Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

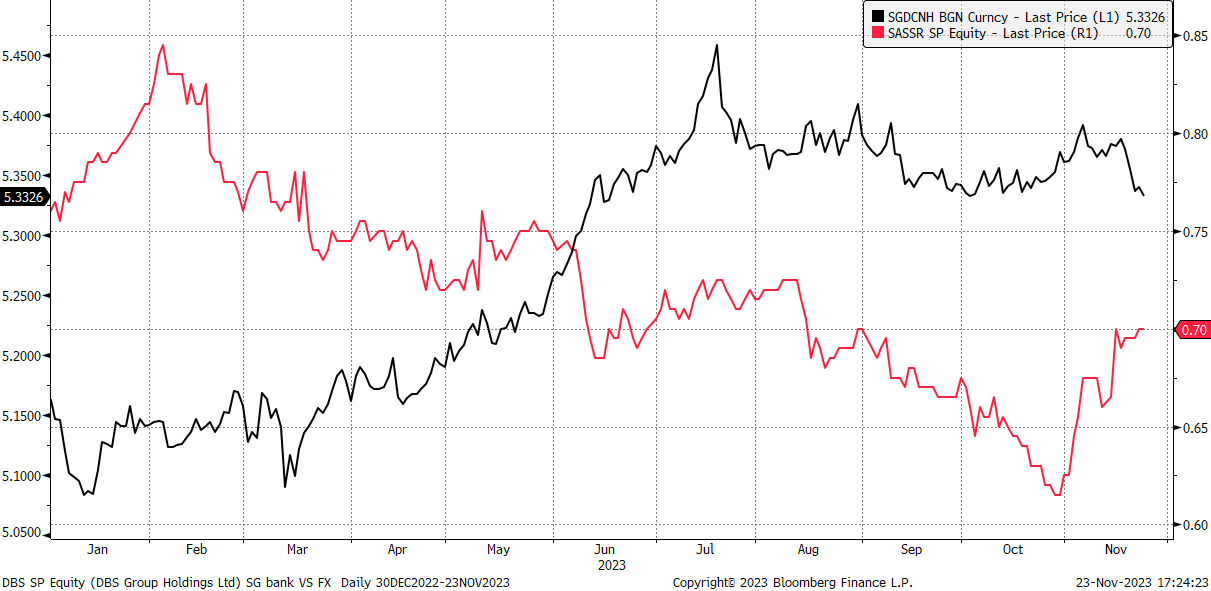

Sasseur REIT (SASSR SP): RMB strengthening

- RE-ITERATE BUY Entry 0.69 – Target – 0.75 Stop Loss – 0.66

- Sasseur Real Estate Investment Trust operates as a real estate investment trust. The Company invests in a diversified portfolio of retail real estate assets. Sasseur Real Estate Investment Trust serves customers in Asia.

- RMB strengthening against SGD. Recently, the Chinese government has taken more aggressive steps to support its economy, such as lowering interest rates, releasing reserve requirements for banks, and increasing spending on infrastructure. These measures have helped to boost economic growth in recent quarters and may help the weakened Chinese yuan to continue to strengthen against the Singapore dollar. FX changes are a key impact on Sasseur’s earnings and dividend as RMB is the operational currency and SGD is the reporting currency.

SGD/RMB price chart

(Source: Bloomberg)

- Retail market recovery in China. The retail market in China experienced a robust recovery in 3Q23, supported by local authorities measures to boost domestic consumption. A notable 18.9% YoY increase in total outlet sales in RMB marked an all-time high since its listing, fuelled by the anniversary sales and consumption-boosting initiatives.

- Resilient 3Q23 performance. Despite a 17.7% YoY decline in total distributable income per unit (DPU) to 1.512 Scts, the business performance showcased steady resilience in 3Q23. Outlet sales in RMB rose by an impressive 15.9% QoQ, with a consistent 15.8% YoY increase, driven by pent-up demand and supportive local measures.

