20 July 2022: Keppel DC REIT (KDCREIT SP), Sinopharm Group Co., Ltd. (1099 HK)

Singapore Trading Ideas | Hong Kong Trading Ideas | Market Movers | Trading Dashboard

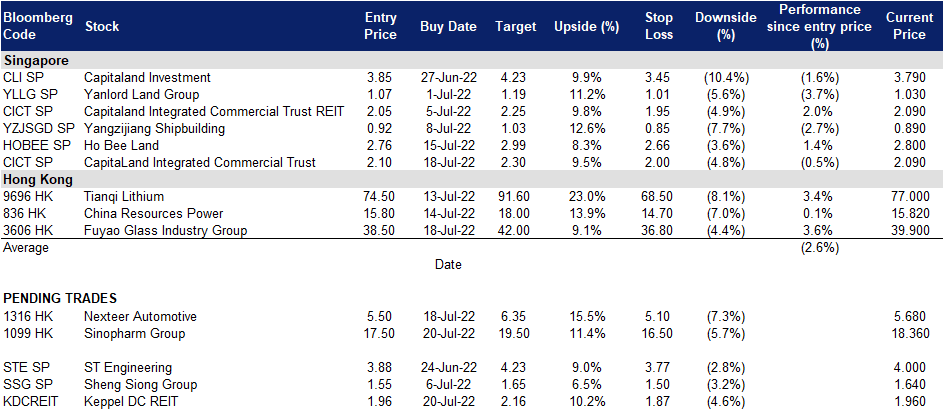

Keppel DC REIT (KDCREIT SP): Undervalued DC play could see mean reversion post 1H22 results

- BUY Entry 1.96 – Target – 2.16 Stop Loss – 1.87

- Keppel DC REIT is the first pure-play data centre REIT listed in Asia on SGX. KDCREIT’s investment strategy is to invest in a portfolio of income-producing real estate assets which are used primarily for data centre purposes as well as real estate-related assets. With a portfolio of assets located in key data centre hubs across Asia Pacific and Europe, the Manager aims to deliver sustainable returns to investors by capturing value from the data centre industry.

- 1H22 results to see continued support from past acquisitions. Contributions from its previously acquired Eindhoven DC, Guangdong DC, London DC, and the completion of AEIs at its DC1 and Intellicentre3 development will continue to support topline revenue. Nonetheless, we expect NPI margins to continue to be afflicted by strong energy prices, we note that MSCI Global Energy Index only peaked in early June but has been on the downtrend ever since, indicating that energy prices may have peaked.

- Demand for DCs continues to be strong, supply deluge may provide a cap floor. According to Cushman & Wakefield, demand for contiguous 10MW or more blocks of DC capacity continues to be strong. In fact, 18 markets that the firm tracks are currently now in sub-teen vacancies, double the number from 2021. This has led to continued growth in data center construction globally, providing ample acquisition opportunities for KDCREIT. In 2022, Cushman & Wakefield is expecting 4.1 GW (2021: 2.9GW) of DC capacity to be developed. Notably, London (prior KDCREIT acquisition) is a key location that is developing supply rapidly. Other Markets include Hong Kong and Jakarta.

