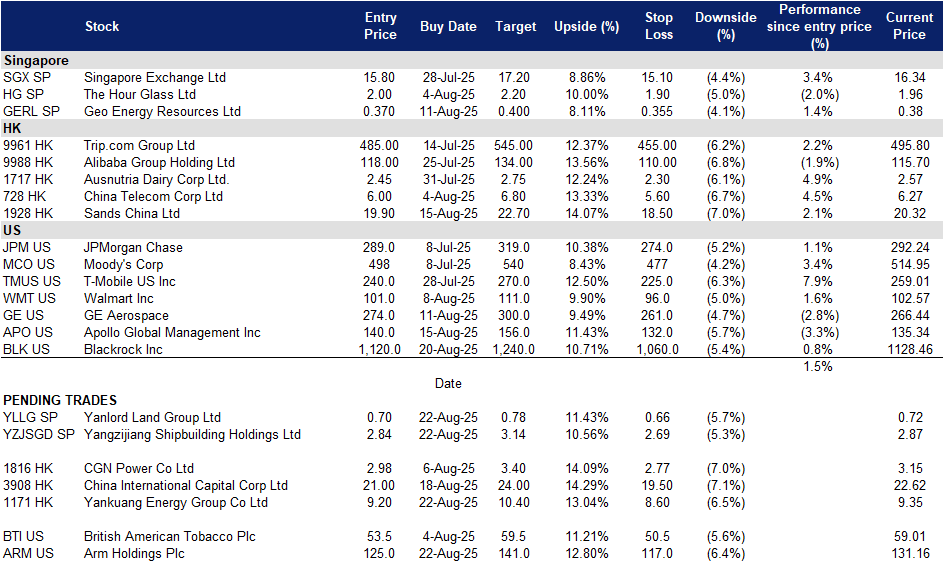

Yangzijiang Shipbuilding Holdings Limited builds a wide range of ships. The Company produces a wide range of commercial vessels, mini bulk carriers, multi-purpose cargo vessels, containerships, chemical tankers, offshore supply vessels, rescue and salvage vessels, and lifting vessels.

Record profit growth despite revenue headwinds. Yangzijiang Shipbuilding delivered a record-high net profit of RMB4.2bn (S$752.6mn) in 1H25, representing a 36.7% YoY surge, even as revenue dipped 1.3% to RMB12.9bn. The earnings strength was driven by a sharp improvement in profitability, with net margins expanding to 32.5% from 23.4% a year earlier, supported by higher contributions from associated companies and joint ventures. Contributions from Yangzi-Mitsui Shipbuilding (RMB320mn) and Tsuneishi Zhoushan (RMB160mn) were particularly meaningful, following Yangzijiang’s 34% equity stake acquisition earlier this year. This diversification into partnerships and associate stakes is proving to be an effective earnings stabiliser, helping to offset revenue softness from lower-value oil tanker contracts and weaker shipping charter rates.

Robust order book provides earnings visibility amid industry slowdown. Despite order wins slowing sharply to just US$537mn in 1H25 compared to US$3.3bn in the year ago period, Yangzijiang’s outstanding order book remains substantial at US$23.2bn, stretching through 2029 and beyond. Roughly 85% of the new contracts in the period were for container vessels, underscoring continued demand for Yangzijiang’s core products despite global shipbuilding orders contracting 54% YoY in the first half. This sizeable backlog provides clear earnings visibility for the next few years and positions the company to accelerate its orderbook growth once tariff uncertainties and global trade volumes stabilise in the second half. The management has also indicated confidence in filling its remaining 2028-2029 delivery slots, largely for small to mid-sized vessels, further supporting medium-term growth.

