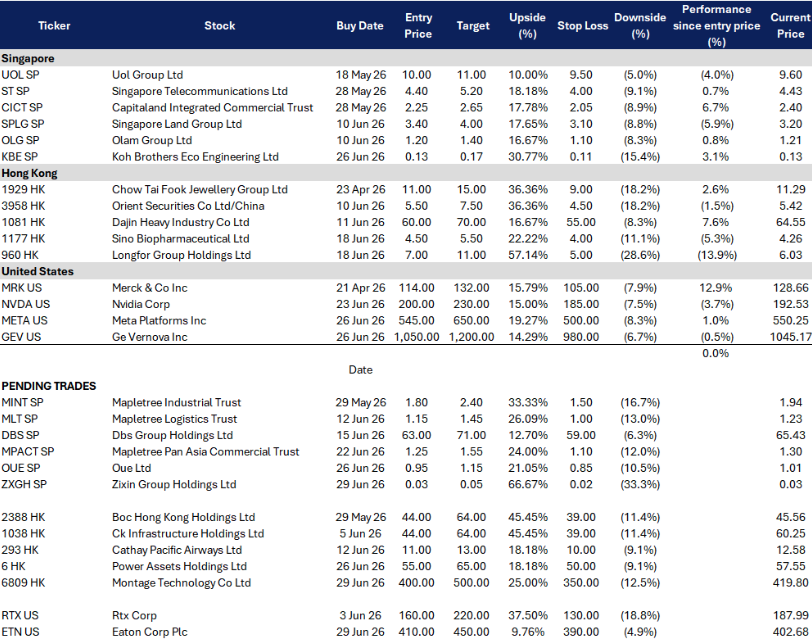

ZXGH SP

Sweet-potato value-chain scaling, Hainan replication, and ODM margin recovery

KEY INSIGHTS #1

Rural revitalisation plus Hainan replication gives Zixin a bigger addressable runway.

The core upside is no longer only Liancheng sweet-potato snacks. Zixin is extending its model beyond Fujian, with Hainan positioned as the first meaningful replication market. The investment case is that Zixin’s integrated model of seedlings, cultivation, processing, cold-chain and waste recovery can be sold into other state-linked or cooperative farmland systems. That turns the story from a small branded-food manufacturer into a repeatable rural-industrialisation platform.

KEY INSIGHTS #2

ODM and processed products can lift revenue quality if margins stabilise.

Zixin’s processed snack and functional-food business remains the higher-quality driver. In 1H FY2026, revenue rose 40.8% YoY to RMB220.6M, driven mainly by processed snacks and functional foods, while net profit more than doubled to RMB16.1M. Gross margin normalised to 30.2% from 33.2%, broadly in line with management’s 30% target, suggesting the market should focus on volume scale and product mix rather than overreacting to some raw-material pressure.

OUE SP

Airport-hotel expansion, REIT recovery, and deep NAV discount

KEY INSIGHTS #1

Crowne Plaza Changi Airport acquisition extends the hospitality platform.

OUE and Tokyo Century announced the acquisition of Crowne Plaza Changi Airport for S$500M, marking their second hotel collaboration at Singapore Changi Airport. This is the clearest near-term corporate action because it deepens OUE’s airport hospitality exposure at a globally relevant travel hub and reinforces management’s willingness to recycle capital into operating assets with tourism and aviation leverage.

KEY INSIGHTS #2

NAV discount is still too wide if asset values stabilise.

OUE reported NAV per share of S$3.85 at end-2025, while the share price is around S$1.05, implying the stock trades at roughly 0.27x P/NAV. The discount is justified by loss-making reported earnings and holdco complexity, but the gap becomes harder to ignore if hospitality improves, finance costs ease, and impairments at associates stop worsening.

6809 HK

Memory-interface scarcity, AI server torque, and China semiconductor scarcity premium

KEY INSIGHTS #1

AI servers are shifting the bottleneck from compute to memory bandwidth.