- 3Q23 business updates. Total revenue declined by 1.5% YoY to S$30.3mn. 9M23 revenue decreased by 1.5% YoY to S$92.9mn. Despite growth in RMB for both outlet sales and EMA rental income for 3Q23 and 9M23, the decline in revenue was due to a weak RMB against SGD.

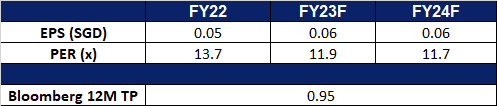

- Market Consensus. We have a fundamental coverage with a BUY recommendation and a TP of S$1.05. Please read the full report here.

(Source: Bloomberg)

Tianjin Pharmaceutical Da Re Tang Group Corp Ltd (TIAN SP): Respiratory illness strikes Northern China

- BUY Entry 2.04 – Target – 2.20 Stop Loss – 1.96

- Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited produces and sells traditional Chinese medicine, western medicine, health products, and healthcare instruments. The Company also manufactures gene-related biopharmaceutical products. Tianjin Pharmaceutical Da Ren Tang Group markets its products under the Great Wall, Cypress, and Health brand names.

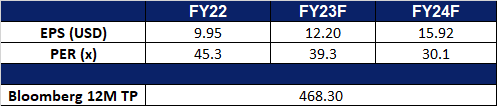

- Respiratory symptoms spreading. China’s National Health Commission (NHC) responded to concerns about respiratory illness outbreaks, citing a surge in acute respiratory infections attributed to a combination of known pathogens, including influenza, rhinovirus, mycoplasma pneumoniae, and respiratory syncytial virus. Despite videos and social media showing crowded hospitals, the NHC assured the World Health Organisation (WHO) that no unusual or novel pathogens were detected, linking the rise to the easing of COVID-19 restrictions and the circulation of known pathogens. Influenza, respiratory syncytial virus, and adenovirus have been circulating since October. While China sees the surge as seasonal and linked to immunity debt, the WHO advises precautionary measures and stays in contact with Chinese authorities. The heightened concern may lead Chinese residents to stock up on medication and health supplements, benefiting companies like Tianjin Pharmaceutical, a producer of such health products.

- Resistance to antibiotics. Despite mycoplasma pneumonia showing resistance to a broad spectrum of antibiotics, it can be treated with other drugs like azithromycin, erythromycin, and clarithromycin. The State Council taskforce has ordered local governments to enhance preparedness for outbreaks of flu, COVID, and other infectious diseases, which may heighten the need for healthcare equipment and medications.

- 3Q23 business updates. Total revenue declined by 5% YoY to RMB$1,705mn. 9M23 revenue increased by 4% YoY to RMB$5,793mn. Issued cash dividend on 6 June 2023 amounting to RMB1.12 per ordinary share.

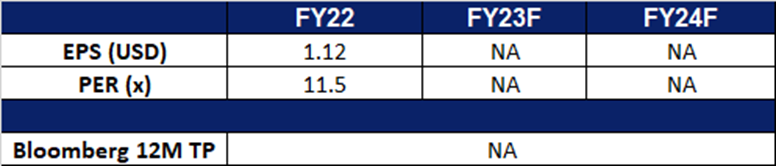

- Market Consensus.

(Source: Bloomberg)

Trip.com Group Ltd. (9961 HK): Favourable seasonality

- BUY Entry – 273 Target – 295 Stop Loss – 262

- Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travellers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

- Upcoming winter travel season. The upcoming winter and festive seasons are expected to provide a boost to travel demand. The winter holidays spanning early November through January are usually one of the busiest travelling periods. Consumers are likely to be clearing their work leaves, or finding time to escape the heat or cold in their countries. The upcoming winter holidays also mark the first winter season since China’s re-opening at the start of 2023. Trip.com would be able to ride on the rising demand for travelling over this peak period. Furthermore, a more relaxed visa-free transit policy is bound to encourage travel agencies from home and abroad to help more foreign visitors come to China. China’s 72-hour and 144-hour visa-free transit policies have been extended to visitors from 54 countries, with Norway being the latest addition.