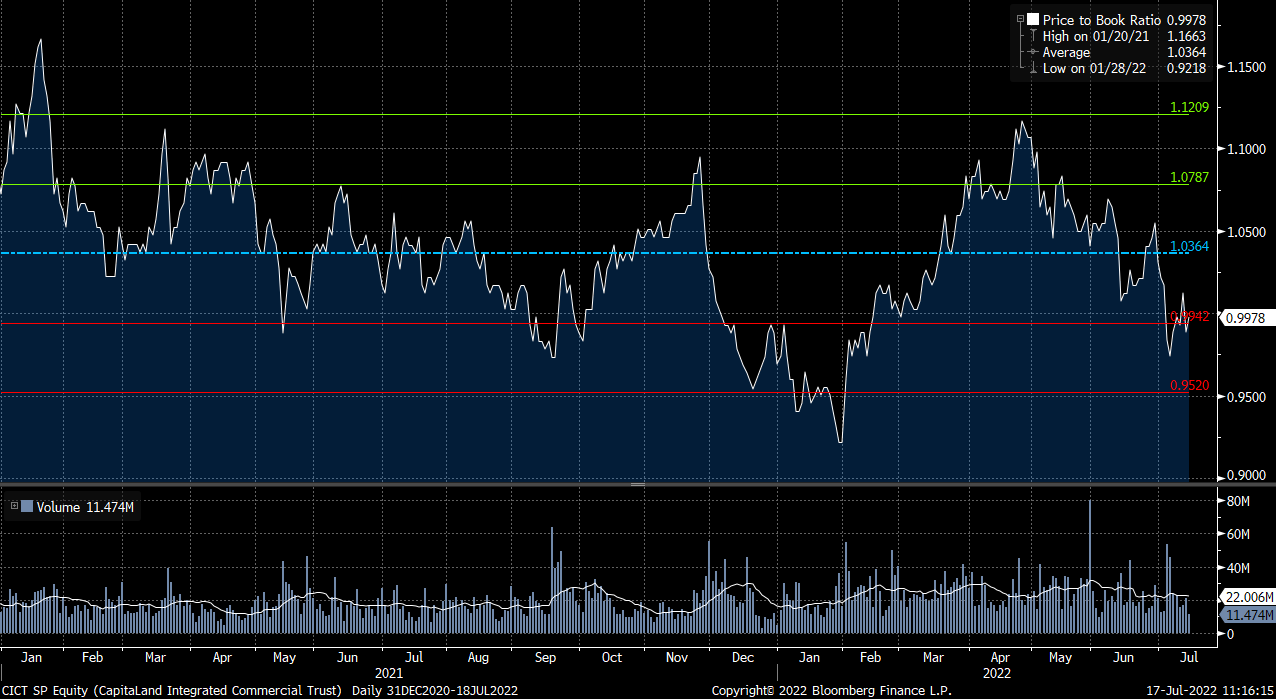

- Post 1Q22 correction may have been overdone. Recall that in 1Q22, KDCREIT reported flat DPU of S$0.02466 apiece (+0.2% YoY). Investors were worried that NPI margin contraction to 91% from 91.5% could spill over especially in an inflationary environment. This has led to a number of Street downgrades, resulting in 5/7/1 BUY/HOLD/SELL ratings and an average TP of S$2.29. Based on consensus estimates, FY22F gross revenue should swell 7.8% YoY, while NPI should nodge a lower but still respectable 4.7% YoY increase. FY22F DPU growth should come in at 2% YoY to S$0.101 apiece. We believe that KDCREIT is trading at a significant discount to its historical trading range considering that it is currently trading ~2sd away from its 2-year mean of ~2.1x P/B. At current prices, KDCREIT would trade at an attractive 5.1%/5.4% FY22F/23F yield.

CapitaLand Integrated Commercial Trust (CICT SP): Position for strong set of results on 28 July

- RE-ITERATE BUY Entry 2.10 – Target – 2.30 Stop Loss – 2.00

- CICT owns and invests in quality income-producing assets primarily used for commercial (including retail and/ or office) purposes, located predominantly in Singapore. As the largest proxy for Singapore commercial real estate, CICT’s portfolio comprises 21 properties in Singapore and two in Frankfurt, Germany, with a total property value of S$22.5bn as of 31 December 2021. CICT is managed by CapitaLand Integrated Commercial Trust Management Limited, a wholly-owned subsidiary of CapitaLand Investment Limited (CLI), a leading global real estate investment manager with a strong Asia foothold.

- Easing of pandemic restrictions from April 2022 to bolster office portfolio. We reckon that the substantial easing of pandemic restrictions in Singapore would provide significant tailwinds to CICT’s office properties. On its office portfolio, anecdotal evidence suggests that the large crowds seen in the core central region on weekdays implies that the return to office community has swelled (22 April 2022: 47%), and should result in greater leasing traction and in turn rental reversions. In addition, we believe that the acquisition of a 70%-stake in CapitaSky on 27 April 2022 will reap immediate benefits to this segment.