The cleanest angle is not generic “China chip” exposure, but memory-bandwidth scarcity. AI workloads need faster data movement between GPUs, CPUs and memory, and Montage’s DDR5 / MRDIMM ecosystem is directly exposed to that. Its Gen2 MRCD and MDB chipset supports DDR5 MRDIMM data rates up to 12,800 MT/s, aimed at next-generation computing platforms. That makes Montage a second-order AI infrastructure beneficiary: not the GPU itself, but a critical enabler of higher memory bandwidth.

KEY INSIGHTS #2

H-share listing creates a scarcity premium, but also makes this a high-beta tape trade.

Montage listed in Hong Kong in February 2026, raising about HK$7.04B, with the stock closing 64% above its IPO price on debut. The retail tranche was more than 700x oversubscribed, while the international tranche was more than 37x covered, showing unusually strong institutional and retail appetite for liquid China AI semiconductor exposure. That scarcity premium can persist, but it also means valuation is vulnerable when the AI-chip tape de-rates.

0006 HK

UKPN disposal unlock, defensive utility carry, and balance-sheet firepower

KEY INSIGHTS #1

UKPN disposal crystallises value and gives the balance sheet optionality.

Power Assets is participating in the disposal of UK Power Networks, with HKEX filings showing the transaction was formally announced in February 2026 and followed by an EGM circular in April 2026. This is the key catalyst because UKPN is one of the group’s major UK regulated utility holdings. A successful completion would convert part of embedded asset value into cash, giving Power Assets more flexibility for acquisitions, deleveraging, special distributions, or reinvestment into energy transition assets.

KEY INSIGHTS #2

Low gearing gives M&A firepower in a utility sector where capital is scarce.

The group’s FY2025 recurring profit rose modestly, while third-party summaries of the annual results note net debt to net total capital of about 1% on a corporate basis. That is unusually conservative for a utility/infrastructure investor. In a sector where many peers are still managing higher funding costs, Power Assets’ balance sheet can become an offensive tool rather than just a defensive buffer.

ETN US

Grid-to-chip power infrastructure leader for AI data centres

KEY INSIGHTS #1

Strong orders and Boyd Thermal expand Eaton’s data centre exposure.

Eaton’s 1Q26 sales rose 17% YoY to a record level, while rolling 12-month orders in Electrical Americas increased 42% YoY, primarily driven by data centre demand, supporting its decision to raise 2026 organic growth guidance to 9%-11%. The acquisition of Boyd Thermal also adds liquid-cooling capabilities, allowing Eaton to offer a broader grid-to-chip portfolio covering electrical distribution, power management and thermal infrastructure.

KEY INSIGHTS #2

Rising rack density increases power and cooling content per data centre.

As AI servers become more power-intensive, data centres require substantially more electrical distribution, backup power, power conversion and liquid cooling equipment than traditional facilities. This increases the infrastructure content required per megawatt and supports sustained demand for Eaton’s integrated electrical and thermal solutions as hyperscalers expand AI capacity and modernise power architecture.

GEV US

Full-spectrum beneficiary of AI-driven power and grid investment

KEY INSIGHTS #1

Record orders and backlog provide multi-year growth visibility.

GE Vernova is benefiting across both power generation and grid equipment, with 1Q26 orders reaching US$18.3bn, backlog rising to US$163bn, and management raising its 2026 guidance. Its Electrification segment secured US$2.4bn of data centre equipment orders in one quarter, exceeding the whole of 2025, while the Prolec GE acquisition expands its transformer manufacturing and grid equipment capabilities in North America.

KEY INSIGHTS #2

AI power shortages are accelerating gas generation and grid upgrades.

AI data centres are creating a structural rise in electricity demand that existing grids cannot meet quickly enough, driving simultaneous investment in gas turbines, transmission equipment, transformers and renewable capacity. With data centre electricity consumption expected to more than double over the long term, GE Vernova is positioned across the full power value chain required to generate, transmit and manage this incremental demand.

