Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

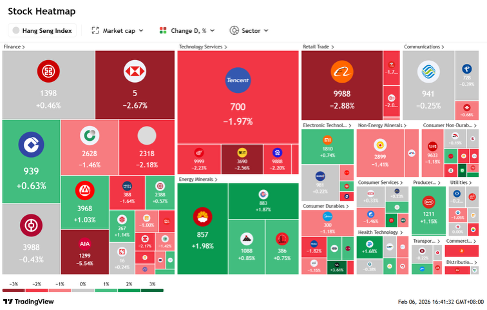

Hong Kong

BUY

Hrnetgroup Ltd (HRNET SP)

RE-ITERATE BUY

Thai Beverage Public Co. Ltd. (THBEV SP)

| Entry: 0.71 Target: 0.81 Stop Loss: 0.66 |

| Hiring Tightness, Cash Buffer, Tech Upside |

| Key Insights |

- Labour market stays tight, so staffing demand does not need a boom to grind higher. Macro conditions in Singapore remain supportive for staffing volumes even if corporates are cautious. Total employment growth in 2025 was 57,300, and unemployment in Dec 2025 stayed at 2.0% overall. Importantly, 26.4% of firms expected to raise wages in the next three months (as of Dec 2025), which usually keeps churn and replacement hiring active. This environment tends to favour flexible staffing as employers keep headcount agile while still needing to fill roles.

- Public sector tech wins are building proof points for Octomate. Since late 2025, management has been pushing HR tech distribution into national workforce infrastructure. One example is EASEJobs integrating with the Careers and Skills Passport, and being one of only three job platforms in Singapore to offer that integration. More recently, Octomate won a workforce management implementation at Outward Bound Singapore for 250 staff, focused on roster scheduling and leave planning. It is not immediately material on its own, but repeated wins plus the ISO IEC 27001 and ISO IEC 27018 certifications strengthen credibility in data security, which is often a gating factor for government linked and regulated customers.

| Entry: 0.45 Target: 0.55 Stop Loss: 0.40 |

| Spirits ballast, beer margin rebuild, and tourism tailwind into 2026 |

| Key Insights |

- “Back to the bar” — tourism and on-premise recovery support volume and mix. Thailand’s Ministry of Finance keeps its 2026 foreign-arrivals forecast at 35.5m, a constructive backdrop for on-premise consumption and premium mix through peak travel windows. Tourist volumes tie directly to beer and spirits sell-out in key urban and resort channels, providing a cyclical lift atop domestic demand..

- Dividend visibility and liability management de-risk the story. FY25 payout stayed steady at THB0.62 DPS with a higher full-year payout ratio 61.4%. The group refinanced with THB38B of debentures in Aug-2025 at 1.72–2.37% coupons and added long-tenor bank lines, smoothing maturities and lowering funding risk. Stable distributions plus cheaper debt support a rerate if operating momentum holds.

BUY

Chow Tai Fook Jewellery Group (1929 HK)

RE-ITERATE BUY

Galaxy Entertainment Group (27 HK)

| Entry: 13.5 Target: 16.5 Stop Loss: 13 |

| Hard luxury rebound with mix driven margin upside |

| Key Insights |

- Demand Inflection. In the quarter ended 31 Dec 2025, Group retail sales value rose 17.8% YoY, with the Mainland up 16.9% and Hong Kong Macau plus other markets up 22.9%. Same store sales also turned decisively positive, up 21.4% in the Mainland and 14.3% in Hong Kong and Macau. This is a clear signal that discretionary appetite for jewellery is recovering even with a high gold price backdrop, which typically pressures unit volumes but supports ticket size.

