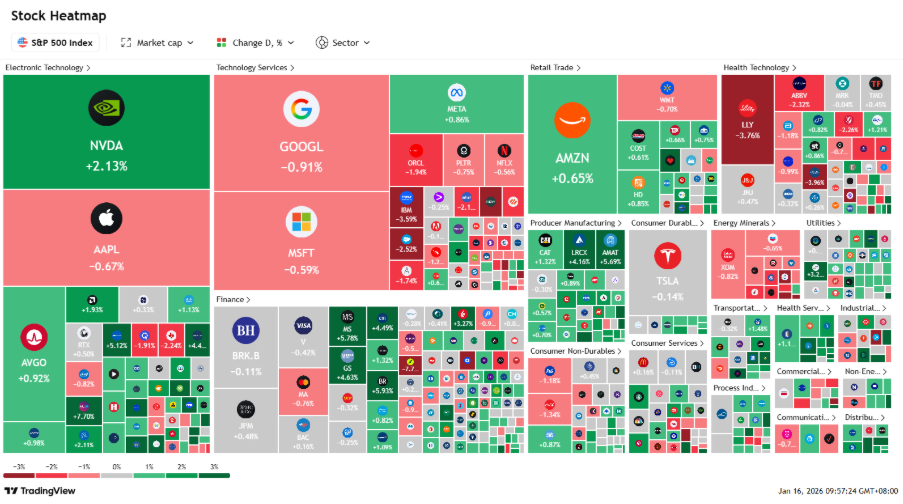

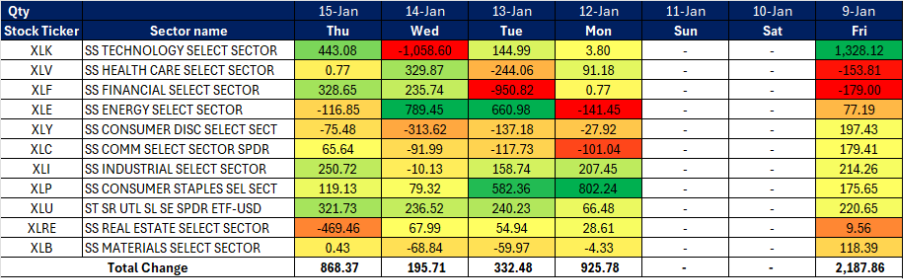

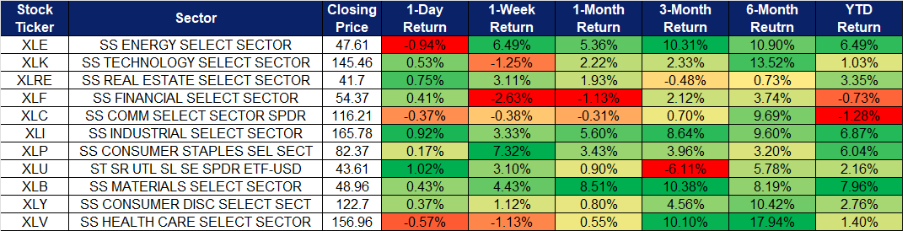

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

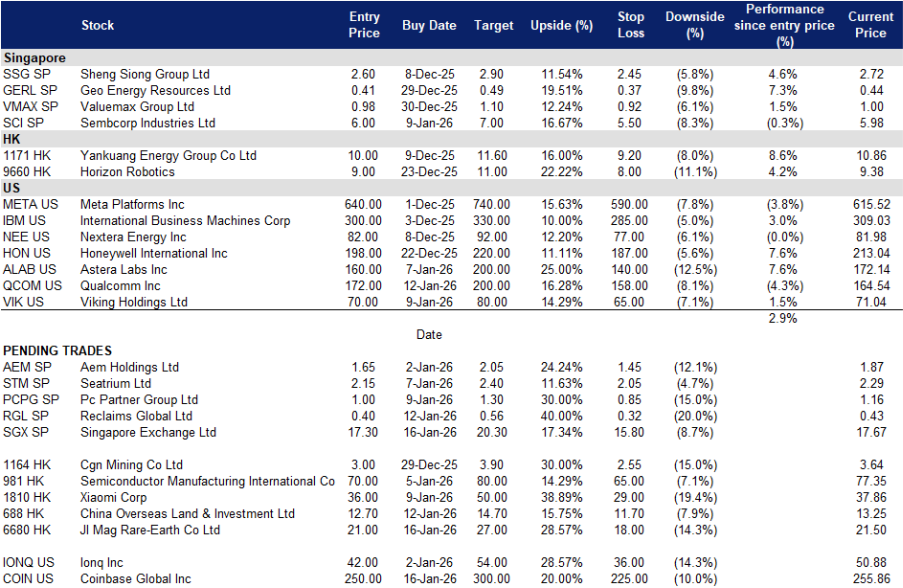

Singapore Exchange Ltd (SGX SP): Crypto-perps As Regulated Beta, Multi-asset Engine, And Dividend Glide Path

- BUY Entry – 17.3 Target – 20.3 Stop Loss – 15.8

- Singapore Exchange Limited owns and operates Singapore’s Securities and derivatives exchange and their related clearing houses. The Company also provides ancillary securities processing and information technology services to participants in the financial sector.

- BTC tape can pull flows into SGX’s new crypto perps. BTC is trading around $96.7k with a ~$97.7k intraday high today. Such levels typically pull forward hedging, basis trades, and flow into perpetuals. SGX launched Bitcoin and Ether perpetual futures on 24 Nov 2025, restricted to accredited, expert, and institutional investors. Second-order logic: when BTC is up and vol is up, regulated derivatives access is in demand; listed perps plus related hedges lift volumes and clearing economics. Ongoing BTC strength and volatility, alongside visible institutional adoption, can support a near-term re-rating for SGX as the regulated venue exposure in Singapore.

- Core engines are already compounding. FY25 net revenue S$1,298m (+11.7% YoY) and adjusted NPAT ~S$610m; derivatives DAV +17.2% and OTC FX ADV +28.5% to ~US$143b underscored breadth across equities, commodities and FX. A stronger base means even modest crypto-perp traction can drop through to group P and L.

- Dividend glide path and balance-sheet discipline. Management outlined a quarterly DPS step-up from FY26 to FY28 (subject to earnings) after delivering FY25 DPS 37.5 cts. Low leverage and growing data/connectivity revenues add quality to earnings while new products extend optionality.

