Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

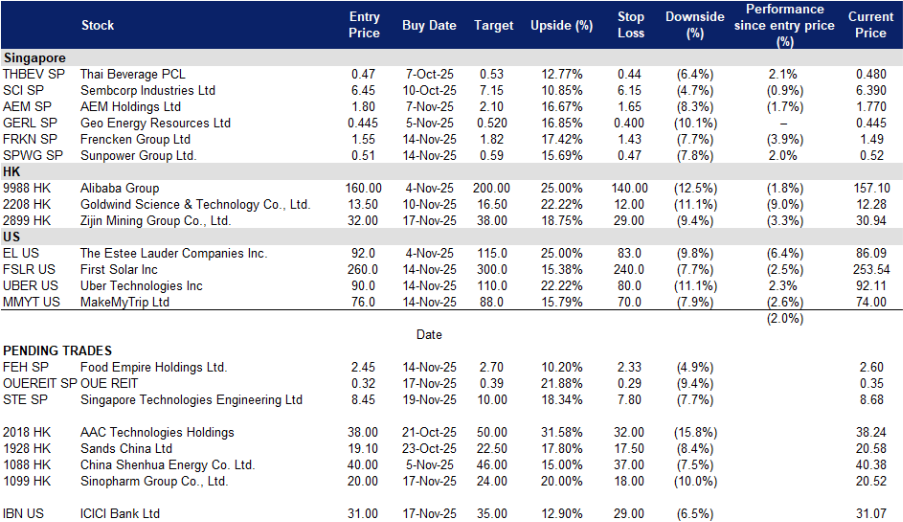

Singapore Tech Engineering (STE SP): Record Order Book, Multiyear Dividend Uplift, Aero Cycle Tailwinds

- BUY Entry – 8.45 Target – 10.00 Stop Loss – 7.80

- ST Engineering Ltd is a global technology, defence, and engineering group. The Company uses technology and innovation to solve problems and improve lives through its diverse portfolio of businesses across the aerospace, smart city, defence, and public security segments. ST Engineering serves clients worldwide.

- Order book at a new high with strong win rate. 9M25 revenue was S$9.1B, +9% y/y, supported by S$14.0B of contract wins year to date and a record S$32.6B order book as at 30 Sep 2025. Visibility is high with S$2.8B slated for delivery in 4Q25. This underpins growth into 2026 across all three segments.

- Commercial aerospace recovery extends the earnings upcycle. Aero revenue grew 11% y/y in 9M25 on strength in engine MRO and nacelles, partly offset by lower PTF. Industry data point to continued passenger demand growth and a tight MRO backdrop as the global fleet expands, supporting volume and mix for ST Engineering’s network.

- Dividend plan and portfolio recycling strengthen total return. The Board declared a 3Q25 interim dividend of 4.0 cents per share and guided for a FY25 final dividend of 6.0 cents plus a special dividend of 5.0 cents subject to approval, implying 23.0 cents total for FY25. Cash proceeds of S$594M from divestments, with after tax gains of S$258M, provide flexibility to fund growth and de leverage while rewarding shareholders. From FY26, ordinary dividends will track one third of y/y net profit increases.

- 1H25 results review. Revenue S$5.92B, +7.2% y/y, EBITDA S$871M, +10.8%, EBIT S$602M, +15.2%, net profit S$403M, +19.7%. Segment revenue growth: Commercial Aerospace +5%, Defence and Public Security +12%, Urban Solutions and Satcom +0.3%. Order book S$31.2B at 30 Jun 2025.

- Market consensus

(Source: Bloomberg)

OUE REIT (OUEREIT SP): Falling Funding Costs + Resilient Singapore Office; Hospitality Steady On Higher RevPAR

- RE-ITERATE BUY Entry – 0.32 Target – 0.39 Stop Loss – 0.29

- OUE Real Estate Investment Trust (OUE REIT) provides real estate investment services. The Company invests in income-producing real estate used primarily for retail, hospitality, and office purposes in financial and business hubs, as well as real estate-related assets. OUE REIT serves customers in Singapore and China.

