26 September 2022: DBS Group Holdings Ltd (DBS SP), TRIP.COM (9961 HK)

Singapore Trading Ideas | Hong Kong Trading Ideas | Market Movers | Trading Dashboard

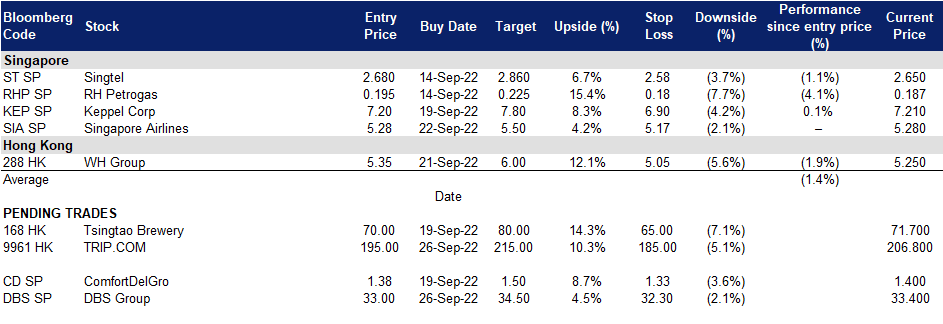

DBS Group Holdings Ltd (DBS SP): Tailwinds from rate hikes

- BUY Entry 33.0 – Target – 34.5 Stop Loss – 32.3

- DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The company offers mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage services. DBS Group also is the primary dealer of Singapore government securities. DBS Bank Ltd operates as a bank offering wealth management, personal, and business banking services. DBS Bank serves customers worldwide.

- Housing loan rate adjustments. After the recent rate hike from the United States Federal Reserve, DBS announced that it would temporarily cease its fixed-rate home loans as the loan rates on these packages are being reviewed. The bank however continues to offer floating rate packages which are pegged to the SORA. By putting a pause on fixed-rate home loan packages in this volatile interest rate market, they are mitigating their risks and passing them on to their borrowers.

- Benefiting from higher Interest rates. With the constant rise in interest rates, DBS will be able to increase its margins when lending money to borrowers. Additionally, by taking advantage of the difference between the interest paid out to lenders and the interest earned from short-term investments, their profits will grow.

- Expansion of services. With the rapid boom of the cryptocurrency sector and the surge in the volume of crypto transactions carried out on its members-only platform, DBS recently expanded access to its crypto trading services. It announced the roll-out of self-directed crypto trading on DBS digibank, enabling 100,000 of the bank’s wealth clients who are accredited investors to trade cryptocurrencies on the DBS Digital Exchange (DDEx) at their convenience. These clients will be able to trade four cryptocurrencies – Bitcoin, Bitcoin Cash, Ether and Ripple – on DDEx with a minimum investment of S$500.

- The updated market consensus of the EPS growth in FY22/23 is 15.2%/18.7% YoY, respectively, translating to 11.1×/9.4x forward PE. The current PER is 12.8x. Bloomberg consensus average 12-month target price is S$39.31.

(Source: Bloomberg)

Singapore Airlines Ltd (SIA SP): Robust tourism demand

- RE-ITERATE BUY Entry 5.28 – Target – 5.50 Stop Loss – 5.17

- The Singapore Airlines Group has over 20 subsidiaries, covering a range of airline-related services, from cargo to engine overhaul. Its subsidiaries also include SIA Engineering Company, Scoot, Tiger Airways, Singapore Flying College and Tradewinds Tours and Travel. Principal activities of the Group consist of air transportation, engineering services and other airline related activities.

- Post-Covid boom. In 2022, according to statistics collated by Singapore Tourism Board, there has been an exponential increase in visitor arrivals since the reopening of our borders to vaccinated travellers without quarantine in April. Between January and August this year, there were a total of about 2.96 million visitors, a Y-o-Y increase of 1,833% as compared to the same period in 2021. In August alone, Singapore welcomed approximately 729 thousand visitors. However, visitor growth can be seen slowing as there was only a slight increase of 2000 visitors, from July to August.

- Tailwinds. Since the gradual reopening of borders globally, travel has resumed. Singapore Airlines Limited has benefited from this with growth in passenger traffic. It more than doubled its monthly available seat kilometres and boosted the number of passengers it flew by more than ten-fold. With both business and leisure travellers increasing, the airline will have to manage resources and manning shortages well.

- Travel growth. Aviation will continue to recover as we see more borders opening up and people take advantage of their freedom to travel. Additionally, with the upcoming events to be held in Singapore and the year-end holiday season coming up, we expect travel demand to remain robust for the rest of the year.

- 1Q23 results review. In1Q23 (YE March), net profit arrived at S$370 million, recovering from a S$409 million loss during the same period in 2021. This was a result of the sharp revival in travel demand after economies reopened their borders. Additionally, their operating statistics showed significant month-on-month passenger traffic growth since April, with August seeing a tapered increase.