- Return of the tourist dollar on eased travel restrictions. According to STB, Singapore clocked 1.5m visitor arrivals in 1H22, more than 12x more on a YoY basis. Meanwhile, 1Q22 tourist dollars climbed to S$1.33bn (+213% YoY) driven by feeder markets such as Indonesia and India. Nonetheless, this is still a far cry from pre-pandemic spending of S$6.6bn in 1Q19. Moving forward, there is increasing optimism that global travel will start to pick up pace and the agency believes that Singapore can expect to receive between 4 to 6 million visitors this year, which would fuel tourism spending particularly along the downtown Orchard road belt.

- FY22 results to be fueled by M&As. Recall that in1Q22, CICT already started to see a recovery across its portfolio and reported strong office rental reversion of 9.3%, while its retail rental reversions saw a slight 1.2% increase after excluding Raffles City Singapore’s AEI. The Street is thus overall bullish on CICT’s prospects, with 16/3/1 BUY/HOLD/SELL ratings and an average TP of S$2.45. Based on consensus estimates, FY22F gross revenue and NPI should swell 7.0/8.3% YoY, while distributable income would grow at a faster 12.5% pace. FY22F DPU should come in at 9.3% YoY to S$0.114 apiece due mainly to a larger unit base. We believe that CICT is slightly undervalued now considering that it is currently trading ~1sd away from its post-merger mean of ~1.04x P/B. At current prices, CICT would trade at an attractive 5.4%/5.7% FY22F/23F yield.

Sinopharm Group Co., Ltd. (1099 HK): A defensive counter amidst a market downturn

- BUY Entry – 17.5 Target – 19.5 Stop Loss – 16.5

- Sinopharm Group Co Ltd is a China-based company principally engaged in pharmaceutical and medical devices distribution business. The Company operates its business through four segments. Pharmaceutical Distribution segment is engaged in the distribution of pharmaceutical products to hospitals, other distributors, retail pharmacy stores and clinics. Medical Devices segment is engaged in the distribution of medical devices, as well as provides installation and maintenance services. Retail Pharmacy segment is engaged in the operation of chain pharmacy stores. Other Business segment is engaged in the distribution of laboratory supplies, manufacture and distribution of chemical reagents, production and sale of pharmaceutical products.

- 1Q22 earnings review. 1Q22 revenue grew by 6.86% YoY to RMB17.15bn. Net profit attributable to shareholders dropped by 23.25% YoY to RMB252.36mn. The decrease in profit was mainly attributable to the decline in the results of Sinopharm Accord’s associates due to the impact of the Covid-19 pandemic, which resulted in a corresponding decrease in investment income of Sinopharm Accord. At the same time, due to the impact of the pandemic, the retail sector has seen a decline in store traffic, and the new stores opened in 2021 cost a large initial investment, the benefits of which have not yet emerged, resulting in a decrease in the margin levels.

- A defensive stock amidst a market downturn. The Hong Kong market has been hammered by both a slowdown in China’s economy and geopolitical risks. Growth, value, and cyclical sectors, as well as other thematic stocks, have been sold off indiscriminately. However, this stock is relatively outperforming the rest as its business is largely immune to inflation and policy risks. The business driver is the distribution volume rather than profit margins. The growth in demand for medicines and medical devices is stable with low price sensitivity.

- The updated market consensus of the EPS growth in FY22/23 is -0.6%/9.9% YoY respectively, which translates to 5.8x/5.3x forward PE. The current PER is 8.3x. The FY22F/23F dividend yield is 5.2%/5.7%. Bloomberg consensus average 12-month target price is HK$23.37.