Cementing China’s global shipbuilding dominance. The broader Chinese shipbuilding industry continues to reinforce its dominance, accounting for 51.7% of global completions and 68.3% of new orders in 1H25. The ongoing CSSC-CSIC share-swap merger, set to create the world’s largest listed shipbuilder by assets and revenue, will streamline operations, cut costs by up to 10%, and enhance competitiveness in high-end vessel types such as LNG carriers and mega container ships. For Yangzijiang, operating alongside a larger state-owned champion presents both challenges and opportunities, while competition may intensify, the stronger ecosystem could enhance supply chain efficiencies and global credibility for Chinese shipbuilders. Ultimately, the consolidation underscores China’s shipbuilding dominance, providing a supportive backdrop for Yangzijiang’s growth trajectory.

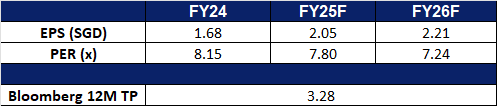

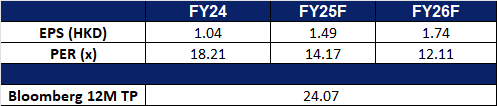

1H25 results review. Yangzijiang Shipbuilding reported 1H25 revenue of RMB12.88bn, a 1.3% YoY decline. It reported a net profit of RM4.18bn, a 36.7% jump YoY, from RMB3.06bn in the year-ago period. In the first half, the group secured contracts amounting to US$537.2mn (S$690mn) for 14 vessels, with about 85% for container ships, raising the group’s total outstanding order book to US$23.2bn for delivery in 2029 and beyond.

Market consensus

(Source: Bloomberg)

Yanlord Land Group Ltd (YLLG SP): Further intervention to revive property market

BUY Entry – 0.70 Target – 0.78 Stop Loss – 0.66

Yanlord Land Group Ltd is a real estate development company. The Company develops high-end residential property projects in the Peoples Republic of China.

Profitability turnaround driven by higher-margin deliveries. Yanlord Land achieved a net profit of RMB379.2mn in 1H25, reversing from a RMB486mn loss in the prior year period. The improvement was underpinned by a strategic shift toward delivering higher-margin development projects and a reduction in write-downs on completed and in-progress properties. While revenue fell 53.5% YoY to RMB9.3bn due to lower gross floor area delivered, earnings per share rebounded to S$0.1963 from a loss of S$0.2516. This profit recovery, despite weaker top-line performance, signals improved cost discipline and portfolio optimisation.

Policy support and market stabilisation. China’s property sector remains in a prolonged downturn, but recent government actions could accelerate stabilisation. Regulators are preparing to mobilise central state-owned enterprises and bad-debt managers, including China Cinda Asset Management, to purchase unsold housing inventory, tapping into RMB300bn of PBOC funding. Removing price caps and involving well-capitalised state entities could improve the programme’s economics and speed up clearance of the estimated 60 million unsold apartments nationwide. For Yanlord, whose projects are concentrated in premium urban locations, such coordinated intervention, combined with early signs of moderating sales declines, could help sustain profitability into 2026-2027, even as the recovery is expected to be gradual and execution risks remain.

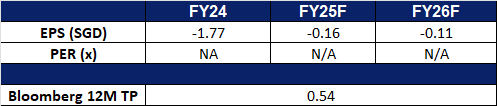

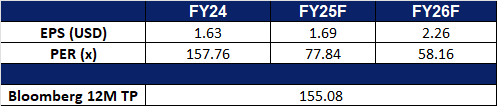

1H25 results review. Yanlord reported 1H25 revenue of RMB9.2bn, a 53.5% YoY decline from 1H24 revenue of RMB20bn. It reported earnings per share S$0.1963 in 1H25, reversing from a loss of S$0.2516 in 1H24.

