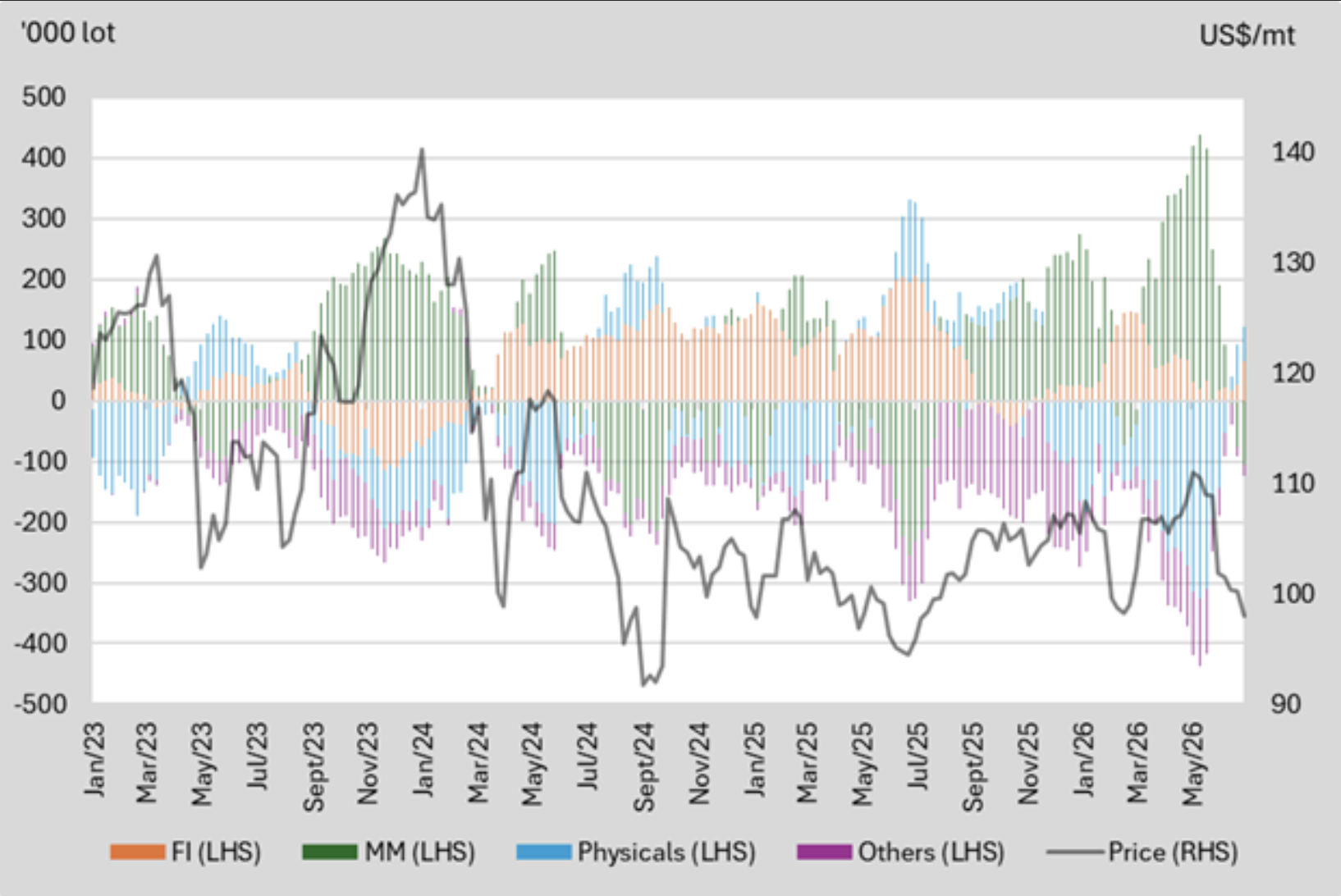

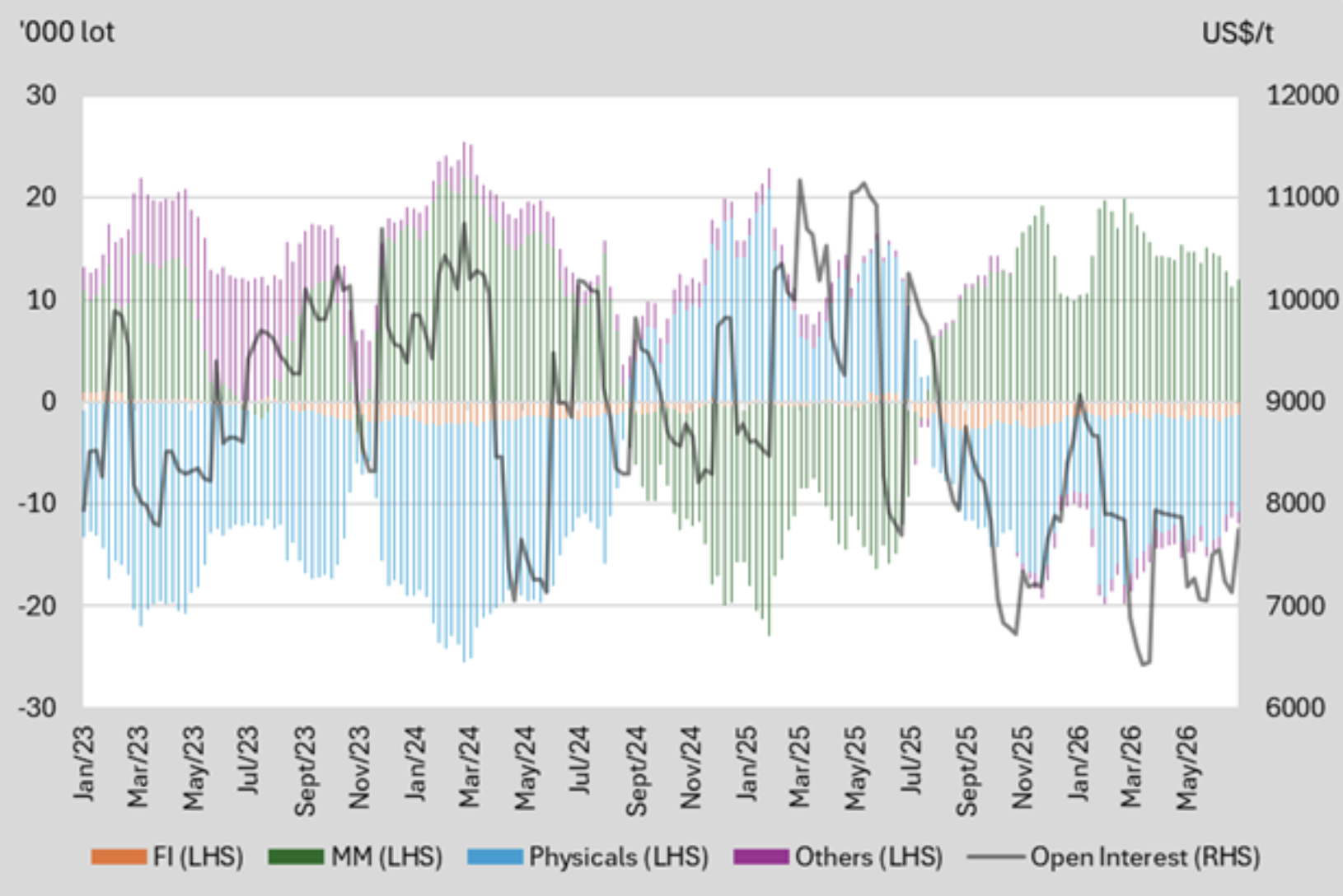

