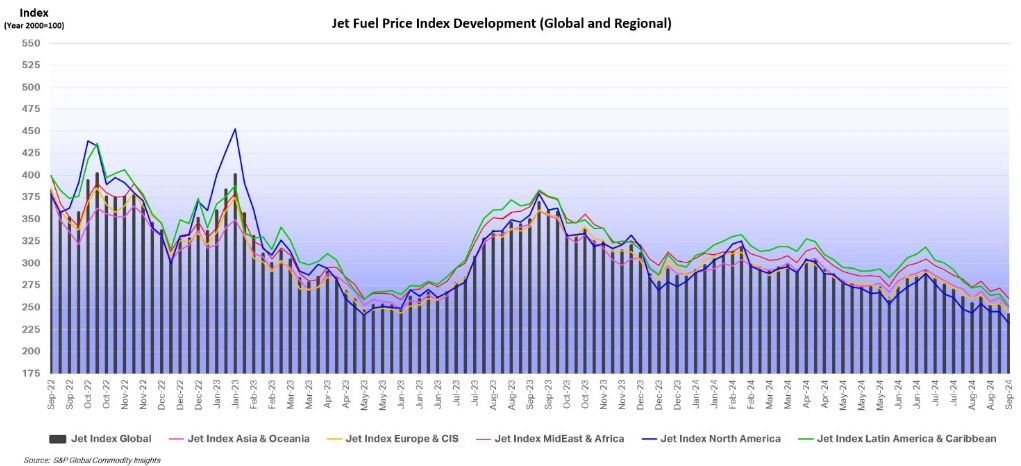

- Continued strong travel demand. According to the International Air Transport Association (IATA) in July 2024, global air passenger demand increased by 8%, reaching a record high, with capacity up 7.4% and a load factor of 86%. International travel grew by 10.1%, while domestic demand rose 4.8%, despite disruptions like the CrowdStrike IT outage. Asia-Pacific saw the highest demand growth at 19.1%, though some routes remain below pre-pandemic levels, while Europe and Latin America also posted strong gains. North America had the highest load factor at 89.4%. IATA highlighted the need to resolve supply chain issues to maintain accessibility and affordability in air travel. With declining jet fuel prices and sustained demand, Singapore Airlines will continue to benefit from improved margins.

Jet Fuel Price Trend

(Source: International Air Transport Association)

- Potential growth in Indian travel market. India has approved Singapore Airlines’ foreign direct investment into the merged Air India-Vistara entity, clearing the final hurdle for the merger. SIA will hold a 25.1% stake in the new carrier with an initial investment of ₹20.6 billion, expected to increase to ₹50.2 billion after completion. Vistara flights will be operated by Air India starting in November 2024. The merger, delayed from its original March target, is expected to close by the end of 2024, giving SIA a significant foothold in India’s rapidly growing travel market.

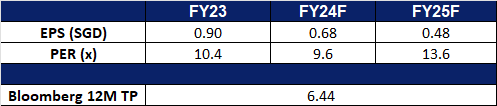

- 1Q25 results review. Total revenue for Q1 increased by 5.3% YoY to S$4,718mn from S$4,479mn in 1Q24. Passenger flown revenue grew 4.1% to S$3.8bn, supported by a 13.8% increase in passengers carried and strong load factors. Net profit saw a 38.4% YoY decline to S$452mn, due to weaker operating performance, a reduction in net interest income, lower surplus on disposal of aircrafts and spare engines, and a lower share of profit from its associated companies.

- Market Consensus.

(Source: Bloomberg)

Sasseur REIT (SASSR SP): REIT-liable portfolio

- RE-ITERATE BUY Entry – 0.665 Target– 0.725 Stop Loss – 0.635

- Sasseur Real Estate Investment Trust operates as a real estate investment trust. The Company invests in a diversified portfolio of retail real estate assets. Sasseur Real Estate Investment Trust serves customers in Asia.

- Stable 1H24 performance. Sasseur REIT reported a 5.1% YoY decline in distributable income per unit (DPU) to 3.153 Scts in 1H24. Despite this, EMA rental income remained stable, delivering RMB329.0mn, a 0.9% YoY growth, equivalent to S$62.3mn, a slight 0.4% YoY decline. This performance aligns with expectations, considering the changes in the treatment of upfront borrowing costs and 20% of the REIT Manager’s base fee to be paid in cash. The 3.9% YoY decline in outlet sales in RMB during 1H24 reflects the higher sales base from 1H23, driven by pent-up demand following China’s economic reopening.