Market consensus

(Source: Bloomberg)

Yankuang Energy Group Co Ltd. (1171 HK): Rebounding coal prices

BUY Entry – 9.20 Target – 10.40 Stop Loss – 8.60

Yankuang Energy Group Co Ltd is a China-based company principally engaged in the coal business. The Company mainly conducts businesses through five segments. The Products of the Coal Business segment mainly includes thermal coal, pulverized coal injection coal and coking coal, which are suitable for power, metallurgy and chemical industries. The Products of the Coal Chemical and Power segment mainly includes methanol, acetic acid, ethyl acetate, caprolactam, urea, ethylene glycol, naphtha, crude liquid wax and others. The Mining Equipment Manufacturing segment is mainly engaged in the manufacturing of mining equipment. The Non-coal Trade and Logistics segment is mainly engaged in smart logistics business. The Loan and Financial Leasing segment is mainly engaged in deposit and loan businesses.

Sustained power demand through summer heatwaves. Record-high temperatures across China this summer have driven a surge in electricity consumption, as households and businesses rely more heavily on air conditioners and fans. In regions such as northeastern coastal cities and Shandong province, where temperatures have exceeded 35°C, cooling has become an essential need rather than a discretionary choice. The resulting spike in electricity demand is expected to support continued coal consumption, providing a near-term tailwind for Yankuang Energy, even as China gradually transitions toward cleaner energy sources.

Stricter coal supply regulation to support prices. Chinese authorities have recently intensified efforts to curb excessive coal production, launching inspections across eight provinces—including Shanxi, Inner Mongolia, Shaanxi, and Xinjiang—to crack down on overmining. Regulators have also warned that mines exceeding permitted capacity could face shutdowns. These measures, aimed at curbing overcapacity and stabilizing the market, are likely to tighten supply and create upward pressure on coal prices, benefiting Yankuang in the near term.

Coal price rebound underway. Since June 2025, coal prices have steadily recovered, supported by strong summer power demand and growing expectations of policy support for coal producers. The recent regulatory clampdown on overproduction has further strengthened market sentiment, contributing to incremental price gains. As a result, Yankuang stands to benefit from selling coal at higher price levels over the coming quarters.

Thermal Coal Prices

(Source: Bloomberg)

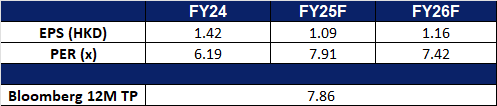

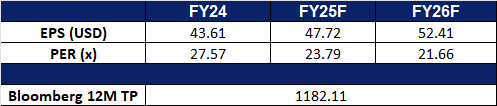

1Q25 results review. 1Q25 operating income fell by 23.5% to RMB30.3bn, compared to RMB39.6bn in 1Q24. Profit attributable to shareholders fell by 27.9% to RMB2.71bn in 1Q25, compared to RMB3.76bn in 1Q24. Basic earnings per share was RMB0.27 per share compared to RMB0.39 in 1Q24.

Market consensus.

(Source: Bloomberg)

China International Capital Corp Ltd. (3908 HK): Beneficiary of shifting global capital flows

China International Capital Corp Ltd is a China-based company mainly provides investment banking services to domestic and overseas enterprises, institutions and individuals. The Company mainly operates its businesses through six segments. The Investment Banking segment mainly provides equity financing, debt and structured financing and financial consulting services for enterprises and institutions. The Stock segment mainly provides comprehensive financial services for stock business to professional investors. The Fixed Income segment mainly provides interest rate and foreign exchange, credit business, securitization business, derivatives and futures business. The Investment Management segment is mainly engaged in asset management business, fund management business and private equity investment fund business. The Wealth Management segment mainly provides wealth management products and services. The Research segment mainly provides research services to customers.