- Updated market consensus of the EPS in FY23/24 is S$0.333/S$0.365 respectively, which translates to 16.1x/14.6x forward PE. Bloomberg consensus average 12-month target price is S$5.86.

(Source: Bloomberg)

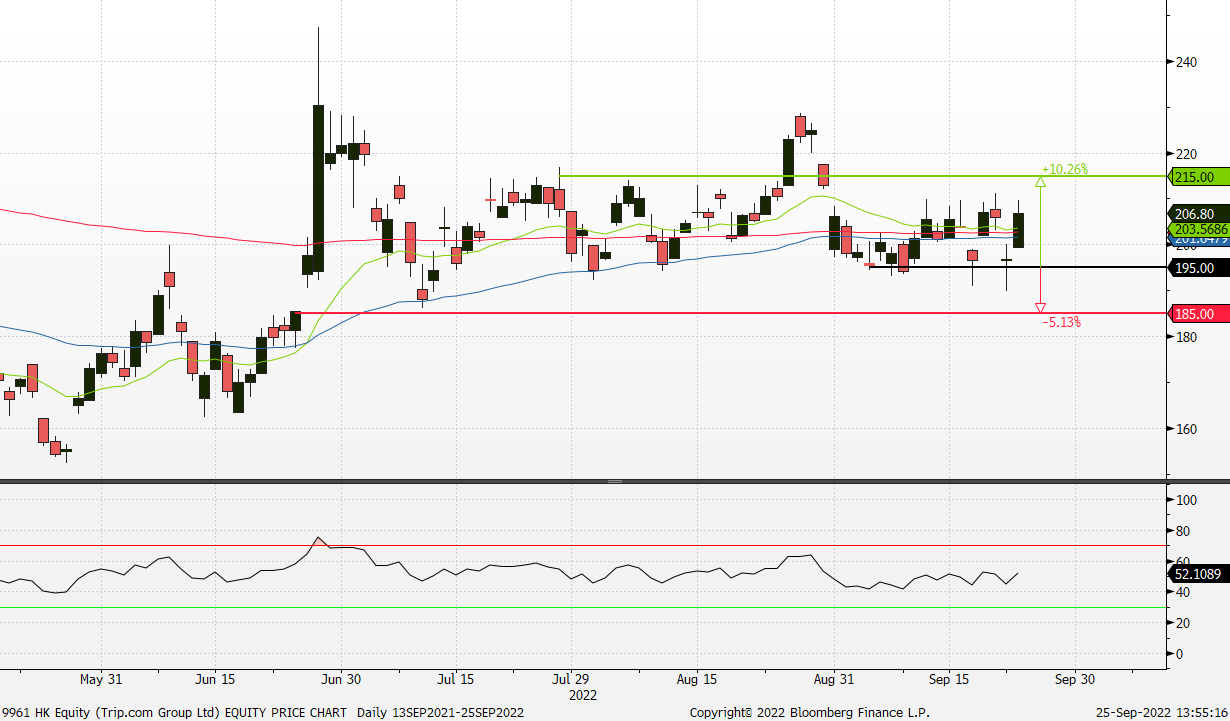

TRIP.COM (9961 HK): Japan, Taiwan, and Hong Kong reopen

- Buy Entry – 195 Target – 215 Stop Loss – 185

- Trip.com Group Limited, formerly Ctrip.com International, Ltd., is a travel service provider in China that provides accommodation booking, transportation ticketing, package tours and corporate travel management. The company aggregates hotel and transportation information to help leisure and business travellers make reservations. The company helps leisure travellers book travel packages and guided tours and helps corporate clients manage their travel needs. The company also offers a range of travel-related services to meet the different booking and travel needs of leisure and business travellers, including visitor reviews, attraction tickets, travel-related financial services, car services, travel insurance services and passport services. The company also offers package tours for independent leisure travellers, including tour groups, semi-tour groups and private groups, as well as package tours that require different transportation arrangements (such as cruise, buses or self-driving).

- Tailwinds of Asia tourism. Japan will fully reopen to foreign tourists from 11th October onwards. Tourists will no longer need a visa to enter the country. Taiwan will reopen its borders from 13 October onwards. Arrivals will be asked to self-monitor for seven days. From 26 October, travellers arriving in Hong Kong will no longer have to go into mandatory hotel quarantine.

- 2Q22 results review. Net revenue dropped by 32% YoY and 2% QoQ to RMB4.0bn due to the continued disruptions resulting from the COVID-19 resurgence in China. Gross profit dropped by 35.0% YoY and 0.2% QoQ to RMB3.0bn. Net profit attributable to company shareholders was RMB69mn compared to a net loss of RMB647mn during the same period in 2021 due mainly to effective cost control.