- An increasing amount of flights showcasing strong travel demand. Several airlines globally have already announced plans to increase the number of flights globally across the incoming winter travel season. Chinese airlines have also seen a rise in scheduled flights for winter-spring, scheduling 96,651 domestic cargo and passenger flights each week for the upcoming winter-spring season, an increase of 33.95% from the same period in 2019-2020, according to the Civil Aviation Administration of China (CAAC). 516 new domestic routes will also be opened from Oct 29 to March 30 next year, providing 7,202 flights each week, according to the CAAC. In terms of international flights, 150 domestic and foreign airlines plan to arrange 16,680 flights per week, reaching 68 foreign countries. The US Department of Transportation announced that flights between China and the US will increase to 70 a week starting on 9 November, from the current 48 a week. The average flights between the two counties averaged 340 a week in the pre-COVID period.

- Promoting inbound tourism to China. Trip.com has signed a three-year agreement with the China International Culture Association (CICA) to boost inbound tourism through the Nihao! China campaign, which focuses on cultural exchange and fostering connections between China and international visitors. This year’s Hello! China event drew 892 representatives from 70 countries and regions around the world. To support China’s inbound tourism goals, the group will provide carefully chosen content highlighting specific products and services and will work with Chinese cultural centers, tourist boards, and other organizations.

- 3Q23 results. Net Revenue improved to RMB 13.7bn, up 99% YoY, compared to RMB 6.9bn in 3Q22. Net profit rose to RMB 4.6bn in 3Q23, compared to RMB 245mn in 3Q22. Diluted EPS was RMB 6.84 in 3Q23, compared to RMB0.41 in 3Q22.

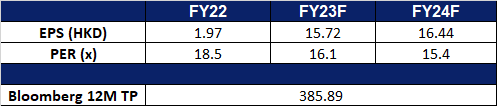

- Market Consensus.

(Source: Bloomberg)

Sunny Optical Technology Group (2382 HK): Promising signs of recovery

- RE-ITERATE BUY Entry – 71.0 Target – 77.0 Stop Loss – 68.0

- Sunny Optical Technology (Group) Company Limited is an investment holding company principally engaged in the design, research and development, manufacture and sale of optical and optical related products and scientific instruments. The Company operates its business through three segments: Optical Components, Optoelectronic Products and Optical Instruments. Through its subsidiaries, the Company is also engaged in the research and development of infrared technologies. The Company distributes its products in the domestic market and to overseas markets.

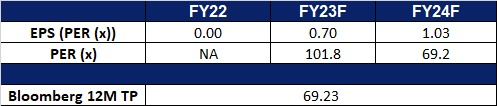

- Recovery in the smartphone market. While China smartphone market shipments dipped slightly in 3Q23 compared to a quarter ago, the market saw a significant rebound in October, supported by regional recoveries and new product upgrade demand. Total shipments of smartphones rose by 11%, primarily fueled by an impressive 83% surge in Huawei sales. Xiaomi also reported a 33% increase in smartphone sales for October. The impressive performance of Huawei and Xiaomi indicates a potential rebound in the China smartphone market, which saw a decline over several quarters previously. Sunny Optical would be able to tap into this recovery of the smartphone market to drive sales to its customers.

- Demand exceeding supply. The launch of the Mate 60 Pro handsets by Huawei Technologies as well as the Xiaomi Mi 14 series saw a huge demand from consumers. Huawei Technologies reportedly sold 1.6mn of its Mate 60 Pro handsets in 6 weeks, while Xiaomi sold over 1.0mn of its Mi 14 series in the first week of its launch. Demand exceeded the supply of these handsets after its launch and suppliers are looking to restock them to cater to the high demand. With companies like Huawei being one of Sunny Optical’s biggest customers for camera modules, Sunny Optical is bound to benefit from the strong demand for high-end Huawei products.

- Breakthrough amidst US chip sanctions. The success of Semiconductor Manufacturing International Corp (SMIC) in delivering an advanced, 7-nanometer processor for Huawei paved the way for further technological advancements in China. This slightly reduced China’s dependence on the US for equipment to produce chips, which had faced many headwinds in China as a result of the constant chip sanctions that the US imposed on China.