(Source: Bloomberg)

Nexteer Automotive Group Ltd (1316 HK): Riding on the auto sector recovery

- RE-ITERATE Buy Entry – 5.50 Target – 6.35 Stop Loss – 5.10

- Nexteer Automotive Group Limited is an investment holding company. The Company through its subsidiaries are primarily engaged in the design and manufacture of steering and driveline systems, advanced driver assistance systems (ADAS) and automated driving (AD) and components for automobile manufacturers and other automotive-related companies. Its operations are in the United States of America (USA), Mexico, Poland and the People’s Republic of China (China). The principal markets for the Company’s products are North America, Europe, South America, China and India. The Company has approximately 27 manufacturing plants, one global technical center, over two regional technical centers, one software service center and approximately 13 customer service centers. Its subsidiaries include Nexteer US Holding I LLC, Rhodes I LLC, Steering Solutions IP Holding Corporation, Chongqing Nexteer Steering Systems Co., Ltd., CNXMotion, LLC and Dongfeng Nexteer Steering Systems (Wuhan) Co., Ltd.

- Auto sales recovered in June. Automobile sales in China expanded 23.8% YoY to 2.5 mn units in June of 2022, boosted by government incentives to support the industry and a recovery in production, particularly in coronavirus lockdown-hit Shanghai, according to the China Association of Automobile Manufacturers. The auto part manufacturer sector also followed the recovery, but we still think the upside potential is bigger.

- New orders to uphold the growth. In 1Q22, the total value of new order signed amounted to US$2.73bn, four times of the total value signed in 1Q21. With the recovery in the auto markets in Europe and Asia Pacific, the oder book is expected to grow healthily in FY22.

- Updated market consensus of the EPS growth in FY22/23 is 19.4%/52.5% YoY respectively, which translates to 12.3x/8.1x forward PE. The current PER is 15.6x. Bloomberg consensus average 12-month target price is HK$6.67.

(Source: Bloomberg)

United States

Top Sector Gainers

| Sector | Gain | Related News |

| Apparel/Footwear | 4.91% | Consumer discretionary stocks gain as investors dabble with beat-up names Nike Inc (NKE US) |

| Industrial Machinery | +4.63% | U.S. Senate set to pass $52bn CHIPS Act Applied Materials Inc (AMAT US) |

| Semiconductors | +4.35% | Chip designers warm to U.S. bill despite big benefits to Intel NVIDIA Corp (NVDA US) |

- Goldman Sachs Group Inc/The (GS US) rose 5.6% to lead the Dow Jones Industrial Average higher, building on the bank’s post-earnings gains. Other bank stocks traded higher alongside Goldman.

- Boeing Co (BA US) rose 5.7%, continuing an upward trend for the stock, after Boeing announced several deals for plane orders. The deals include an order for five 787 Dreamliners from AerCap and orders for 737 Max jets from Aviation Capital Group and 777 Partners. Shares of Boeing are up more than 10% in July.

- International Business Machines Corp (IBM US) slipped 5.2% after the tech company warned of a potential $3.5 billion hit from a strong U.S. dollar. That warning overshadowed better-than-expected earnings and revenue for the previous quarter.

- Cruise line and airline stocks surged as investors continue to debate consumer health and the potential for a recession — while travel demand remains strong. Royal Caribbean Cruises Ltd (RCL US) and Carnival Corp (CCL US) gained 5.8% and 7.4% respectively.

Singapore

- Genting Singapore Ltd (GENS SP) shares continued to fall 2.5% yesterday, after the company said on Sunday that it is not aware of nor involved in any ongoing discussions on a potential transaction involving the company.

- First Resources Ltd (FR SP) shares fell 2.9% yesterday. Asian buyers are ramping up palm oil purchases to replenish inventories after prices corrected to their lowest in a year and as top producer Indonesia has scrapped levies on exports. The market is anticipating higher supplies from Indonesia after scrapping its export levy last week for all palm oil products until Aug. 31 to boost exports and ease high inventories.