- FY25 results review. Net revenue S$1,298m (+11.7% YoY); adjusted NPAT ~S$610m; total DPS 37.5 cts. Volumes: cash-equities SDAV S$1.34b (+26.5%); derivatives DAV +17.2%; OTC FX ADV ~US$143b (+28.5%).

- Market consensus

(Source: Bloomberg)

Reclaims Global (RGL SP): Recycling Lever To Singapore’s Multi-year Build, Disciplined Ops, Visible Catalysts

- RE-ITERATE BUY Entry – 0.40 Target – 0.56 Stop Loss – 0.32

- Reclaims Global Limited provides waste management services. The Company offer recycling facilities, demolition works, disposal of construction, earth moving, and mass excavation, as well as focuses on machinery such as tipper, truck, dump trucks, and other equipment. Reclaims Global serves customers in Singapore.

- Public-works supercycle and green-concrete adoption. BCA projects 2025 construction demand at S$47–53B nominal, with S$39–46B per year on average from 2026–2029, underpinned by public housing, transport and coast-protection works. Recycled aggregates are explicitly supported in BCA guidance and Green Mark encourage lower-carbon mixes, improving demand for quality recycled materials. This macro and policy mix is constructive for Reclaims’ recycling and excavation volumes into 2026–2029.

- Operating leverage from an integrated model, with improving productivity. Reclaims’ vertical set-up links excavation waste collection to in-house crushing and finished recycled aggregates, then self-deliveries via its fleet. Digitalisation of ERP, HRMS and fleet tracking has already been rolled out, supporting faster quote-to-bill and better asset turns. These features allow margin defense as volumes rise and provide flexibility to price for mix.

- Capital return visibility. Management highlighted NAV 27.5 cts/share as of 31 Jul 2025 and paid an interim dividend of 0.5 cts/share in 1H26. Industry drivers include the expanded Land Intensification Allowance for the built-environment sector from 2026–2030, and Singapore’s multi-decade coastal protection program. Tender momentum and policy follow-through can tighten utilisation across all three segments.

