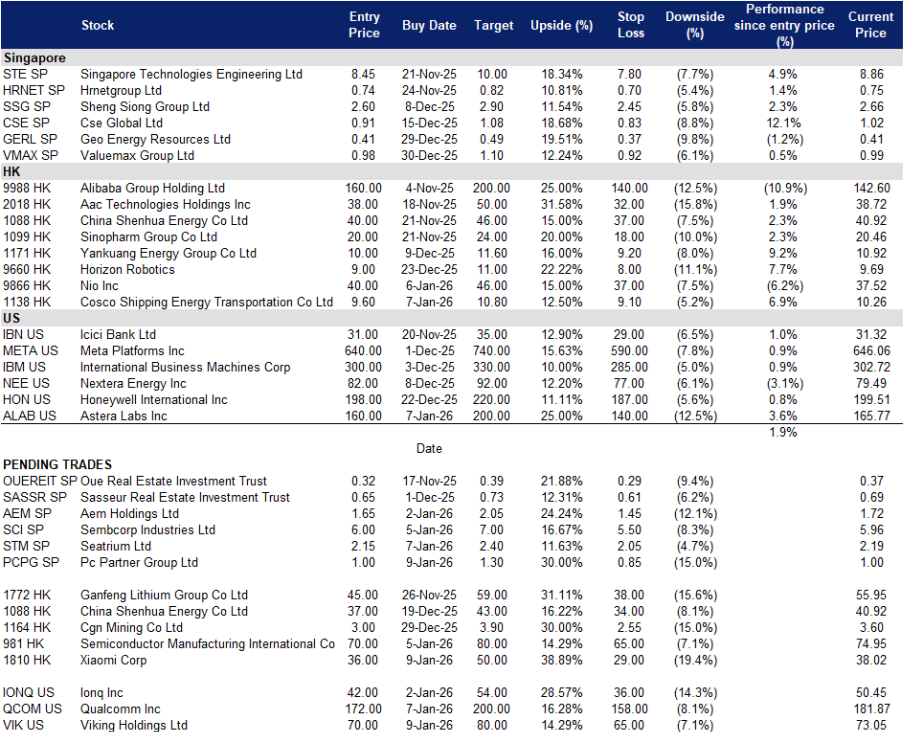

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

PC Partner Group (PCPG SP): RTX 50 Cycle Meets Memory Shock. SGX Pivot Improves Allocation

- BUY Entry – 1.00 Target – 1.30 Stop Loss – 0.85

- PC Partner Group Ltd. is principally engaged in the design, development and manufacture of video graphics cards. The Group manufactures various electronics components and products for customers under its electronics manufacturing services division and also manufactures other personal computers related products.

- Memory supercycle is resetting GPU BOMs and ASPs. Conventional DRAM contract prices are forecasted to jump 55–60% QoQ in 1Q26, with graphics DRAM tightness extending as GDDR6 and GDDR7 are pulled into AI supply chains. Retail prints around CES show DDR5 kits at extreme price points and OEMs flagging broad PC price hikes as RAM scarcity bites. For AICs, this raises bill-of-materials costs but also supports higher street ASPs and favors brands with supply access and pricing power. Net, the setup is mixed for unit volumes yet constructive for own-brand revenue and blended gross dollars through the RTX 50 cycle if allocation holds.

- SGX pivot is already improving allocation and channel reach. Management disclosed that after relocating HQ to Singapore and achieving the SGX listing, the group obtained top-of-the-line RTX 5090 allocation, which helped drive the sharp rebound in own-brand VGA sales in 1H25. The same move broadened Southeast Asia distribution and investor access. We see structural benefits for allocation and marketing efficacy into 2026 as Nvidia’s premium SKUs remain supply-constrained.

- Cycle and capacity catalysts. The RTX 50 desktop refresh, a tighter AIB market that shipped 12.0M units and $8.8B in Q3 2025, and the new Batam, Indonesia facility add volume and mix optionality. If retailer reports of RTX 50 shortages persist due to GDDR7 scarcity, premium SKUs should sustain pricing and brand pull-through for ZOTAC, Inno3D and Manli.

- 1H25 results review. Revenue HK$6,355.3M, +28.5% YoY. Profit attributable to owners HK$250.4M, +29% YoY. Gross margin 10.5% versus 11.3% a year ago as BOM costs rose with mix and scale in brands. Brand VGA revenue HK$4,961.0M, +60.3% YoY; VGA total HK$5,770.3M, +41.1% YoY. Interim dividend HK$0.25 per share paid on 10 Oct 2025.

- KGI has initiated a report which can be found here.

- Market consensus

(Source: Bloomberg)

Seatrium Ltd. (STM SP): Seatrium Oil Security Premium Lifts FPSO Cycle. Order Cover To 2031. Transition Projects Add Balance

- RE-ITERATE BUY Entry – 2.15 Target – 2.40 Stop Loss – 2.05

- Seatrium Ltd offers engineering solutions for the offshore, marine, and energy industries. The Company provides rigs and floaters, repairs and upgrades, offshore platforms, and specialized shipbuilding. Seatrium serves customers worldwide.