- Offshore optionality is emerging as a credible second engine. The flagship store in Bangkok and plans on further store openings in Australia and Canada by end June 2026, with Middle East expansion targeted over the next two years are key progress to watch. This is strategically important because it gives the market a second narrative beyond Mainland store density and domestic consumption, and it can also help brand elevation, a key requirement for sustaining fixed price mix and pricing power.

| Entry: 40 Target: 48 Stop Loss: 36 |

| Premium mass leader into a Macau demand reacceleration |

| Key Insights |

- Lunar New Year set up looks better than the market is priced for. January 2026 Macau GGR printed MOP22.633B, up 24% YoY and up 8.35% MoM, an early signal that premium demand and visitation are holding up into peak seasonal periods. This matters because the stock tends to rerate on inflections in monthly GGR and premium mass momentum rather than on long dated forecasts.

- Valuation rerate optionality, consensus upside remains meaningful. Street targets still imply material upside. Sell side consensus on major market data platforms shows an average target around HK$49.24 versus spot around HK$42.3, leaving a double digit rerate path if GGR stays firm and Galaxy Macau keeps premium mass share.

BUY

GE Vernova Inc. (GEV US)

RE-ITERATE BUY

Fluence Energy Inc. (FLNC US)

| Entry: 750 Target: 830 Stop Loss: 710 |

| Vertical powerhouse of the electrification super-cycle |

| Key Insights |

- The AI Energy Anchor. GE Vernova acts as the critical backbone for the AI revolution, utilizing its $150 billion backlog and F-class gas turbines to meet the surging demand for 24/7 “always-on” data center power. By anchoring these hardware sales with high-margin Long-Term Service Agreements (LTSAs), the company transforms traditional equipment cycles into a resilient, software-like recurring revenue stream.

- Vertical Integration and Grid Orchestration. The $5.275bn acquisition of Prolec GE vertically integrates GEV into the high-margin transformer market, securing a critical supply chain bottleneck essential for global grid upgrades. This structural dominance is further fortified by the Xcel Energy Strategic Alliance and the GridOS platform, which lock in multi-gigawatt capacity and position GEV as the “partner of choice” for intelligent grid orchestration.

| Entry: 26 Target: 30 Stop Loss: 24 |

| High density operating system of the global energy transition |

| Key Insights |

- More than just a battery vendor. Beyond hardware, Fluence utilizes AI-driven platforms like Mosaic and Nispera to enable high-margin energy arbitrage and the sub-second grid stability required by power-hungry AI data centres. This software-first strategy positions the company as an indispensable gatekeeper of energy infrastructure, driving long-term recurring revenue and a valuation premium.

- Dominating with the Gridstack Pro. Fluence is effectively leveraging a “Made in America” strategy to capture the burgeoning U.S. utility and AI data center markets.It’s Gridstack Pro dominates the U.S. market by pairing a 30% energy density advantage with a domestic supply chain that qualifies for IRA tax credits. The 1,200 MWh Pioneer project in Arizona serves as a flagship proof-of-concept for this cost-effective, high-density solution to solve critical land-constraint issues for data centres and utilities while mitigating the geopolitical risks of international supply chains.

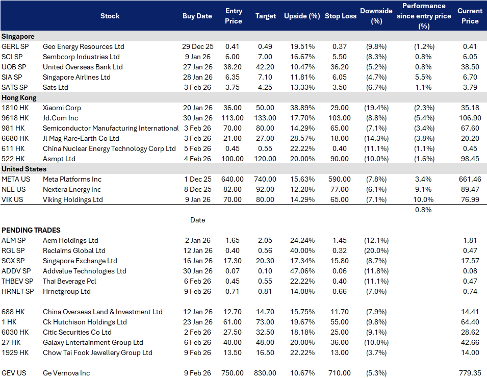

Trading Dashboard Update: Add Coherent Corp (COHR US) at US$185 and Fluence Energy Inc (FLNC US) at US$24 and cut at US$24. Cut Ums Integration Ltd (UMSH SP) at S$1.24, Seatrium Ltd (STM SP) at S$2.05, Astera Labs Inc (ALAB US) at US$140 and Ondas Inc (ONDS US) at US$9. Take profit on Lumentum Holdings Inc (LITE US) at US$500.