- 1H23 earnings. Revenue fell by 15.9% YoY to RMB14.28bn, compared to RMB16.97bn in 1H22. Net profit fell by 66.7% YoY to RMB459.4mn, compared to RMB1.38bn in 1H22. Basic EPS fell by 67.8% YoY to RMB39.99, compared to RMB124.13 in 1H22.

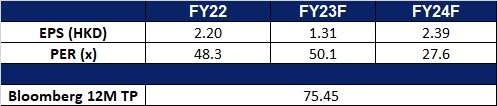

- Market Consensus.

(Source: Bloomberg)

Netflix Inc (NFLX US): Subscribers and profitability boost

- BUY Entry – 475 Target – 500 Stop Loss – 462

- Netflix, Inc. operates as a subscription streaming service and production company. The Company offers a wide variety of TV shows, movies, anime, and documentaries on internet-connected devices. Netflix serves customers worldwide.

- Increase in subscribers. Netflix exceeded expectations in its third-quarter results, reporting a substantial boost in subscriber growth with the addition of 8.76mn global subscribers. This surge was attributed to efforts to crack down on password-sharing and the introduction of a new ad-supported tier. The company’s earnings and revenue surpassed estimates. The total membership rose to 247.15mn, exceeding the expected 243.88mn. Notably, the ad plan membership experienced a nearly 70% QoQ growth. Netflix continues to dominate the streaming industry.

- Raising prices for profitability. In response to increased production costs and the pursuit of improved profitability, Netflix announced a price hike for its basic and premium plans in the US. The basic plan will now cost US$11.99 (up from US$9.99), while the premium plan will be US$22.99 a month (up from US$19.99). Despite this, Netflix is maintaining its ad tier pricing at US$6.99 a month. This strategic move in pricing aligns with the company’s commitment to maintaining its dominance in the streaming world. Additionally, Netflix provided a forecast for an 11% jump in revenue in the fourth quarter, reaching US$8.69bn, with expectations of net subscriber adds similar to the third quarter. Furthermore, the company also addressed shareholder concerns about executive compensation, promising substantial changes to a more conventional model in 2024 while retaining a performance-based structure.

- 3Q23 results. Revenue rose to US$8.54bn, up 7.7% YoY, in line with expectations. GAAP EPS beat estimates by US$0.23 at US$3.73. Expect Q4 revenue of US$8.69bn vs US$8.54bn consensus. Revised its full-year operating margin upwards to 20%. FY24 operating margin to be between 22% and 23%.

- Market consensus.

(Source: Bloomberg)

Shopify Inc (SHOP US): Shopping frenzy

- RE-ITEREATE BUY Entry – 70 Target – 76 Stop Loss – 67

- Shopify Inc. provides a cloud-based commerce platform. The Company offers a platform for merchants to create an omni-channel experience that helps showcase the merchant’s brand. Shopify serves customers in Canada.