- Venezuela disruption tightens heavy supply and keeps offshore spend high. Sanctions escalation and the U.S. blockade have sharply curtailed Venezuelan exports and forced PDVSA to cut production, removing a key heavy supply source and lifting the medium-term premium on reliable offshore barrels in Brazil, Guyana and the Gulf of Mexico. This is supportive for FPSO awards where Seatrium is already the lead contractor on Petrobras P-84 and P-85. A prolonged Venezuelan outage and any eventual rebuild both bias demand toward large yard capacity.

- Diversified backlog and improving mix argue for rerate. Net order book stood at about S$16.6B as of the 3Q update with deliveries through 2031 and a visible pipeline across FPSOs, platforms and grid related systems. Management is targeting better margins via project mix and cost programs after resolving the Brazil legacy probe, which removes a governance overhang. This combination increases earnings visibility without relying on a single segment.

- Offshore wind and grid platforms complement oil and gas cycle. Beyond hydrocarbons, Seatrium is delivering converter platforms for TenneT in the Dutch North Sea and other offshore wind assets in Europe and Asia. These programs diversify the backlog and create medium term balance as energy transition spending resumes.

- 1H25 results review. Revenue S$5.4B, +34% YoY. Net profit S$144M, +301% YoY. Gross margin improved on higher margin projects and efficiencies. Net order book at S$18.6B at end June with deliveries to 2031. Company reiterated progress toward 2028 targets and highlighted stable demand for offshore energy infrastructure and steady activity in offshore wind and repair.

- Market consensus

(Source: Bloomberg)

Xiaomi Corp (1810 HK): AI Phone Upcycle Meets EV Scale, HyperOS Ties The Ecosystem

- BUY Entry – 36 Target – 50 Stop Loss – 29

- Xiaomi Corporation manufactures communication equipment and parts. The Company produces and sells mobile phones, smart phone software, set-top boxes, and related accessories. Xiaomi markets its products worldwide.

- AI devices are recovering and Xiaomi is gaining share. The global smartphone market returned to growth in Q3 2025. IDC and other trackers place Xiaomi at No. 3 with about 43–44M units and ~13–14% share, positioning the brand to monetize the AI handset cycle through 2026. In parallel, Xiaomi is pushing a broad HyperOS 3.0 rollout across two dozen plus models, which should lift engagement, retention, and services monetization into the next upgrade wave.

- EV optionality is scaling and can drive re-rating. Management now targets ~550k EV deliveries in 2026 after a breakout 2025. Pre-orders opened this week for an upgraded SU7 with lidar and quoted range up to 902 km, keeping the brand in the performance conversation and addressing safety scrutiny from 2025 incidents. If execution holds, the EV leg broadens revenue mix beyond handsets and supports a higher ecosystem multiple.

- Ecosystem flywheel across phone, IoT, and car. Deeper HyperOS integration across phones, wearables, home devices, and the vehicle OS increases lock-in and lifetime value. This creates more durable cross-sell pathways than single-category peers and supports services ARPU resilience even when hardware units are choppy.

- 3Q25 results review. Revenue RMB113.1B, +22.3% YoY.Adjusted net profit RMB11.3B, +81% YoY, a quarterly record, helped by mix and operating leverage.

- Market consensus

(Source: Bloomberg)

Semiconductor Manufacturing International Corp. (981 HK): Policy Localisation Plus Record Revenue Outlook Support Mature Node Leadership

- RE-ITERATE BUY Entry – 70 Target – 80 Stop Loss – 65

- Semiconductor Manufacturing International Corporation operates as a semiconductor foundry. The Company provides integrated circuit foundry and technology services including the testing, development, design, manufacturing, packaging, and sale of integrated circuits. Semiconductor Manufacturing International offers its products and services around the world.

- Policy push lifts domestic share and capacity approvals. Beijing has directed that at least 50% of tools used in new wafer capacity be domestically produced. Combined with the Big Fund’s latest capital round, this accelerates approvals and anchors capex for mature nodes where domestic tools are viable. Into 2026, WSTS projects the global semiconductor market to approach about $975B, with Logic and Memory leading. This backdrop supports China localisation and stable demand for SMIC’s core nodes as supply chains rebalance.

- Tailwind on portfolio consolidation and asset quality. SMIC is taking full control of SMNC via a CNY40.6B share deal, simplifying the structure and adding 12-inch capability directly onto the parent balance sheet. The move should improve capital allocation, utilisation planning and disclosure at group level as domestic equipment share increases under the new policy regime.

- Localisation of handset silicon and mature node mix. China smartphone leaders are regaining share and raising domestic content, which supports local foundry demand for modem, RF, power management and application processors on mature processes. While handset shipment trends are uneven, Huawei’s resurgence and ongoing contract wins in China provide a more dependable local order book into 2026.

- 3Q25 results review. Revenue $2.38B, +9.7% YoY, ahead of consensus. Net profit $191.8M, +28.9% YoY. Management and trackers flagged a full year revenue outlook above $9B. Gross margin around 22% with utilisation near 96%.