- Shifting consumer dynamics in China. Amid growing consumer caution, outlet sales have seen a modest decline. Sasseur REIT has felt the impact of weaker consumer spending in China, with sales declining YoY, exacerbated by the strong 1H23 base. The slower-than-expected recovery in the Chinese economy has added to consumption uncertainty. However, proactive management efforts, including ongoing tenant mix enhancements, are helping to attract diverse audiences and support portfolio sales performance.

- 1H24 results review. EMA rental income for 1H24 increased by 0.9% YoY to RMB329.0mn from RMB326.0mn. However, unfavourable forex movements led to a slight 0.4% YoY decline in EMA rental income, totalling S$62.3mn. The combination of forex headwinds and declining outlet sales resulted in a 2.9% YoY drop in distributable income to S$42.7mn, with a corresponding decrease in 1H24 DPU to 3.153 Scts. RMB sales for 1H24 declined by 3.9% YoY, reflecting ongoing weakness in the outlet business.

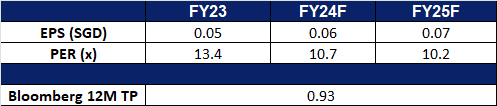

- We have fundamental coverage with a BUY recommendation and a TP of S$0.90. Please read the full report here.

- Market Consensus.

(Source: Bloomberg)

The Hong Kong market is closed today in observance of a public holiday (Mid-Autumn Festival). Trading resumes on Thursday, 19 September.

Universal Display (OLED US): OLED gadgets in demand

- BUY Entry – 207 Target – 231 Stop Loss – 195

- Universal Display Corporation is a member of the United States Display Consortium. The Consortium is a cooperative industry and government effort aimed at developing an infrastructure to support a North American flat panel display infrastructure. The Company and its partners are developing high-resolution, full color, light weight Organic Light Emitting Diode (OLED) technology.

- Demand for notebook and tablet OLED products is growing. OLED adoption is rapidly expanding in mobile PCs. Omdia forecasts a 37% compound annual growth rate in demand for OLED panels in laptops and tablets from 2023 to 2031. This surge reflects a growing number of brands investing in high-end notebooks with OLED displays. Market penetration is accelerating shipments of OLED screen tablets and laptops are projected to reach 12 million and 5 million units, respectively, in 2024. By 2027, these figures are expected to increase to 21 million and 28 million units.

- Strong cash position. As of the second quarter of 2024, the company held US$530.5mn in cash and equivalents, significantly exceeding its total debt of US$24.7mn. This robust cash position demonstrates the company’s strong financial health and ability to generate cash. Free cash flow in the second quarter reached US$57.89mn, approaching the historical peak of US$66.38mn.

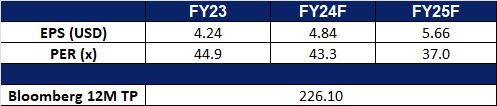

- 2Q24 earnings review. Revenue rose by 8.1% YoY to US$158.5mn, missing estimates by US$1.44M. GAAP EPS was US$1.10, missing estimates by US$0.05.

- Market consensus.

(Source: Bloomberg)

Boston Scientific Corp (BSX US): A growing stock in a defensive sector

Boston Scientific Corp (BSX US): A growing stock in a defensive sector

- RE-ITERATE BUY Entry – 82 Target – 90 Stop Loss – 78

- Boston Scientific Corporation develops, manufactures, and markets minimally invasive medical devices. The Company’s products are used in interventional cardiology, cardiac rhythm management, peripheral interventions, electrophysiology, neurovascular intervention, endoscopy, urology, gynecology, and neuromodulation.

