Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

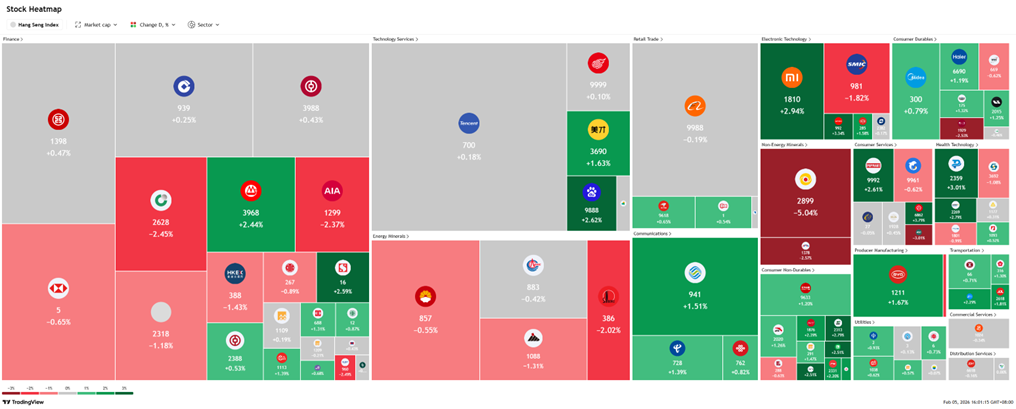

Hong Kong

BUY

Thai Beverage Public Co. Ltd. (THBEV SP)

RE-ITERATE BUY

Addvalue Technologies (ADDV SP)

| Entry: 0.45 Target: 0.55 Stop Loss: 0.40 |

| Spirits ballast, beer margin rebuild, and tourism tailwind into 2026 |

| Key Insights |

- “Back to the bar” — tourism and on-premise recovery support volume and mix. Thailand’s Ministry of Finance keeps its 2026 foreign-arrivals forecast at 35.5m, a constructive backdrop for on-premise consumption and premium mix through peak travel windows. Tourist volumes tie directly to beer and spirits sell-out in key urban and resort channels, providing a cyclical lift atop domestic demand..

- Dividend visibility and liability management de-risk the story. FY25 payout stayed steady at THB0.62 DPS with a higher full-year payout ratio 61.4%. The group refinanced with THB38B of debentures in Aug-2025 at 1.72–2.37% coupons and added long-tenor bank lines, smoothing maturities and lowering funding risk. Stable distributions plus cheaper debt support a rerate if operating momentum holds.

| Entry: 0.068 Target: 0.100 Stop Loss: 0.060 |

| IDRS lead, turnaround momentum, and contract pipeline support 2026 carry |

| Key Insights |

- Real-time LEO ops are moving from nice-to-have to must-have. Earth observation, asset monitoring and responsive space missions increasingly need continuous command, telemetry and payload data outside ground-station passes. Addvalue’s IDRS is advertised as the only space-proven commercial option delivering always-on IP sessions over GEO L-band with session continuity across spot-beam handovers. As more smallsat operators prioritize latency and uptime, attach rates for relay terminals and airtime can rise, supporting recurring service revenue on top of hardware.

- Installed base and airtime scale can compound. AGM disclosures indicate a growing on-orbit terminal base with additional units awaiting launch, which should translate into higher airtime adoption as fleets scale. The combination of new terminals shipped and rising in-service units expands recurring revenue and improves working-capital turns as the model shifts toward services.

BUY

Galaxy Entertainment Group (27 HK)

RE-ITERATE BUY

CITIC Securities Co Ltd (6030 HK)

| Entry: 40 Target: 48 Stop Loss: 36 |

| Premium mass leader into a Macau demand reacceleration |

| Key Insights |

- Lunar New Year set up looks better than the market is priced for. January 2026 Macau GGR printed MOP22.633B, up 24% YoY and up 8.35% MoM, an early signal that premium demand and visitation are holding up into peak seasonal periods. This matters because the stock tends to rerate on inflections in monthly GGR and premium mass momentum rather than on long dated forecasts.

- Valuation rerate optionality, consensus upside remains meaningful. Street targets still imply material upside. Sell side consensus on major market data platforms shows an average target around HK$49.24 versus spot around HK$42.3, leaving a double digit rerate path if GGR stays firm and Galaxy Macau keeps premium mass share.

| Entry: 27.5 Target: 32.5 Stop Loss: 25.0 |

| China deal engine with policy tailwinds and fee leadership |

| Key Insights |

- Policy push and market plumbing support activity. The CSRC’s 2026 work plan prioritises market stability, deeper long-term capital and wider two way opening including QFII optimisation and broader futures access. Recent fine tuning to curb leverage while keeping the rally durable indicates a preference for steady turnover and higher quality issuance rather than boom bust swings. That backdrop is constructive for a scaled franchise that earns across brokerage, underwriting and FICC.

- Fee leadership with diversified engines. CITIC Securities ranked number one in APAC ex Japan investment banking fees in 2025, supported by bond and equity underwriting depth. Scale in asset management and market making augments earnings when primary markets pause and positions the group to capture any revival in IPOs and refinancings.

BUY

Fluence Energy Inc. (FLNC US)

RE-ITERATE BUY

Lumentum Holdings Inc. (LITE US)

| Entry: 26 Target: 30 Stop Loss: 24 |

| High density operating system of the global energy transition |

| Key Insights |

- More than just a battery vendor. Beyond hardware, Fluence utilizes AI-driven platforms like Mosaic and Nispera to enable high-margin energy arbitrage and the sub-second grid stability required by power-hungry AI data centres. This software-first strategy positions the company as an indispensable gatekeeper of energy infrastructure, driving long-term recurring revenue and a valuation premium.