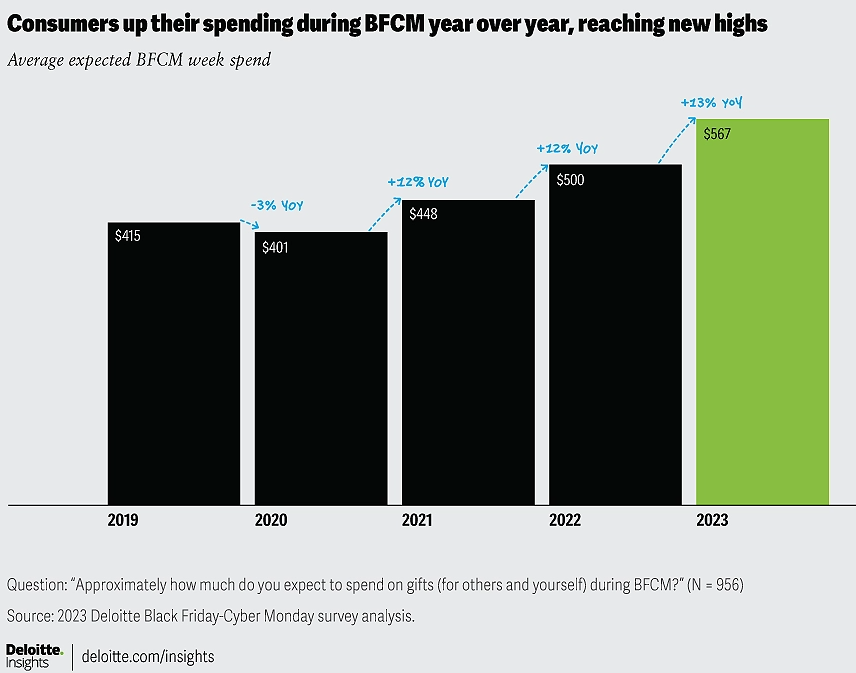

- Black Friday and Cyber Monday weekend frenzy. Shopify experienced a robust 13% YoY surge in Gross Merchandise Volume (GMV), reaching US$61.0bn in 4Q22, propelled by a successful Black Friday and Cyber Monday weekend. The company foresees sales surpassing 4Q22 in the current quarter. The Thanksgiving week, comprising Black Friday and Cyber Monday, kicks off the holiday shopping season, accounting for about 16.7% of retail sales during this period. The National Retail Federation (NRF) estimates that 19% of annual retail sales occur between Black Friday and Christmas. This year, 74% of Americans are expected to shop during this week, marking the highest since 2017. The NRF projects holiday spending to grow by 3-4%, reaching US$957.3bn to US$966.6bn. Deloitte predicts consumers will spend an average of US$567 during Black Friday to Cyber Monday, a 13% increase YoY, with Millennials driving 43% of sales. The surge in holiday spending is anticipated to bring sales back to pre-pandemic levels, creating a promising season for retailers and consumers. Despite economic concerns, the 2023 Deloitte holiday survey reveals that US consumers are determined to make this holiday season memorable by planning to spend an average of US$1,652, surpassing pre-pandemic figures for the first time. Emphasising value during key promotional events may be a winning strategy for retailers, given that 66% plan to shop during the week of Black Friday-Cyber Monday. The shortened shopping timeframe, reduced from 7.4 weeks to 5.8 weeks, underscores the importance of having the right products at the right prices during promotional periods.

Spending expected to incline over Black Friday, Cyber Monday (BFCM) weekend

(Source: Deloitte Consumer Industry Center)

Prediction of holiday consumption

(Source: National Retail Federation)

- Positive results and costs refinement. Shopify displayed a strong third-quarter performance that exceeded expectations. Shopify foresees a mid-twenties percentage growth in 2023 revenue YoY, driven by a robust fourth-quarter performance. GMV for the quarter rose by 22% to US$56.2bn. The company’s net income reached US$718mn, compared to a loss of US$158.4mn in the same period last year. Operating expenses declined 23% YoY to US$779mn, primarily due to its reduced headcount and the sale of its logistics business. Shopify’s solid results coincide with strategic moves, including workforce reductions and partnerships with Amazon and Faire.

- Partnership with Amazon. Shopify announced an open partnership with Amazon, allowing its merchants access to the Buy with Prime app for a complete e-commerce experience on their storefronts outside Amazon. This collaboration is available to all merchants using or interested in Amazon’s fulfillment network. Buy with Prime enables Prime members to shop on non-Amazon e-commerce sites using their Amazon account for checkout, with Amazon handling fulfillment. The partnership, announced in August 2023, resulted in the Shopify app offering easier integration and additional features like catalog syncing. The move targets the growing overlap of sellers on both Amazon and Shopify, providing a streamlined experience for brands with a presence on both platforms.

- 3Q23 results. Revenue rose to US$1.71bn, up 24.8% YoY, beating expectations by US$40mn. Non-GAAP EPS beat estimates by US$0.10 at US$0.24. Expect full-year revenue to grow by a mid-20s percentage rate YoY, driven by Q4 revenue growth in the high-teens on a GAAP basis.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Sasseur REIT (SASSR SP) at S$0.69. Cut loss on OCBC Bank (OCBC SP) at S$12.58.