KEY METRICS | EXECUTIVE SUMMARY | ECONOMIC OUTLOOK | MARKET OUTLOOK | KEY SECTOR INDICATOR | SECTOR POSITIONING & STYLE PREFERENCES | KGI TOP 5 PICKS

Executive Summary

Singapore enters 2H26 from a position of macro resilience, with growth still supported by electronics, wholesale trade, finance, professional services and government policy support. However, the pace of growth is likely to moderate from the strong 1H26 base as external demand normalises, tariff effects become more visible, and outward-facing sectors face a less supportive global backdrop. Inflation remains manageable but has moved higher from the low levels seen in 2025, prompting MAS to maintain a cautious appreciation-bias policy stance. Against this backdrop, we remain constructive on Singapore equities, supported by resilient corporate earnings, dividend yield, capital return potential, and policy-led efforts to deepen local equity market liquidity.

Singapore’s 2H26 growth outlook remains positive but moderating, with MTI maintaining its 2026 GDP growth forecast at 2.0%–4.0%. Inflation is expected to remain contained within MAS’ 1.5%–2.5% forecast range, while monetary policy remains cautiously tight through a modest appreciation path for the S$NEER.

We maintain an Overweight stance on Singapore equities, with a 12-month STI target range of 5,300–5,500, implying mid-single-digit price upside from current levels and a higher total return when including dividends. While valuation is no longer outright cheap after the strong rally, the market remains supported by earnings resilience, dividend yield, bank capital returns and policy-led liquidity catalysts.

The key themes for 2H26 are: i) AI-led export and manufacturing resilience, with the latest May NODX data showing continued strength in electronics and early broadening into selected non-electronics categories; ii) policy-led market re-rating, supported by MAS’ Equity Market Development Programme and broader efforts to deepen Singapore’s equity market; and iii) Quality and Yield demand, as investors continue to favour companies with strong balance sheets, visible cash flows and sustainable dividends.

We prefer Financials, Industrials / Infrastructure / Defence, and Quality Mid-Caps, while remaining selective on highly discretionary consumer names and highly levered real estate / lower-quality REITs. From a style perspective, we favour Quality and Yield over pure Growth, with selective exposure to AI-cycle beneficiaries and under-covered mid-caps with improving liquidity.

The main downside risks are external and earnings-driven: a renewed geopolitical or trade shock could weaken external demand and raise imported cost pressures, while earnings disappointment after the STI’s strong re-rating could trigger market consolidation, particularly in banks and other index-heavy names.

Singapore’s 2H26 growth outlook remains resilient but is expected to moderate from the strong 1H26 base. MTI maintained its 2026 GDP growth forecast at 2.0%-4.0%, after the economy expanded 6.0% YoY in 1Q26 and 1.0% QoQ on a seasonally adjusted basis. Growth should continue to be supported by electronics, precision engineering, wholesale trade, finance, and professional services, but the pace is likely to slow as external demand normalises and the US-Israel-Iran conflict weighs on energy costs and business confidence.

Singapore’s labour market remains resilient, but the latest release points to a clearer moderation in hiring momentum. Total employment increased by 9,400 in 1Q26, marking the 18th consecutive quarter of expansion since 4Q21, but this was slower than the 17,700 increase in 4Q25. The moderation was mainly due to slower non-resident employment growth, while resident employment growth improved from 3,100 in 4Q25 to 5,400 in 1Q26. Unemployment rates remained low and stable, with overall unemployment at 2.0%, resident unemployment at 2.9% and citizen unemployment at 3.1% in March 2026.

Fiscal policy remains targeted and counter-cyclical rather than broad-based stimulus. Budget 2026 support focuses on easing business cost pressures, strengthening workforce transformation, supporting household consumption and helping firms internationalise. Measures such as enhanced household support, corporate tax rebates and business cost relief should provide a modest cushion to domestic demand in 2H26.