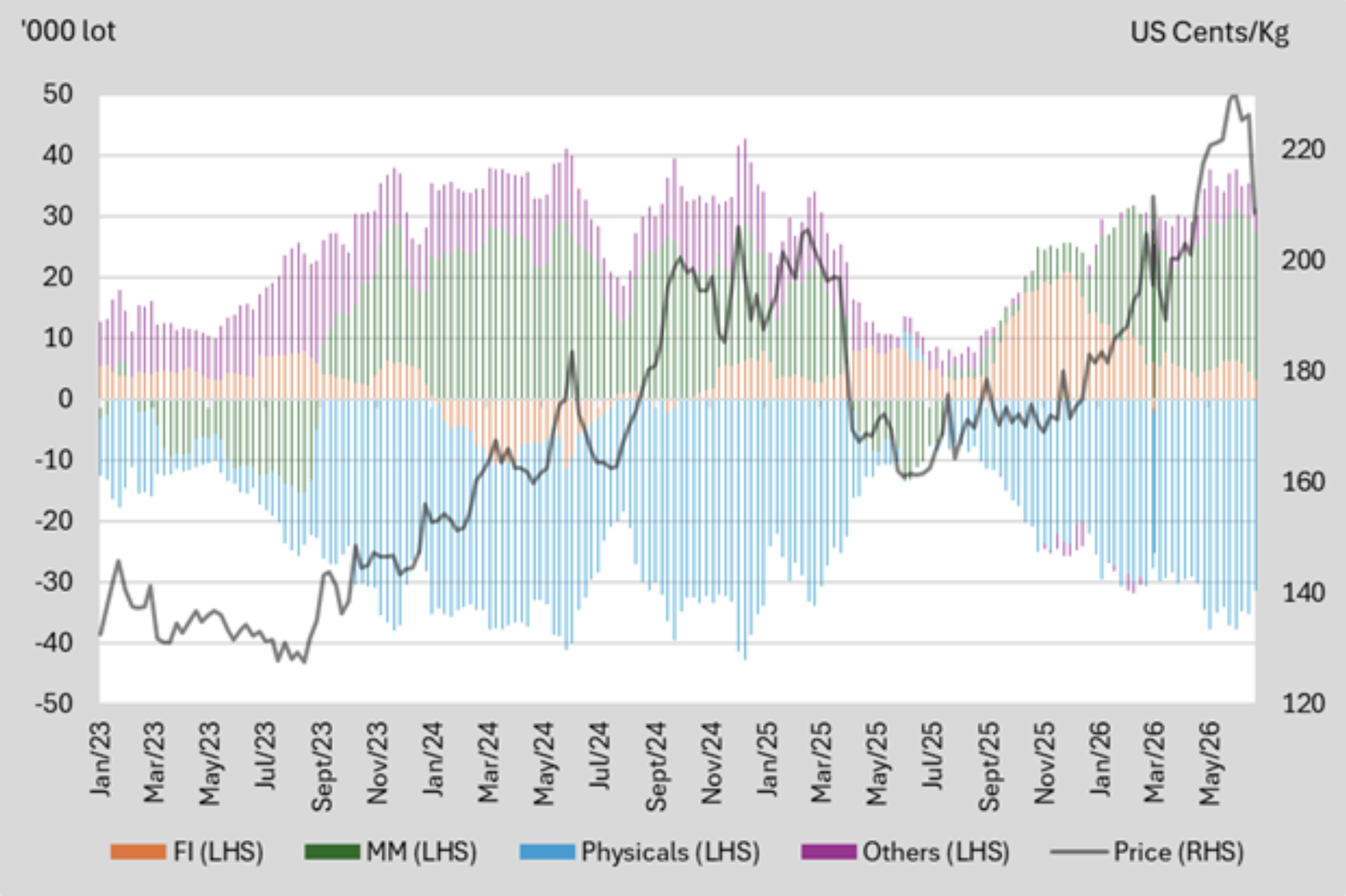

| Financial Institutions | An entity, such as a broker