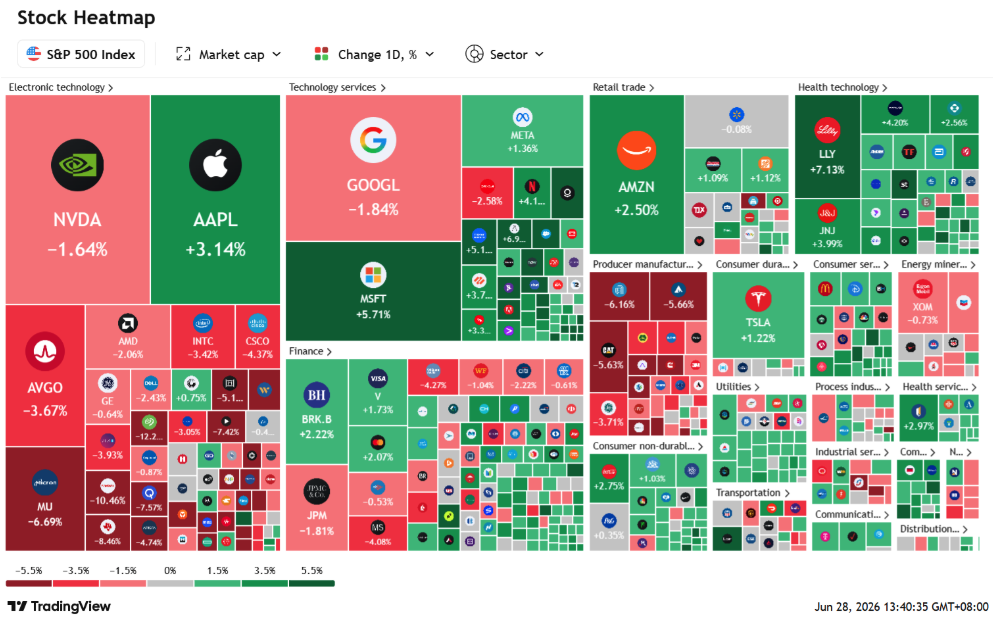

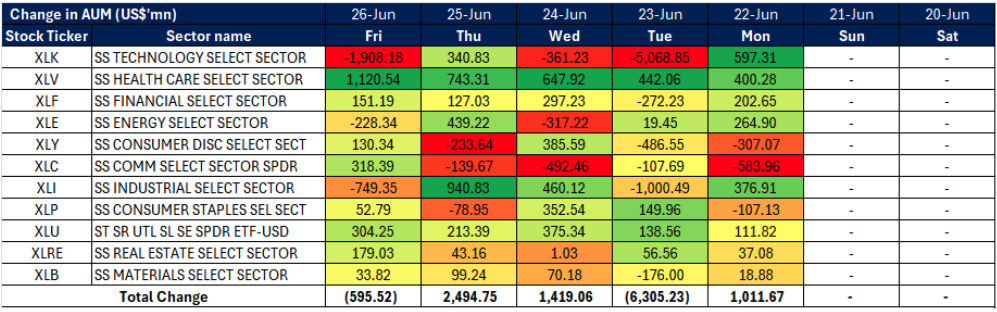

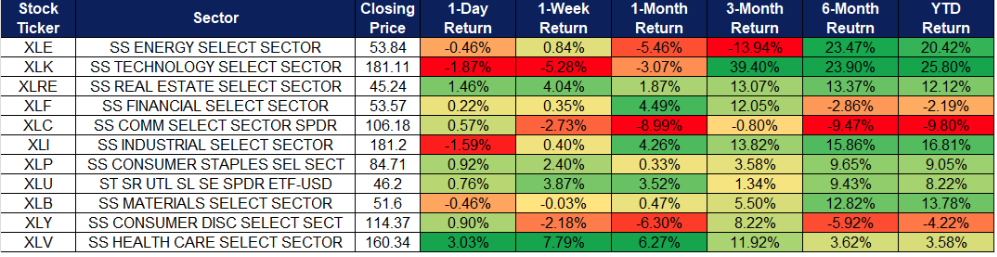

STOCKS

–

STOCKS

STOCKS