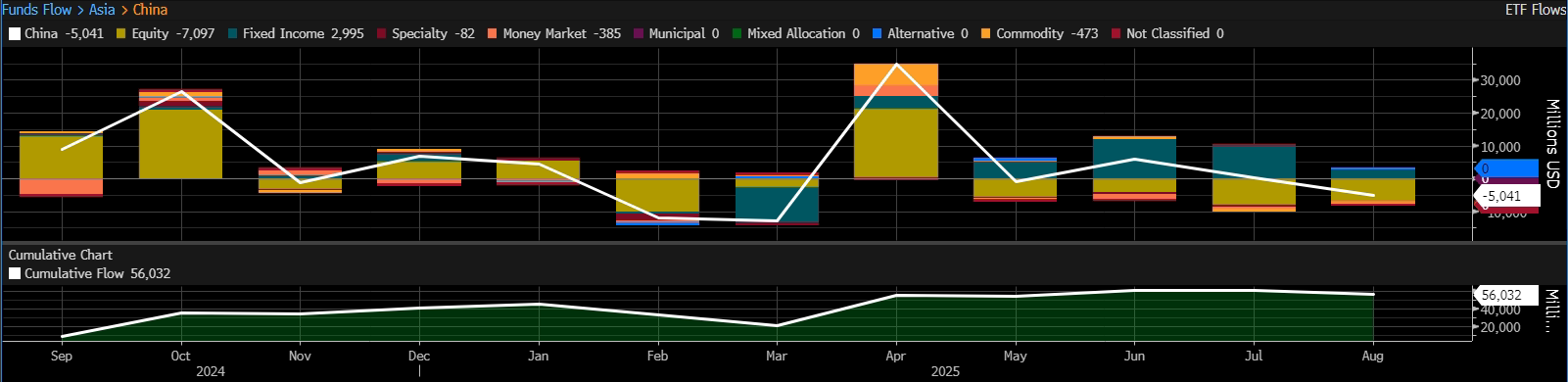

Capital inflow to emerging markets. The continued depreciation of the U.S. dollar, driven by U.S. policy instability and heightened trade tensions, has prompted global investors to reduce U.S. exposure and seek opportunities in emerging markets. April marked a turning point, with China recording a sharp spike in net inflows, particularly into equities, signalling renewed investor confidence. While May saw a slight pullback, net inflows resumed in June and July, keeping cumulative foreign investment levels elevated since April. This influx of capital supports market liquidity, trading volumes, and asset valuations, key revenue drivers for CICC. As one of China’s leading investment banks with strong asset management and brokerage capabilities, CICC stands to benefit from both higher transaction-based income and an expanded asset base, which will boost recurring management fees.

Fund flow – China

(Source: Bloomberg)

Potential rate cut in September. According to CME FedWatch, there is a 92.6% probability of a 25 basis point Federal Reserve rate cut in September, marking the first easing move this year, with markets pricing in the possibility of additional cuts before year-end. Lower U.S. rates would weaken the dollar, reduce global funding costs and stimulate cross-border capital flows into higher-growth regions, particularly Asia. For CICC, easier global liquidity conditions could translate into increased deal-making, underwriting activity and portfolio rebalancing into Chinese assets. This macro backdrop would enhance the appeal of Chinese equities and bonds, further supporting CICC’s investment banking and trading revenue streams while improving financing conditions for its corporate clients.

Strategic expansion into Southeast Asia to diversify growth. CICC’s private equity arm, CICC Capital, is partnering with Malaysia Digital Economy Corp to launch a US$100mn fund targeting the country’s gaming industry, part of a broader move by state-backed Chinese investment banks to deploy over US$1bn in Southeast Asia. This expansion aligns with Beijing’s “China plus N” strategy, helping Chinese corporates diversify supply chains and tap into Southeast Asia’s high-growth sectors such as AI, renewable energy, advanced manufacturing and healthcare. With China already the region’s largest trading partner, CICC’s regional presence will deepen cross-border investment flows, diversify revenue beyond the domestic market and position the firm to capture value from rising bilateral trade and digital economy initiatives.

1Q25 results review. 1Q25 revenue rose by 47.7% to RMB5.72bn, compared to RMB3.87bn in 1Q24. Profit attributable to shareholders rose 64.9% to RMB2.04bn in 1Q25, compared to RMB1.24bn in 1Q24. Basic earnings per share was RMB0.382 per share compared to RMB0.223 in 1Q24.

Market consensus.