trading desk, bank trading desk or swap dealer, that uses the futures markets to manage or hedge the risk. |

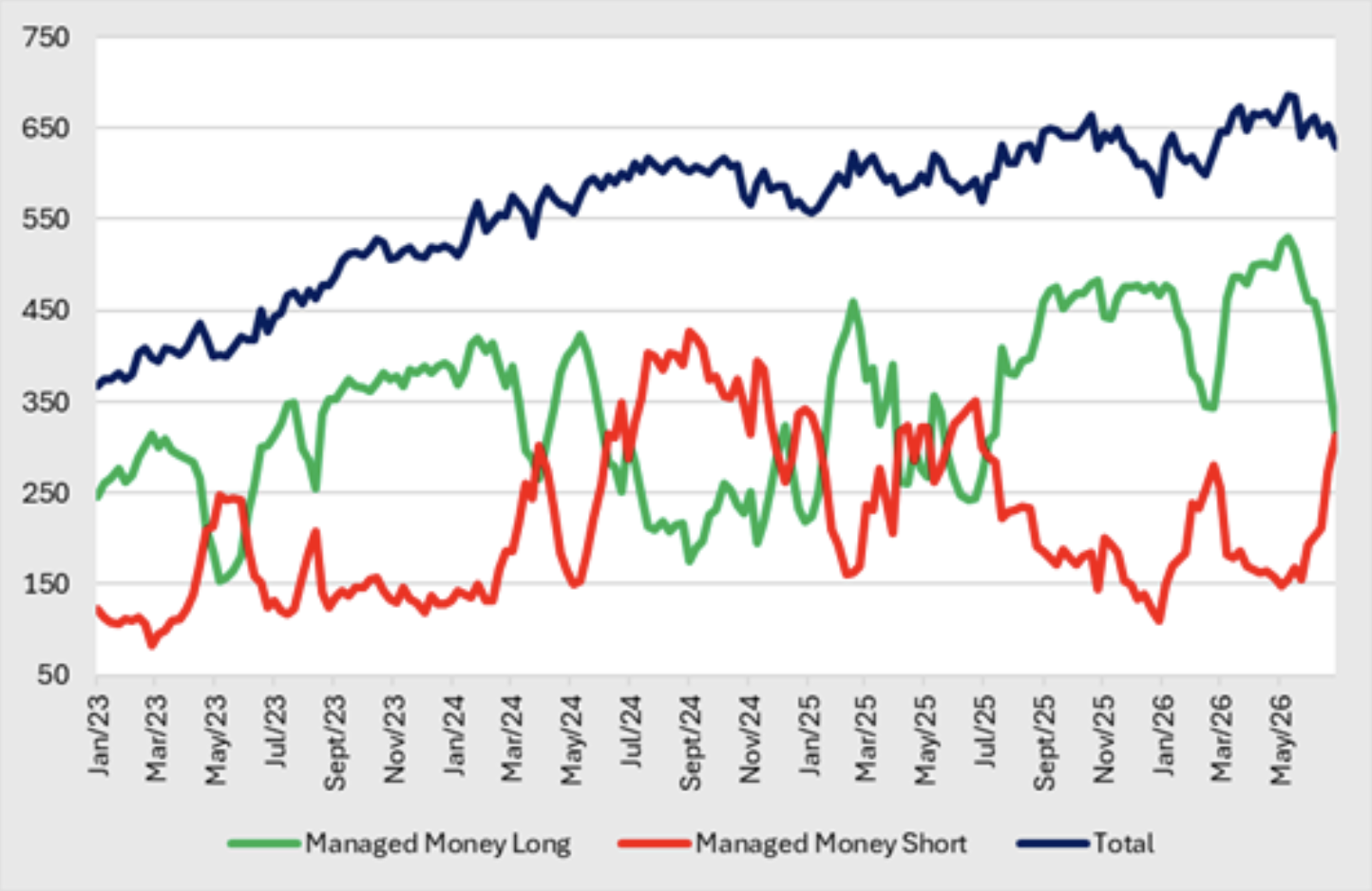

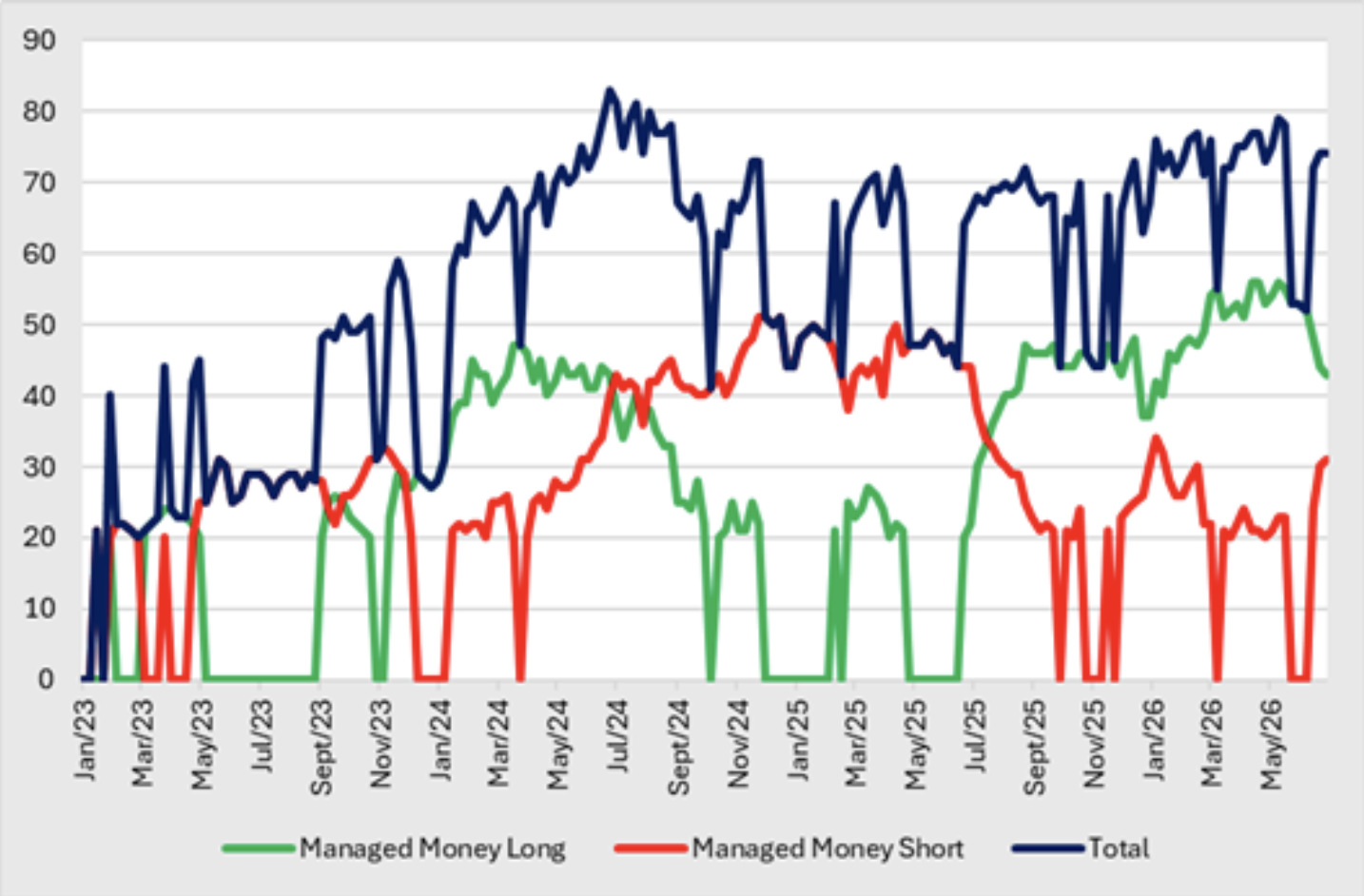