- 1H26 results review. Revenue S$21.8M, +15% YoY. Net profit S$2.48M, −14% YoY, margin ~11%. Interim DPS 0.5 cts, NAV 27.5 cts/share, issued shares 131M.

- Market consensus

(Source: Bloomberg)

JL MAG Rare-Earth Co., Ltd. (6680 HK): Magnet Supply Security Back In Focus; Policy And Price Sheet Set The Stage

- BUY Entry – 21 Target – 27 Stop Loss – 18

- JL MAG Rare-Earth Co., Ltd. manufactures rare earth materials. The Company produces NdFeB magnet materials and other rare earth products. JL MAG Rare-Earth supplies its products to wind power, new energy vehicles, inverter air conditioners, energy saving elevators, and other fields.

- Tight magnet backdrop meets policy re-risking. Rare-earth policy headlines have re-tightened supply risk premia. China’s export license frictions and fresh curbs toward Japan in January 2026 refocus investors on magnet bottlenecks just as EV and wind demand stabilise into 2026. EU and US initiatives to localise critical minerals and curb waste exports underscore Western dependence on Chinese magnet processing capacity. This policy mix is supportive for tier-one Chinese magnet makers with scale and export access.

- Margin rebuild as feedstock prices firm from Q4 lows. Upstream NdPr indicators turned higher into late 2025. Reported prints show Pr-Nd oxide and alloy gained into December, while Neodymium oxide in Northeast Asia was quoted near $101/kg in December 2025. Moderate price firmness supports pass-through and margin retention on new orders, after a weak pricing phase earlier in 2025. JL MAG’s scale and mix enable quicker pricing capture versus small peers.

- Greenland political risk post second order catalyst. Any follow-through headlines on Greenland’s security posture or Western critical-minerals policy, plus renewed market chatter around supply security, can re-rate rare-earth magnet names quickly. Greenland remains strategically discussed but operationally constrained, keeping near-term reliance on Chinese value chains elevated.

- 1H25 results review. Revenue about RMB3.23B, up from RMB2.90B in 1H24. Gross margin 16.39% vs 8.66% in 1H24. Net profit attributable RMB305M, +155% YoY. Interim dividend proposed RMB1.8 per 10 shares.

- Market consensus

(Source: Bloomberg)

China Overseas Land & Investment (688 HK): SOE Ballast As China Steers Inventory Clearance And Sector Consolidation

- RE-ITERATE BUY Entry – 12.7 Target – 14.7 Stop Loss – 11.7

- China Overseas Land & Investment Limited provides real estate services. The Company develops, manages, and invests in commercial properties. China Overseas Land & Investment serves customers globally.

- Policy push to clear inventory supports SOE leaders. Beijing has intensified real estate stabilization with city-led inventory absorption and urban-renewal programs, aiming to reduce unsold stock and steady prices into 2026. Reuters highlighted measures such as government purchases of completed homes for affordable-housing use and tailored city policies. This backdrop typically channels demand and credit to higher quality state-linked developers. COLI’s December update showed RMB39.83B monthly contracted sales and RMB251.23B for 2025, confirming continued scale despite a tough market.

- Consolidation tailwind as Vanke moves toward restructuring. China Vanke has negotiated bank interest deferrals to September 2026 and obtained grace-period extensions on onshore bonds, with ratings actions framing the process as distressed. Vanke is preparing a broader restructuring plan. As financing tightens for private peers, projects and land are more likely to transfer to centrally backed groups. COLI, with strong access to funding and a national sales platform, is well placed to acquire selective assets at attractive terms and to benefit from less aggressive price competition in Tier 1 markets.

- Balance sheet strength enables counter-cyclical investing. COLI reported interim net gearing ~28.4%, cash to short-term debt of ~4.9x, and maintained “green category” metrics, preserving funding advantages. In 1H25 the Group ranked near the top in contracted sales with RMB120.15B, and management continued disciplined land buying focused on major cities. This balance sheet and footprint support steady execution and opportunistic share gains through the cycle.

- 1H25 results review. Revenue RMB83.22B. Core profit RMB8.78B. Contracted sales RMB120.15B for 1H25. Interim dividend HK$0.25 per share.