- Office remains the anchor with high occupancy and positive reversions. Singapore office committed occupancy stood at 97.4% in 3Q25 with +5.6% rental reversion. Average passing rent is S$10.91 psf pm, and Grade A CBD benchmark is S$12.20 psf pm, leaving headroom on renewals. Like-for-like commercial revenue grew +4.2% and NPI +3.8% in 3Q25 on earlier leasing done at higher rents.

- Rates tailwind is visible in the P&L and the balance sheet work. Finance costs fell 19.7% YoY to S$21.6m in 3Q25 as the weighted average cost of debt eased to 4.1%. The REIT refinanced OUE Bayfront with S$830m facilities, including a S$600m Green Loan, issued S$150m 7-year Green Notes at 2.75% due 2032, and lifted green financing to 85.1% of total debt. Pro forma leverage could reduce to 37.7% with full deployment of Lippo Plaza proceeds, and only 16% of debt now matures in 2026.

- Hospitality and Orchard retail add cyclicals without destabilising cash flows. 3Q25 hospitality RevPAR was S$279 (Hilton Singapore Orchard S$293, Crowne Plaza Changi S$251) despite F1 shifting to October. Mandarin Gallery delivered +9.3% rental reversion with 97.4% committed occupancy. Together, these segments diversify income while the office backbone keeps cash generation predictable.

- 3Q25 results review. Revenue and NPI. Revenue S$70.5m (−5.8% YoY; LfL +1.2%). NPI S$57.0m (−5.6% YoY; LfL +2.0%). The YoY headline decline reflects the 2024 Shanghai divestment; Singapore assets grew on a like-for-like basis. Finance costs S$21.6m (−19.7% YoY). NAV per unit S$0.57.

- Market consensus

(Source: Bloomberg)

Alibaba Group Holding Ltd. (9988 HK): Qwen Consumer Launch Drives AI Flywheel, Cloud Growth Accelerating, China Commerce Steady

- RE-ITERATE BUY Entry – 160 Target – 200 Stop Loss – 140

- Alibaba Group Holding Ltd operates as a holding company. The Company, through its subsidiaries, provides internet infrastructure, electronic commerce, online financial, e-commerce, retail, and internet content services via global marketplaces, as well as offers digital media, entertainment, logistics, and cloud computing solutions.

- Qwen App went live Nov 17, day-one traffic spiked, creating a top-of-funnel AI user engine. Alibaba launched the free Qwen consumer app on Nov 17 across iOS, Android, web and PC. Media and data trackers reported heavy user traffic on day one, with some temporary service delays, indicating rapid adoption. The app is positioned as the primary interface to Qwen3 models and a distribution rail for agentic features that can tie back to Taobao, Amap and Cloud workloads. This widens the AI funnel before monetisation via subscriptions, advertising, commerce conversion and incremental cloud usage.

- Cloud growth is re-accelerating as AI demand scales and capex is funded. June quarter 2025 Cloud Intelligence Group revenue rose 26% y/y, with AI-related product revenue posting triple-digit growth for the eighth straight quarter. Alibaba also raised US$3.2B via zero-coupon convertible bonds to expand data centers and AI infrastructure, reinforcing multi-year capacity for model training and inference. This improves visibility on Cloud top line and operating leverage through 2026.

- China commerce is stabilising, while AIDC narrows losses. June quarter revenue was RMB247.7B, +2% y/y or +10% on a like-for-like basis excluding Sun Art and Intime. Customer management revenue in China Commerce grew 10% y/y, helped by take-rate improvements, and AIDC grew 19% y/y with narrowed losses on better unit economics. The next results are scheduled for Nov 25, 2025, where investors will look for continued CMR strength, AIDC breakeven trajectory and early Qwen usage data points.