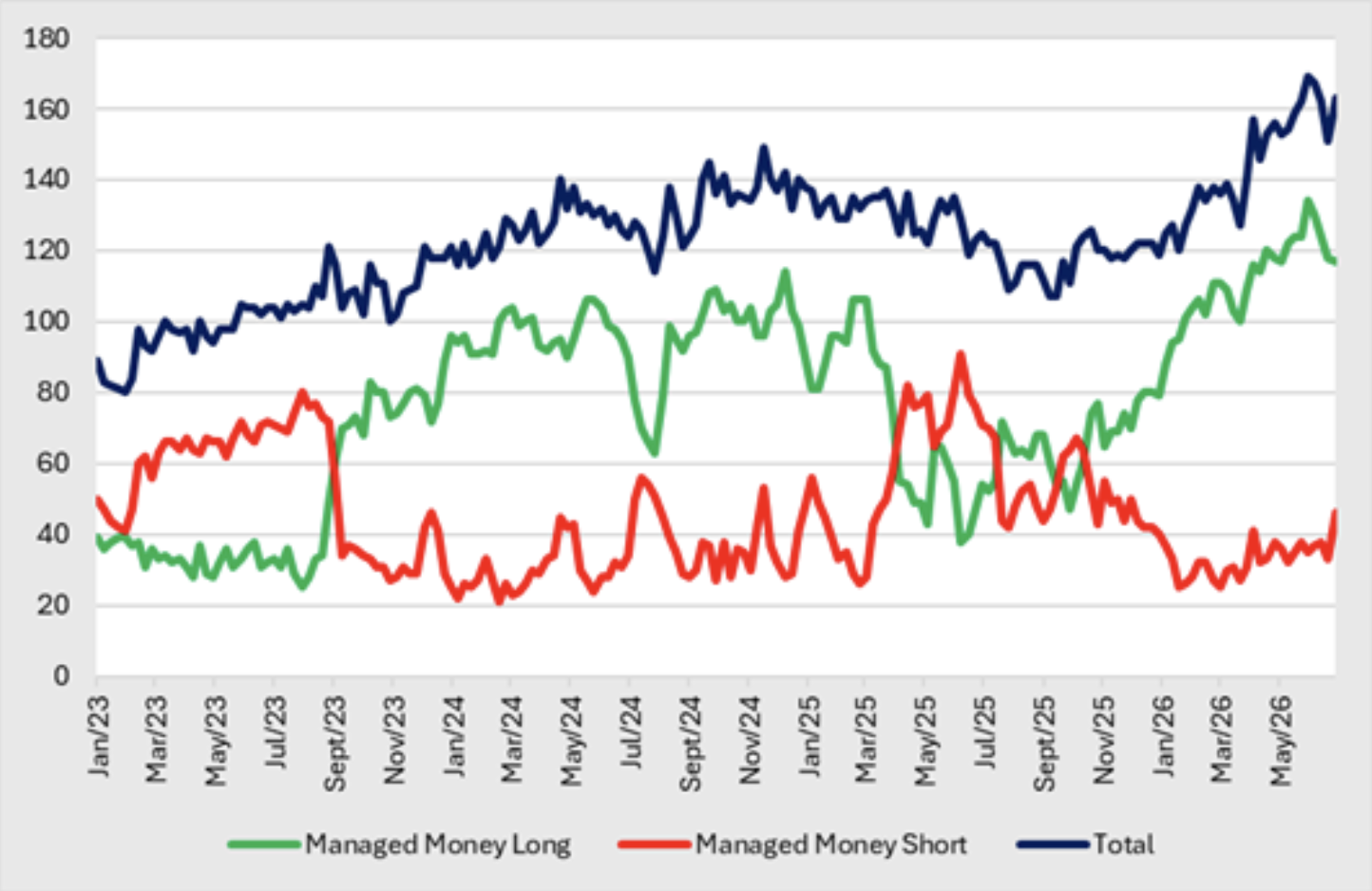

| Managed Money | An entity engaged