- Dominating with the Gridstack Pro. Fluence is effectively leveraging a “Made in America” strategy to capture the burgeoning U.S. utility and AI data center markets.It’s Gridstack Pro dominates the U.S. market by pairing a 30% energy density advantage with a domestic supply chain that qualifies for IRA tax credits. The 1,200 MWh Pioneer project in Arizona serves as a flagship proof-of-concept for this cost-effective, high-density solution to solve critical land-constraint issues for data centres and utilities while mitigating the geopolitical risks of international supply chains.

| Entry: 450 (buy stop) Target: 500 Stop Loss: 425 |

| Leveraging the AI interconnect bottleneck |

| Key Insights |

- Optics bottleneck and hyperscale network buildouts to drive demand growth. With JLL forecasting nearly 100 GW of new data-centre capacity from 2026-2030 and a 14% CAGR for the global data-centre sector through 2030, optics are becoming the next infrastructure constraint after compute, particularly in AI scale-up and inference workloads. Meta’s multi-year US$6bn fibre deal with Corning reinforces the trend toward massive fibre and transceiver deployment, positioning Lumentum’s high-speed 1.6T transceivers, EML lasers, and optical switching technology for both volume growth and upward pricing as hyperscalers race to interconnect tens of thousands of AI nodes with high-bandwidth optics.

- Strong execution and next-generation optics inflect revenue and margin. Lumentum’s first quarter revenue growth of 58% YoY and more than 1,500bps non-GAAP margin expansion, highlight early success in data-centre optics, with guidance indicating more than 20% sequential revenue growth ahead of broader ramps of optical circuit switches and co-packaged optics. As data-centre capacity grows, its broad optical portfolio will enable Lumentum to capture both near-term demand and long-term growth tied to the global AI infrastructure supercycle.

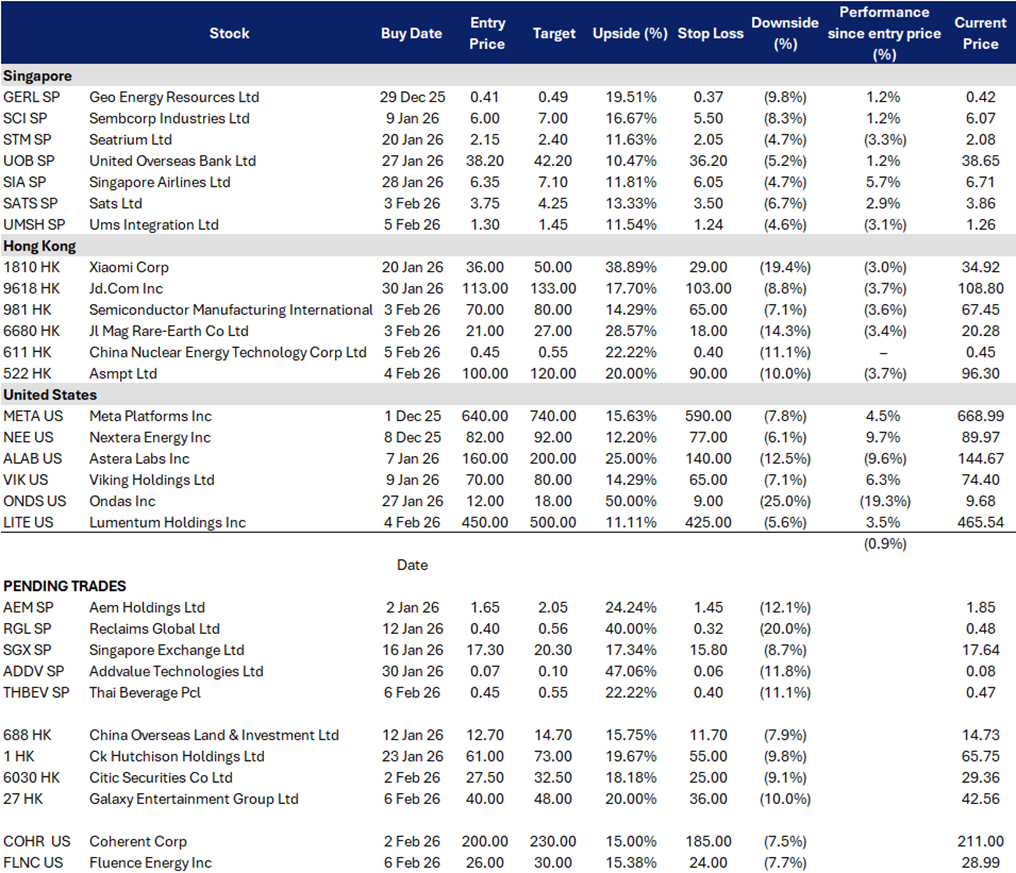

Trading Dashboard Update: Add Ums Integration Ltd (UMSH SP) at S$1.30, China Nuclear Energy Technology Corp Ltd (611 HK) at HK$0.45 and Asmpt Ltd (522 HK) at HK$100. Take profit on Sheng Siong Group Ltd (SSG SP) at S$2.90. Add Lumentum Holdings Inc (LITE US) at US$450. Cut loss on International Business Machines Corp (IBM US) at US$285 and Ionq Inc (IONQ US) at US$36.