- Golden Energy & Resources Ltd (GER SP) and Geo Energy Resources Ltd (GERL SP) shares fell 2.1% and 1.3% respectively yesterday. “China is unlikely to change its coal policy as the backstop of energy security in the near future. National policy is unlikely to encourage gas demand in a significant manner due to concerns over supply chain pressure and affordability.” said Wood Mackenzie research director Miaoru Huang. While China remains committed to long-term climate goals, the immediate focus is to guarantee energy supply and stabilise energy costs. The national 14th five-year energy plan, unveiled in March, re-emphasised coal as the backstop of energy security.

- NIO Inc (NIO SP) shares fell 1.9% yesterday. The negative shift in the market perception of risk sentiment after a report that Apple Inc. would slow hiring and spending knocked down the major US indices at the start of the week. The downside in the NIO stock price still remained cushioned as investors cheered easing bets of aggressive Fed tightening. China’s pledge to support economic growth also saved the day for NIO stock buyers.

Hong Kong

Top Sector Gainers

| Sector | Gain | Related News |

| Textile & Apparels | +1.87% | NA ANTA Sports Products Ltd (2020 HK) |

| Marine & Harbour Services | +1.15% | China’s Tianjin halts some businesses in fresh COVID-19 curbs Orient Overseas (International) Limited (316 HK) |

| Construction Materials | +1.05% | Multiple real estate projects resume construction in China after homebuyers refuse to pay their mortgages for unfinished housing China Shanshui Cement Group Limited (691 HK) |

Top Sector Losers

| Sector | Loss | Related News |

| Alcoholic Drinks & Tobacco | -2.65% | Why is Chinese beer rising in popularity in Pakistan? Tsingtao Brewery Co Ltd (168 HK) |

| Toys | -1.66% | NA Pop Mart International Group Ltd (9992 HK) |

| Electricity Supply | -1.26% | Searing Heat Tests China’s Ability to Keep Its Factories Running China Longyuan Power Group Corp Ltd (916 HK) |

- BYD Electronic International Co Ltd (0285 HK) shares fell 8.9% yesterday. Apple slowed down recruitment, and Apple concept stocks fell. Apple plans to slow hiring and spending growth in some divisions next year in response to a potential recession. However, the change is not for all teams as Apple still plans to have an aggressive product release schedule in 2023.

- Kingboard Laminates Holdings Ltd (1888 HK) and Kingboard Holdings Ltd (0148 HK) shares fell 6.5% and 4.6% respectively yesterday. Kingboard Laminates announced that it expects to achieve a net profit of approximately HK$1.7 billion to HK$2 billion for the six months ended June 30, 2022, a decrease of approximately 40% to 49% compared with the same period last year. Kingboard Group announced that the group expects the group to record a net profit of approximately HK$2.2 billion to HK$2.7 billion for the six months ended June 30, 2022, a decrease of approximately 47% to 57% compared to the same period last year. The expected decline in net profits are mainly due to the decline in the sales volume and unit price of the Group’s copper clad panel products and the provision for credit losses on the bond investments held by the Group.

- Huabao International Holdings Ltd (0336 HK) shares rose 8.2% yesterday. On July 7, according to the official website of the State Tobacco Monopoly Administration, Shenzhen Liyi Technology Co Ltd, a wholly-owned subsidiary of Huabao International, obtained an electronic cigarette production licence. In terms of exports, according to the “Administrative Measures for Electronic Cigarettes”, exports must comply with the laws and regulations of the destination country. It is expected that there are no specific production scale requirements for export licences, and companies are expected to obtain orders by virtue of their competitive advantages.

- SITC International Holdings Co Ltd (1308 HK) shares rose 6.0% yesterday. On July 18, four express delivery companies released their June business briefings, showing that the development of the express delivery industry is picking up. Analysts from Dongxing Securities believe that the express delivery industry is showing a clear recovery trend. Data from the State Post Bureau shows that in the first half of the year, the express delivery business volume is expected to exceed 50 billion parcels, a yearly increase of about 3.6%; business income is expected to be close to 500 billion yuan, a yearly increase of about 2.8%; the average daily business volume has recovered to more than 300 million parcels, exceeding the same period last year.

Trading Dashboard Update: Cut loss on iX Biopharma (IXBIO SP) at S$0.17.