The STI was trading around 5,195 in late June 2026, after reaching an intraday record high of 5,241.80 on 23 June and closing that session at 5,205.75. The index has therefore moved above the 5,000-5,150 range observed in mid-June. Based on the 12-month STI target range of 5,300-5,500, the latest index level implies approximately 2%-6% price upside, before dividends. While the market remains supported by resilient bank earnings, dividend income and policy-led liquidity initiatives, the stronger year-to-date re-rating reduces the available valuation margin of safety.

Aggregate STI EPS growth should remain positive but moderate in 2H26. Banks, SGX, ST Engineering, Sembcorp, Keppel, Singtel and selected industrials are likely to drive index-level resilience. REITs and developers may contribute to a lagged recovery if funding costs ease and rental growth stabilises.

We remain overweight Financials, but the 2H26 focus should shift from pure NIM expansion to the durability of fee income, wealth AUM growth, asset quality and capital returns. With interest rates moving lower, NIM compression is expected to continue across the banks, making wealth management, treasury customer flows and dividend visibility increasingly important.

Financials remain our preferred core overweight, with banks and market infrastructure names continuing to anchor Singapore equity returns. For banks, the key indicators are NIM / NII trajectory, AUM and wealth fee growth, credit costs, and dividend / capital return outlook. DBS continues to screen strongest on capital return and wealth scale, OCBC offers diversified earnings support from banking, wealth and insurance, while UOB remains the relative catch-up candidate with ASEAN wealth and loan growth optionality. While NIMs are likely to moderate as rates normalise, the sector remains supported by resilient asset quality, excess capital, attractive dividends and continued regional wealth inflows. For SGX, the key indicators are securities turnover, derivatives volumes, listing activity and liquidity uplift from MAS’ Equity Market Development Programme.

We remain selective on Real Estate and REITs. The sector should not be analysed only through the lens of interest rates, as the key issue is whether rental growth and occupancy can offset refinancing costs, capex requirements and valuation pressure. The strongest sub-segments are likely to be industrial, logistics, data-centre and essential retail REITs, where demand visibility, tenant stickiness and rental reversions remain relatively resilient. Office REITs remain more mixed, with prime Singapore office assets supported by tight supply, but overseas office exposure remains vulnerable to weaker leasing demand and higher cap rates. Hospitality REITs could benefit from tourism recovery and event-driven demand, but earnings remain more cyclical. Developers are likely to remain range-bound, as residential demand is stable but moderated by cooling measures, land cost discipline and slower asset revaluation gains.

We are overweight Industrials and Infrastructure Conglomerates, as the sector offers visible earnings growth from order books, long-cycle capex and recurring infrastructure income. The strongest areas are aerospace, defence, public-sector engineering, utilities, transport infrastructure, data-centre infrastructure and electrification-related work. Aerospace should benefit from travel normalisation, fleet maintenance demand and supply-chain recovery, while defence and public-security spending provide structural support. Infrastructure conglomerates should benefit from data-centre power demand, urban infrastructure, asset management growth and recurring income from utilities or concessions. The main risk is execution, as cost overruns, labour shortages and working capital needs can dilute order book quality.

We maintain a neutral but selective stance on Energy and Commodities. The sector has upside from geopolitical risk premiums, regional power demand, data-centre electricity needs and energy transition spending, but earnings remain sensitive to commodity prices and input cost volatility. The preferred exposure is contracted energy infrastructure, where earnings are supported by long-term power offtake, fuel cost pass-through or regulated / infrastructure-like returns. Power and utilities should benefit from rising electricity demand, particularly from data centres and industrial activity. Commodity producers and traders remain more cyclical, with earnings driven by spot prices, production volumes, inventory cycles and working capital swings. Agribusiness should be analysed through crush margins, palm oil / sugar cycles, China demand and hedging outcomes rather than commodity prices alone.