(Source: Bloomberg)

Arm Holdings Plc (ARM US): Ramping up growth ambitions

BUY Entry – 125 Target – 141 Stop Loss – 117

ARM Holdings PLC operates as a holding company. The Company, through its subsidiaries, designs and manufactures semiconductor technology and other related products such as computer processors, memory controllers, internet protocol system, graphic processor, security, and storage devices. ARM Holdings serves automotive, infrastructure, and consumer technologies markets worldwide.

Strategic talent acquisition to accelerate in-house chip ambitions. Arm’s recruitment of Amazon AI chip veteran Rami Sinno highlights a strategic pivot from its traditional IP licensing model toward building complete chips and chiplets. Historically, Arm has only designed architectures and instruction sets for customers like Apple, Nvidia and Qualcomm. By investing profits into developing its own finished chips and subsystems, Arm is moving closer to vertically integrated solutions, addressing high-performance AI workloads and competing more directly with Nvidia and custom hyperscaler silicon. While execution risk remains high, bringing in top-tier talent from Amazon, HPE, Intel and Qualcomm demonstrates management’s commitment to building internal expertise and closing capability gaps.

Record licensing and royalty growth underscores resilient business model. Arm delivered record quarterly revenue of US$1.05bn, crossing the US$1bn milestone for the second consecutive quarter. Royalty revenue surged 25% YoY to US$585mn, fuelled by growing adoption of the Armv9 architecture, ramping Compute Subsystem (CSS) deployments and stronger data centre penetration. With over 70,000 enterprises now running workloads on Arm Neoverse-based chips, a 14x increase since 2021, Arm’s ecosystem momentum is accelerating. CSS, which reduces development time and costs for partners, has secured design wins across automotive, datacentre and PC markets, including engagements with leading OEMs such as Tesla, Mercedes-Benz, Samsung and Xiaomi. These highlight Arm’s ability to monetize innovation through recurring royalty streams, even as it experiments with direct chip development.

1Q26 earnings review. Revenue rose 11.8% YoY to US$1.05bn, missing estimates by US$10mn. Non-GAAP EPS was US$0.35, in-line with estimates. Arm expects second-quarter revenue in the range between US$1.01bn and US$1.11bn, which was in line with US$1.05bn expected by analysts.

BlackRock, Inc. provides investment management services. The Company offers investment, advisory, and risk management services. BlackRock serves individuals, families, educational, governments, insurance companies, and non profit organizations worldwide.

401(k) alternative investment access. The new Trump policy opening 401(k) plans to alternative assets such as private equity, infrastructure and private credit aligns perfectly with BlackRock’s dominant position in target-date funds and defined-contribution plan distribution. BlackRock has announced it will launch target-date funds in 2026 that integrate private equity and private credit allocations of 5%-20% depending on investor age, partnering with Great Gray Trust to bring these products to market. Retirement savings already represent over half of BlackRock’s AUM, and the firm estimates private market exposure could enhance returns by roughly 50 basis points annually, creating a substantial competitive advantage as plan sponsors seek yield-enhancing, policy-compliant solutions.

Expansion via M&A in private markets. Acquisitions like Global Infrastructure Partners, HPS Investment Partners, Preqin, and future acquisition of ElmTree Funds, have built a private-markets platform capable of managing the very asset classes now eligible for retirement accounts under the new policy. With private markets potentially comprising 20% of future retirement portfolios, BlackRock’s scale in illiquid assets, combined with its operational, compliance, and risk management infrastructure, positions it to address liquidity, transparency and governance challenges. In a lower-rate environment where return generation is more difficult, the firm’s expanded alternative asset capacity and deep integration with the retirement channel give it both first-mover advantage and the ability to capture outsized flows as the market adapts to the policy shift.

2Q25 earnings review. Revenue rose 12.7% YoY to US$5.42bn, missing by US$40mn. Non-GAAP EPS was US$12.05, topping forecasts by US$1.23. Blackrock declared US$5.21/share quarterly dividend, inline with previous to be distributed on 23 September.