- Market consensus

(Source: Bloomberg)

Coinbase Global Inc (COIN US): Regulatory Clarity Potential Amid Legislative Uncertainty

- BUY Entry – 250 Target – 300 Stop Loss – 225

- Coinbase Global, Inc. provides financial solutions. The Company offers platform to buy and sell cryptocurrencies. Coinbase Global serves clients worldwide.

- Regulatory clarity plus rising crypto prices drive volume recovery. Bitcoin has rebounded to two-month highs, with broader crypto prices stabilising amid expectations of easier U.S. monetary policy and renewed institutional interest, providing a near-term tailwind to trading volumes and sentiment. Against this backdrop, Coinbase’s Q3 execution was strong, with the platform now covering ~90% of total crypto market cap, record share in U.S. crypto futures and global options, and expanding derivatives following the Deribit acquisition. While Coinbase recently pulled support for the current draft of the Crypto Market Structure Act due to concerns over SEC overreach, the broader direction toward regulatory clarity remains intact, supporting Coinbase’s long-term positioning as an “Everything Exchange” spanning spot, derivatives, and payments.

- Stablecoin scale and payments adoption underpin structural growth. USDC reached a record US$74bn market cap in Q3, with more than US$15bn average USDC balances held on Coinbase products, highlighting growing adoption for payments and treasury use by institutions and corporates. Even as proposed legislation may limit interest-bearing stablecoin rewards, exemptions for loyalty and incentive programs preserve Coinbase’s ability to drive engagement, while accelerating stablecoin payments positions the company to benefit as crypto infrastructure increasingly support real-economy transactions.

- 3Q25 results review. The company delivered revenue of US$1.87bn, a 54.5% YoY growth, beating estimates by US$70mn. Non-GAAP EPS was US$1.44 surpassing estimates by US$0.27. In the fourth quarter, the company expects subscription and services revenue of US$710-790mn, technology & development and general & administrative expenses to be between US$925-975mn and sales and marketing expenses of US$215-315mn.

- Market consensus

(Source: Bloomberg)

Viking Holdings Ltd (VIK US): VIK Fuel Tailwind, K-shaped Demand, And Record Forward Cover

- RE-ITERATE BUY Entry – 70 Target – 80 Stop Loss – 65

- Viking Holdings Ltd operates as a holding company. The Company, through its subsidiaries, specializes in providing offshore recreational travel services by cruise vessel. Viking Holdings serves customers worldwide.

- Bunker price to remain downtrend. U.S. military intervention in Venezuela and the seizure of its oil sector are poised to fundamentally transform the global energy landscape. By taking control of the country’s oilfields—which house the world’s largest proven reserves at 300 billion barrels—U.S. firms are expected to take over production management. Currently, Venezuela’s output remains significantly underutilized at less than 1 million barrels per day (bpd). A U.S.-led effort to rapidly scale this production could trigger a global supply glut, driving oil prices into a sustained decline. For Viking, these lower fuel costs are expected to bolster net yields and voyage margins through the first half of 2026, providing the financial flexibility to maintain competitive pricing even as itinerary schedules shift.

- Benefit from the US K-shaped economy. The affluent cohort continues to spend despite broader softness. Research on the “K-shaped” backdrop highlights resilient outlays by higher-income consumers in categories like luxury travel. That demand profile aligns with Viking’s guest mix and supports load factors and pricing into 2026 even if mass-market discretionary ebbs.

- Forward cover and capacity. As of Nov 2, 2025, Viking had sold 96% of 2025 capacity and ~70% of 2026, with $5.6B advance bookings for 2025 and $4.9B for 2026, both above prior-year pace. High pre-sold cover de-risks near-term cash generation and supports incremental fleet deployment.

- 3Q25 results review. Revenue $1.99B, +19% YoY; Net income $514M; Adjusted net income $534M. Bookings: 2025 and 2026 advance bookings up 21% and 14% vs prior seasons at same points, respectively; 2026 capacity ~70% sold. As of 2Q25, cash $2.6B, undrawn revolver $375M; deferred revenue $4.4B.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Add Viking Holdings Ltd (VIK US) at US$70. Cut loss on Royal Caribbean Cruises Ltd (RCL US) at US$275.