- Updated market consensus of the EPS in FY22/23 is RMB1.55/RMB7.14 respectively, which translates to 121.0x/26.3x forward PE. Bloomberg consensus average 12-month target price is HK$262.31.

(Source: Bloomberg)

Tsingtao Brewery Company Limited (168 HK): A FIFA World Cup themed play

- RE-ITERATE Buy Entry – 70 Target – 80 Stop Loss – 65

- Tsingtao Brewery Company Limited, together with its subsidiaries, engages in the production, distribution, wholesale, and retail sale of beer products worldwide. The company sells its beer products primarily under the Tsingtaoand and Laoshan brand names. It also provides wealth management, and agency collection and payment services; and financing, construction, and logistics services, as well as technology promotion and application services.

- FIFA World Cup Qatar 2022 in two months. The once in every four years FIFA World Cup is going to take place from November to December 2022. This is the global largest sports event after the Tokyo Olympic Games, and it is expected to attract a record high of spectators as most countries have eased COVID restrictions. Accordingly, it will stimulate sales of alcohol and other drinks. The beer feast will take place during the world cup period.

- 1H22 earnings review. Revenue grew by 5.4% YoY to RMB19.3bn. Gross profit dropped by 9.6% YoY to RMB7.3bn. GPM dropped by 6.3ppts to 38.1%. Net profit attributable to shareholders of the company grew by 18.1% YoY to RMB2.9bn. NPM increased by 1.3ppts to 14.8%. The growth of the bottom line was due mainly to the upgrade of the product mix and improvement of cost control.

- The updated market consensus of the EPS growth in FY22/23 is 1.5%/17.1% YoY, respectively, translating to 27.4×/23.4x forward PE. The current PER is 24.4x. Bloomberg consensus average 12-month target price is HK$89.35.

(Source: Bloomberg)

United States

Top Sector Gainers

| Sector | Gain | Related News |

| Home Improvement Chains | +0.42% | 3 Companies Boosting Their Dividends Faster Than Inflation Home Depot Inc (HD US) |

Top Sector Losers

| Sector | Loss | Related News |

| Oil & Gas Production | -7.74% | Oil plunges to eight-month low on strong dollar, recession fears ConocoPhillips (COP US) |

| Integrated Oil | -7.07% | Why Oil and Gas Stocks Sank Today Chevron Corp (CVX US) |

| Other Metals/Minerals | -5.55% | Copper price falls to lowest in 2 months on rising interest rates Rio Tinto PLC (RIO US) |

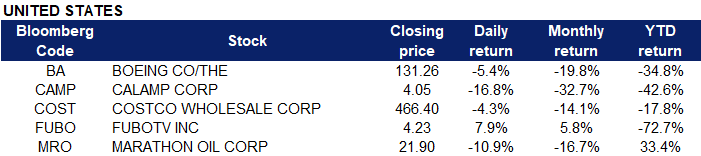

- Boeing Co/The (BA US) was down 5.4% after it reached a $200 million settlement on charges of misleading investors following two of its jetliners being involved in deadly crashes.

- CalAmp Corp (CAMP US) plummeted 16.8% despite an earlier rally. CalAmp reported smaller losses than anticipated in its second-quarter earnings, while also noting record-setting revenue within subscription and software categories.

- Costco Wholesale Corp (COST US), which said it would not raise membership prices this week, saw shares drop 4.3%. Costco released earnings that beat expectations and showed year-over-year gains, but also said it was experiencing higher labour and freight costs.

- fuboTV Inc (FUBO US) jumped 7.9% after Wedbush upgraded the streaming service to outperform from neutral, saying fuboTV is at “compelling entry point” for investors.

- Marathon Oil Corp (MRO US) fell 10.9%, defying a positive report from Evercore ISI that viewed the company as having strong free cash flow.

Singapore

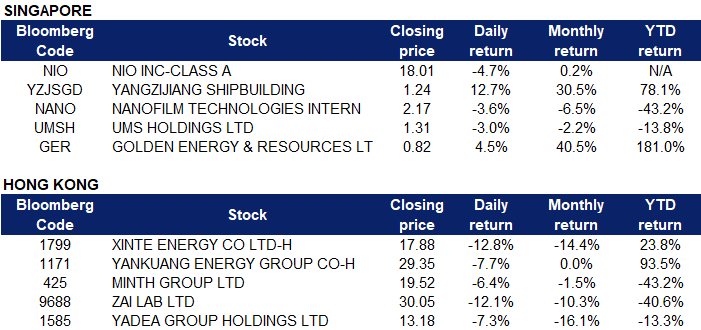

- NIO Inc (NIO SP) fell 4.7% on Friday. Nio recently announced that it shipped the first battery-swap station from its new facility in Hungary as it continues to expand in Europe. But it continued to decline amid increased worries about Russo-Chinese ties, escalating Taiwan tensions, lingering lockdown effects and concerns over more rate hikes from the Fed.