- Market consensus

(Source: Bloomberg)

Viking Holdings Ltd (VIK US): VIK Fuel Tailwind, K-shaped Demand, And Record Forward Cover

- BUY Entry – 70 Target – 80 Stop Loss – 65

- Viking Holdings Ltd operates as a holding company. The Company, through its subsidiaries, specializes in providing offshore recreational travel services by cruise vessel. Viking Holdings serves customers worldwide.

- Bunker price to remain downtrend. U.S. military intervention in Venezuela and the seizure of its oil sector are poised to fundamentally transform the global energy landscape. By taking control of the country’s oilfields—which house the world’s largest proven reserves at 300 billion barrels—U.S. firms are expected to take over production management. Currently, Venezuela’s output remains significantly underutilized at less than 1 million barrels per day (bpd). A U.S.-led effort to rapidly scale this production could trigger a global supply glut, driving oil prices into a sustained decline. For Viking, these lower fuel costs are expected to bolster net yields and voyage margins through the first half of 2026, providing the financial flexibility to maintain competitive pricing even as itinerary schedules shift.

- Benefit from the US K-shaped economy. The affluent cohort continues to spend despite broader softness. Research on the “K-shaped” backdrop highlights resilient outlays by higher-income consumers in categories like luxury travel. That demand profile aligns with Viking’s guest mix and supports load factors and pricing into 2026 even if mass-market discretionary ebbs.

- Forward cover and capacity. As of Nov 2, 2025, Viking had sold 96% of 2025 capacity and ~70% of 2026, with $5.6B advance bookings for 2025 and $4.9B for 2026, both above prior-year pace. High pre-sold cover de-risks near-term cash generation and supports incremental fleet deployment.

- 3Q25 results review. Revenue $1.99B, +19% YoY; Net income $514M; Adjusted net income $534M. Bookings: 2025 and 2026 advance bookings up 21% and 14% vs prior seasons at same points, respectively; 2026 capacity ~70% sold. As of 2Q25, cash $2.6B, undrawn revolver $375M; deferred revenue $4.4B.

- Market consensus

(Source: Bloomberg)

Qualcomm Inc. (QCOM US): AI PC Ramp Meets Nvidia CES Halo, Auto Pipeline Compounds Edge AI Narrative

- RE-ITERATE BUY Entry – 172 Target – 200 Stop Loss – 158

- Qualcomm Incorporated operates as a multinational semiconductor and telecommunications equipment company. The Company develops and delivers digital wireless communications products and services based on CDMA digital technology. Qualcomm serves customers worldwide.

- CES 2026 sets an “AI everywhere” tone that lifts Qualcomm’s edge story. Nvidia’s CES keynote emphasized “physical AI” and unveiled next-gen platforms for autonomous systems. This keeps investor focus on on-device and vehicle-grade inference, a lane where Qualcomm already ships efficient NPUs in phones and is now scaling AI PCs and automotive compute. In parallel, Qualcomm used CES to expand its Windows-on-Arm lineup with Snapdragon X2 Elite and X2 Plus, signaling broader OEM support and higher NPU TOPS this cycle. The net effect is a stronger demand backdrop for low-power edge AI silicon and attach on connectivity and RF.

- Product moat, platform reach, and hyperscaler pull. Q4 FY25 showed QCT record revenue with Handsets $6.96B, Automotive $1.05B, and IoT $1.81B. For FY25, Automotive and IoT combined grew 27% and total QCT non-Apple revenue rose 18%. Management guided Q1 FY26 revenue to $11.8B–$12.6B with non-GAAP EPS $3.30–$3.50, indicating continued momentum while AI PCs begin to layer in. Qualcomm’s automotive design-win pipeline remains about $45B, supported by programs such as Snapdragon Ride with BMW, which broadens visibility into the late-decade model years.

- RF front-end leadership and PC attach are underappreciated levers. Independent tracking places Qualcomm as the leading RFFE vendor by market share, helped by the integrated modem-RF platform. As AI PCs proliferate in 1H26, Qualcomm’s X-series should drive incremental content across Wi-Fi 7, Bluetooth, audio, and platform power management, supporting blended gross margin resilience even as handset units normalize.

- 4Q25 results review. Revenue $11.27B, +10% YoY. Non-GAAP EPS $3.00, +12% YoY. QCT revenue mix: Handsets $6.96B (+14% YoY), Automotive $1.05B (+17% YoY), IoT $1.81B (+7% YoY). Guidance Q1 FY26: Revenue $11.8B–$12.6B, QCT $10.3B–$10.9B, QTL $1.4B–$1.6B, non-GAAP EPS $3.30–$3.50.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Add Astera Labs Inc (ALAB US) at USD 160 and Cosco Shipping Energy Transportation Co Ltd (1138 HK) at HKD 9.60. Cut First Solar Inc. (FSLR US) at USD 240 and Constellation Energy Corp (CEG US) at USD 325.