- 1Q26 results review. Revenue RMB247,652M, +2% y/y. Adjusted EBITA RMB38,844M, −14% y/y on investment in Taobao Instant Commerce. Cloud revenue RMB33,398M, +26% y/y with AI products growing triple-digit for the eighth consecutive quarter. Non-GAAP net income RMB33,510M, −18% y/y. Free cash flow outflow RMB18,815M on cloud infra and quick-commerce spend.

- Market consensus

(Source: Bloomberg)

Sinopharm Group Co., Ltd. (1099 HK): Defensive Demand With NRDL Volume Tailwinds As Pricing Resets

- RE-ITERATE BUY Entry – 20.0 Target – 24.0 Stop Loss – 18.0

- Sinopharm Group Co. Ltd. provides pharmaceutical supply chain services. The Company offers pharmaceutical manufacturing, pharmaceutical distribution, medical devices marketing, logistics and delivery, and other services. Sinopharm Group markets its products throughout China.

- Macro policy and NRDL mechanics favor volume resilience. China’s 2025 NRDL cycle is the most competitive on record, with more than 300 drugs seeking new listings and 200+ up for renewal. The addition of a new Category C pathway aims to expand access for high-value therapies. NRDL inclusion typically trades price for access, which compresses manufacturers’ ASPs but drives distributor volumes. Sinopharm’s breadth positions it to capture that flow as 2025 outcomes roll into 2026 consumption.

- Defensive profile tends to outperform in weak sentiment. Healthcare demand is non-discretionary. Across past slowdowns, defensive sectors, including healthcare, have shown stronger relative performance and lower beta. With global risk appetite rotating toward defensives in 2025, healthcare has re-emerged as a leadership bucket. Against a choppy China tape, Sinopharm’s volume-linked model and dividend support provide downside ballast.

- Fundamentals steady despite pricing pressure. Nine-month 2025 data show revenue RMB431.5B, −2.5% yoy, while net profit attributable to equity holders RMB5.31B, +0.5% yoy. Cost control and operating efficiency offset part of the pricing drag from procurement and reimbursement. Balance sheet scale and diversified payor mix provide cash flow visibility through the NRDL and VBP cycles.

- 9M25 results review. Revenue RMB431.5B (−2.5% yoy). Operating profit RMB10.87B. Net profit RMB8.10B, with RMB5.31B attributable to equity holders (+0.5% yoy). Working capital expanded with receivables and inventory as NRDL and hospital procurement cycles progressed.

- Market consensus

(Source: Bloomberg)

ICICI Bank Ltd (IBN US): Positioned For Sustained Growth Amid Strong Macro Tailwinds

- RE-ITERATE BUY Entry – 31 Target – 35 Stop Loss – 29

- ICICI Bank Limited operates as a bank. The Bank offers saving accounts, loans, debit, credit cards, insurance, investments, mortgages, and online banking services. ICICI Bank serves customers worldwide.

- Resilient macro backdrop supports long-term banking demand. India remains one of the fastest-growing major economies globally, with Moody’s and RBI projecting 6.5% GDP growth through 2027 supported by robust infrastructure spending, tax-driven consumption stimulus, and easing inflation. The recent GST cuts on household essentials and discretionary goods are expected to lift consumer spending and credit uptake, helping offset the drag from U.S. tariffs on Indian exports. ICICI Bank stands to benefit directly from improving domestic liquidity, rising consumption and expanding credit demand across retail, SME, and trade finance segments.

- RBI liquidity easing and policy support strengthen ICICI’s lending capacity. The Reserve Bank of India’s relaxation of Liquidity Coverage Ratio requirements has released meaningful capital back into the banking system, improving sector-wide liquidity by roughly 600 bps. Combined with an expected 25 bps rate cut in December, the monetary backdrop supports loan growth acceleration into FY26.