- Yangzijiang Shipbuilding Holdings Ltd (YZJSGD SP) gained 12.7% on Friday, triggering a query from Singapore Exchange Regulation. Shares of the group have been rising steadily since Sept 8, when it announced that it had obtained a technology membrane licence from French naval engineering company GTT. The receipt of the licence was deemed as a “major breakthrough” by DBS Group Research, paving the way for Yangzijiang’s entry into the liquefied natural gas carrier market. It is also the first non-state-owned enterprise Chinese shipyard to obtain a licence from GTT.

- Nanofilm Technologies International Ltd (NANO SP) and UMS Holdings Ltd (UMSH SP) declined 3.6% and 3.0% on Friday. The Straits Times Index (STI) tumbled 1.1 per cent or 35.97 points to close at 3,227.10 on Friday (Sep 23), as Singapore’s higher-than-expected headline inflation figures for August caught market watchers by surprise. In the broader Singapore market, losers outnumbered gainers 340 to 179 on Friday, with 1.33 billion securities worth S$1.41 billion traded.

- Golden Energy & Resources Ltd (GER SP) rose 4.5% on Friday. Iron ore futures rebounded from two-week lows on Thursday (Sep 22), bolstered by rising steel output in top producer China and expectations of higher demand for the steelmaking ingredient ahead of the country’s Golden Week holiday. China’s daily crude steel output recovered in mid-September mainly due to some blast furnace steelmakers resuming operations or steadily ramping up output after the previous production cutbacks. Steel prices rebounded, other steelmaking inputs also rising, with Dalian coking coal up 2.8 per cent and coke climbing 1.8 per cent.

Hong Kong

Top Sector Gainers

| Sector | Gain | Related News |

| Travel & Tourism | +4.74% | Hong Kong to scrap COVID-19 hotel quarantine for overseas arrivals from Sep 26 Trip.com Group Ltd (9961 HK) |

| Consumer Electronics | +2.21% | U.S. chip alliance against China tests South Korea’s loyalty Smoore International Holdings Ltd (6969 HK) |

| Telecomm. Services | +1.12% | China’s telecom sector posts stable growth in Jan-Aug China Mobile Ltd (941 HK) |

Top Sector Losers

| Sector | Loss | Related News |

| Coal | -2.39% | Xi Jinping over-promised about coal consumption in China, says report Yankuang Energy Group Company Limited (1171 HK) |

| Environmental Energy Material | -2.29% | Anti-dumping duty on China glass imports expires Flat Glass Group Co Ltd (6865 HK) |

| Biotechnology | -2.04% | After a US$1.3 trillion rout, analysts predict more pain in store for Hong Kong’s stock market amid rate increases Genscript Biotech Corp (1548 HK) |

- Xinte Energy Co Ltd (1799 HK) fell 12.8% on Friday. According to a research report released by Cinda Securities, solarzoom statistics found that domestic silicon material production in August 2022 was 61,700 tons, an increase of 5.47% month-on-month. Production is expected to increase by about 20% month-on-month. With the new effective annual production capacity of global silicon materials to be around 120,000 tons in Q4, the price of the industry goods may begin to drop.

- Yankuang Energy Group Co Ltd (1171 HK) tumbled 7.7% on Friday. The European Union issued new guidance last week, saying that the transfer of Russian coal and fertilisers to countries outside the EU is now allowed, citing energy security concerns. This followed an intervention in August that surprised insurers and shipowners as the European Union said it banned Russian coal shipments altogether.

- Minth Group Ltd (425 HK) declined 6.4% on Friday. Recently, CITIC released an updated report lowering Minth Group’s EPS forecast for 2022/23 to 1.45/1.79 yuan, taking into account high sea freight and raw material costs along with their low gross profit margin for their new product. Furthermore, they also factored in the company’s high overseas exposure, and current degree of performance uncertainty.

- Zai Lab Ltd (9688 HK) and Yadea Group Holdings Ltd (1585 HK) fell 12.1% and 7.3% respectively. Hong Kong shares finished a tough week with another loss on Friday (Sep 23) as global markets were battered by recession concerns, with central banks ramping up interest rates to fight inflation. The Hang Seng Index dropped 1.18 per cent, or 214.68 points, to 17,933.27, a day after the HKMA warned of more rate increases. The benchmark slipped into bear territory as losses in tech companies and developers deepened. After facing a succession of challenges, from China’s economic slowdown, tech crackdown, Covid-19 border closures and local currency depreciation, an increase in prime rates will exacerbate pessimism on market outlook.

Trading Dashboard Update: Cut loss on China Resources Power (836 HK) at HK$13.8 and Ganfeng Lithium (1772 HK) at HK$60.0.