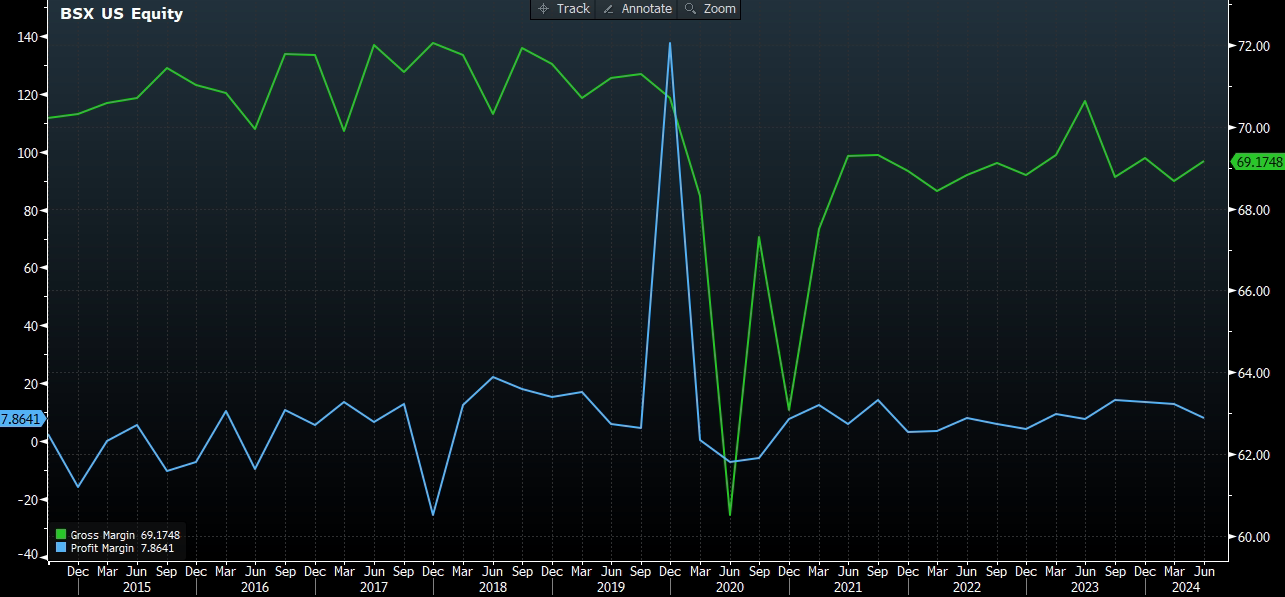

- Exhibits both defensive and growth attributes. Boston Scientific Corp demonstrated remarkable resilience during market downturns supported by strong long-term growth prospects in the healthcare sector. The aging US population and increasing medical needs are driving higher demand for healthcare services and products. The Centers for Medicare & Medicaid Services (CMS) projects national health expenditure growth of 5.6% to outpace GDP growth of 4.3%, rising from 17.3% of GDP in 2022 to 19.7% by 2032. This sustained demand highlights the healthcare sector’s enduring role in economic growth.

- Tailwinds of falling inflation and interest rate cuts. Revenue is expected to grow at an average rate of 10% for the next 3 years from FY25 to FY27, with a 14.25% growth rate expected for FY24. The slowing labour market will lead to a decline in labour costs, which will increase the Boston Scientific’s gross profit and operating profit. As a result of an interest rate cut cycle, the company’s debt costs will fall, reducing its overall interest burden and leading to an improvement in fundamentals. Additionally, as the economy and consumer confidence gradually improve, there will be an increase in demand for medical procedures that require the use of medical devices manufactured by Boston Scientific.

Gross Margin vs Net Profit Margin

(Source: Bloomberg)

- Promising acquisitions. Boston Scientific is making strategic acquisitions to strengthen its business. It plans to acquire Axonics, a maker of devices for urinary and bowel dysfunction, for US$3.7bn, with completion now delayed to the second half of 2024. This acquisition is expected to significantly boost Boston’s urology segment, which contributes about 14% of its sales. Regulatory delays from the FTC may prolong the process. Additionally, in June, Boston Scientific also announced the acquisition of Silk Road Medical for US$1.16bn, expanding its stroke prevention portfolio with Silk Road’s TCAR technology. Both deals are set to close in 2024, with no major impact on earnings expected until 2025.

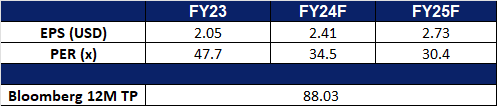

- 2Q24 earnings review. Revenue rose by 14.8% YoY to US$4.12bn, beating estimates by US$100M. Non-GAAP EPS was US$0.62, beating estimates by US$0.04. For Q3, it expects net sales growth to be between 13% to 15% vs estimated growth of 12.09% YoY and adjusted EPS to be $0.57 to $0.59 vs $0.57 consensus. For FY24, it expects net sales growth to be in the range of 13.5% to 14.5% vs estimated growth of 12.38% YoY and adjusted EPS to be $2.38 to $2.42 vs $2.33 consensus.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on Q&M Dental Group Ltd (QNM SP) at S$0.28, Blackstone Inc (BX US) at US$152, Cheniere Energy Inc (LNG US) at US$182.55 and American Electric Power Company Inc (AEP US) at US$104.95. Add Singapore Airlines Ltd (SIA SP) at S$6.5 and Universal Display Corp (OLED US) at US$207. Stop loss on CGN Mining Co Ltd (1164 HK) at HK$1.36.