- Solid financial performance. ICICI Bank continues to post robust fundamentals, deposits grew 7.7% YoY, domestic loans rose 10.6% YoY, and Q2 net income increased 5.2% YoY to exceed estimates. Net interest income grew 7.4%, while NIM compression remains manageable and is guided to stay range-bound due to RBI’s CRR cut. Asset quality continues to improve, with gross NPA declining to 1.58% and provisions down 26% YoY, supporting earnings resilience even amid volatile treasury income. Capitalisation remains strong with a 16.55% capital adequacy ratio and CET-1 at 15.94%, providing ample buffers for growth.

- Potential easing of tariff headwinds. India’s export sector has been pressured by the U.S. 50% tariff regime, but recent Washington-New Delhi discussions signal potential tariff reductions ahead. The Indian Cabinet’s approval of a US$5.1bn export-support package directly benefits trade-linked borrowers and positions ICICI to capture higher working-capital demand as exporters stabilise. With external uncertainty moderating and domestic policy support expanding, ICICI is positioned to gain from both improving export financing activity and growing domestic consumption.

- 2Q26 results. ICICI Bank delivered a 2.21% YoY increase in revenue to US$3.31bn, beating consensus by US$55.27mn. Earnings per share were US$0.39, beating expectations by US$0.03.

- Market consensus

(Source: Bloomberg)

MakeMyTrip Ltd (MMYT US): Multi-Year Travel Upcycle And AI-Driven Platform Expansion

- RE-ITERATE BUY Entry – 75 Target – 85 Stop Loss – 70

- Makemytrip Ltd. offers travel services over the Internet. The Company operates websites that allow travelers to research and plan trips and book airline tickets, hotels, packages, rail tickets, bus tickets, and rental cars. Makemytrip also offers access to travel insurance.

- Macro acceleration to drive travel spend. India is expected to sustain 6.5%-6.7% GDP growth through 2027, supported by robust infrastructure spending, resilient consumption, GST cuts, falling inflation, and a likely RBI rate cut in December. Lower GST on cars, electronics and consumer staples, combined with rising disposable incomes and a rapidly expanding middle class, is boosting discretionary spending, including tourism. With India remaining the fastest-growing major economy and the second-fastest-growing Asia-Pacific tourism market, MakeMyTrip benefits from a durable step-up in travel demand across both domestic and outbound segments.

- Surge in outbound tourism supports growth. India’s outbound tourism market continues to accelerate, with forecasts reaching US$61.7bn by 2033 and annual growth of 11%-15%. Destinations such as Thailand, UAE, Singapore, and Saudi Arabia are aggressively courting Indian travellers through visa relaxations, new routes and targeted marketing. India is set to become the 5th-largest outbound travel market by 2027, supported by rising incomes, better air connectivity, and growing preference for international leisure. MakeMyTrip’s leadership in air, hotels, and packages uniquely positions it to capture this demand, evidenced by strong international growth in 2Q26 despite muted domestic aviation capacity.

- AI-led engagement strengthens competitive moat. MakeMyTrip’s AI initiatives, such as the Myra conversational agent, AI-powered pre-sales bot and voice agent, are materially enhancing conversion, planning behaviour, and customer stickiness. More than 25,000 daily conversations and repeat interactions up to 90 days before travel signal deep integration into pre-trip workflows. AI-enabled assistance is improving efficiency, cross-selling and trip personalization, which remain key drivers of margin expansion and sustained market share gains for the company.

- 2Q26 results. MakeMyTrip delivered an 8.7% YoY increase in revenue to US$229.34mn, missing estimates by US$32.91mn. GAAP earnings per share were -US$0.06, missing expectations by US$0.25. Gross bookings increased by 8.4% YoY to US$2,447.3mn. During the quarter, the company delivered strong growth in international travel as well as non-flight segments within domestic travel.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Take profit on The Hour Glass Ltd (HG SP) at S$2.2 and Mitsubishi UFJ Financial Group Inc. (MUFG US) at US$15.42. Add Zijin Mining Group Co. Ltd. (2899 HK) at HK$32.