We maintain a neutral stance on Consumer and Telco. Consumer spending should remain steady but not strong, supported by a resilient labour market and government household measures, but external uncertainty and cost pressures may limit discretionary demand. Within consumer, staples and supermarkets remain the most defensive, supported by recurring household demand and better cost pass-through. F&B and retail are more mixed, as footfall may remain healthy but rental, labour and input costs continue to pressure margins. Discretionary retail remains the weakest sub-segment, especially for companies without strong brands or pricing power. For telcos, the sector remains defensive and yield-oriented, but re-rating requires better monetisation from enterprise, cybersecurity, cloud, 5G, data centres or regional associates.

We are selectively overweight Small and Mid-Caps, especially profitable, under-covered companies with visible earnings growth, strong balance sheets and shareholder return potential. The sector should be analysed less by industry classification and more by liquidity, earnings visibility, institutional ownership and catalyst strength. MAS’ Equity Market Development Programme should gradually improve market liquidity and research coverage, but the benefits will not be evenly distributed. The strongest candidates are quality mid-caps with positive earnings revisions, scalable platforms, order book visibility, dividend growth or corporate action catalysts. Lower-quality illiquid names without clear earnings drivers may continue to lag despite broader policy support.

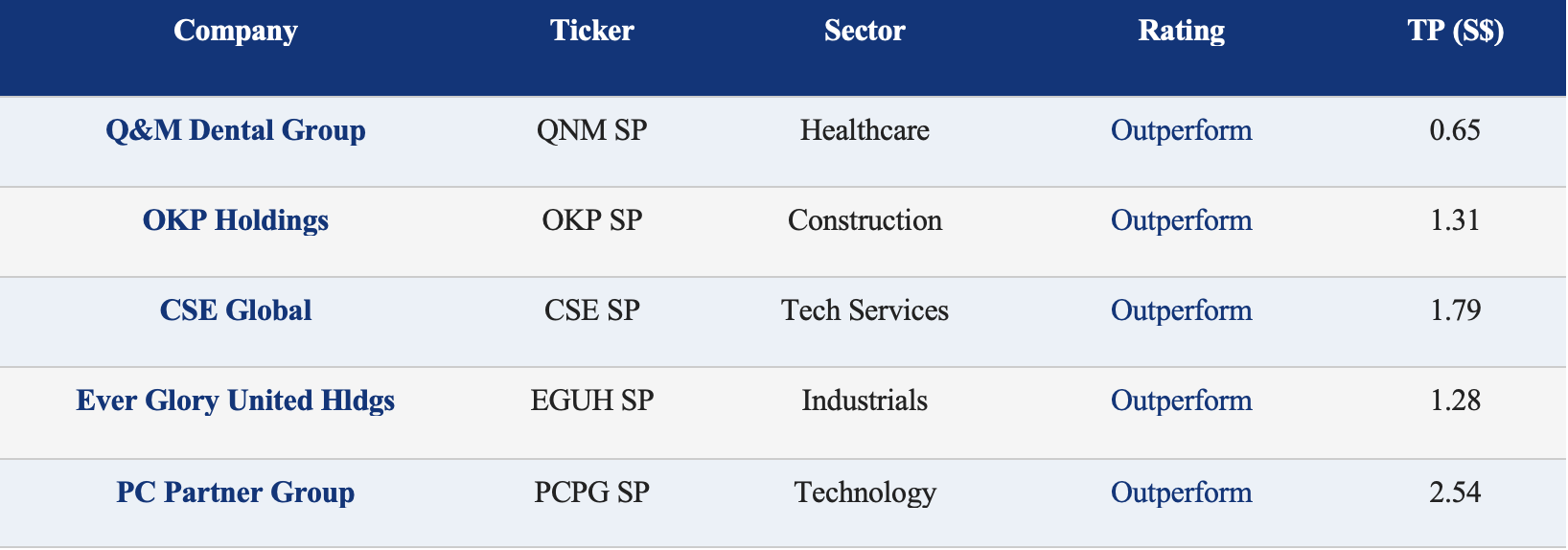

Based on our latest company updates and initiation coverage, we highlight five stocks from KGI’s Singapore coverage universe as our top picks for 2H26. These names offer a combination of earnings visibility, structural growth tailwinds and attractive risk-reward, and span healthcare, infrastructure, engineering and technology.