in organised futures trading on behalf of funds or special investment vehicles — including pension funds, asset managers, hedge funds, proprietary trading groups and family offices. |

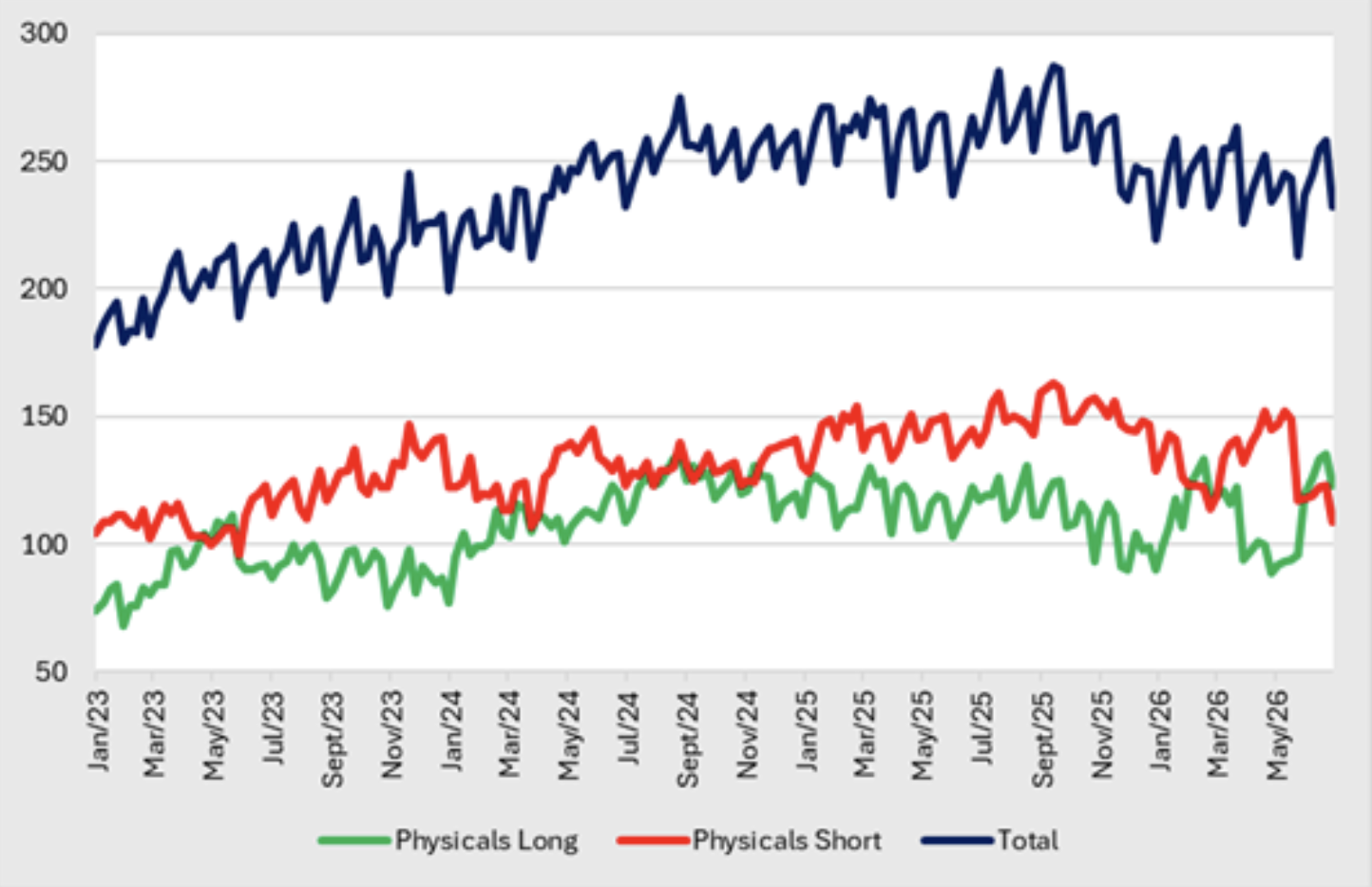

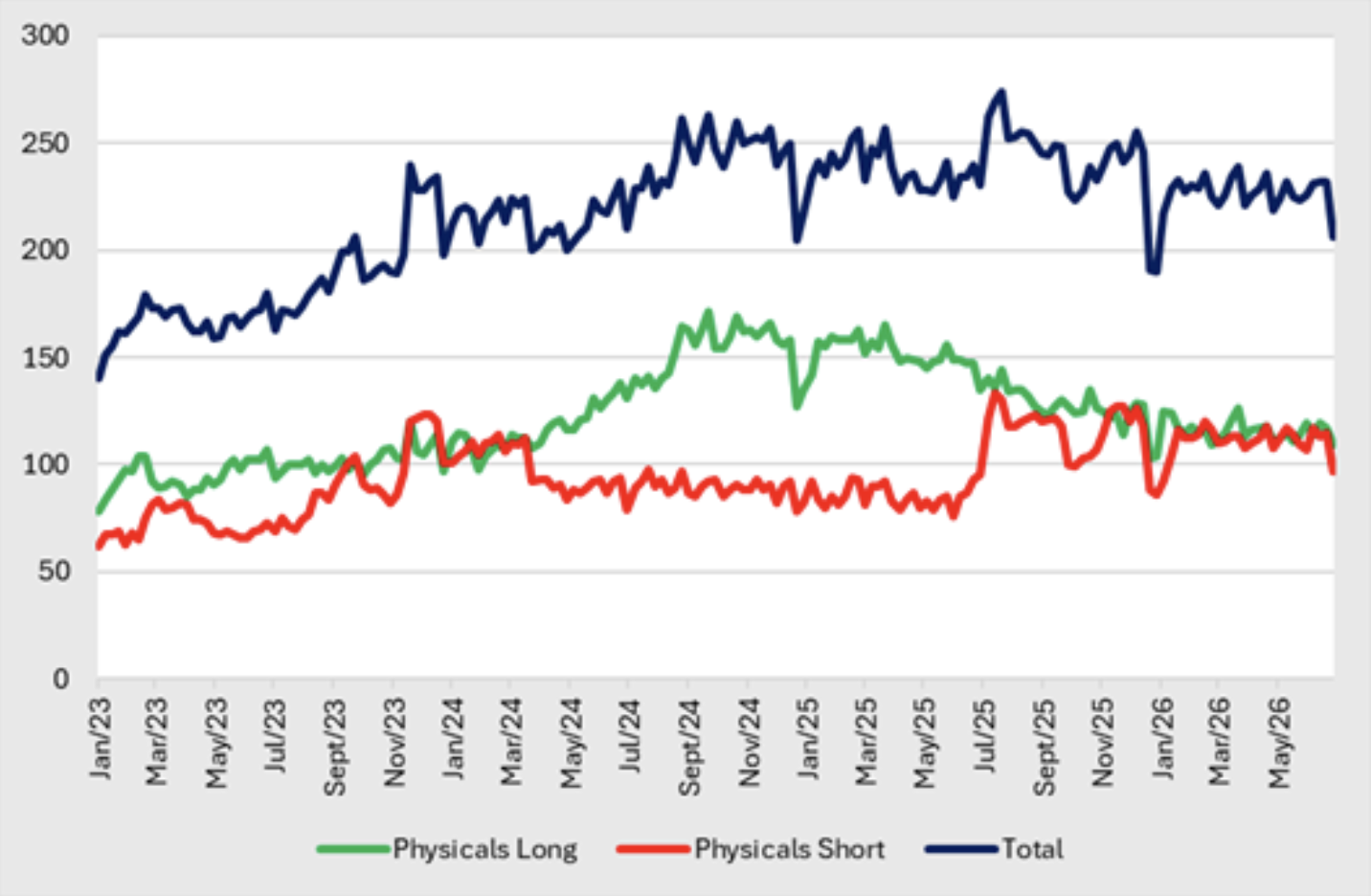

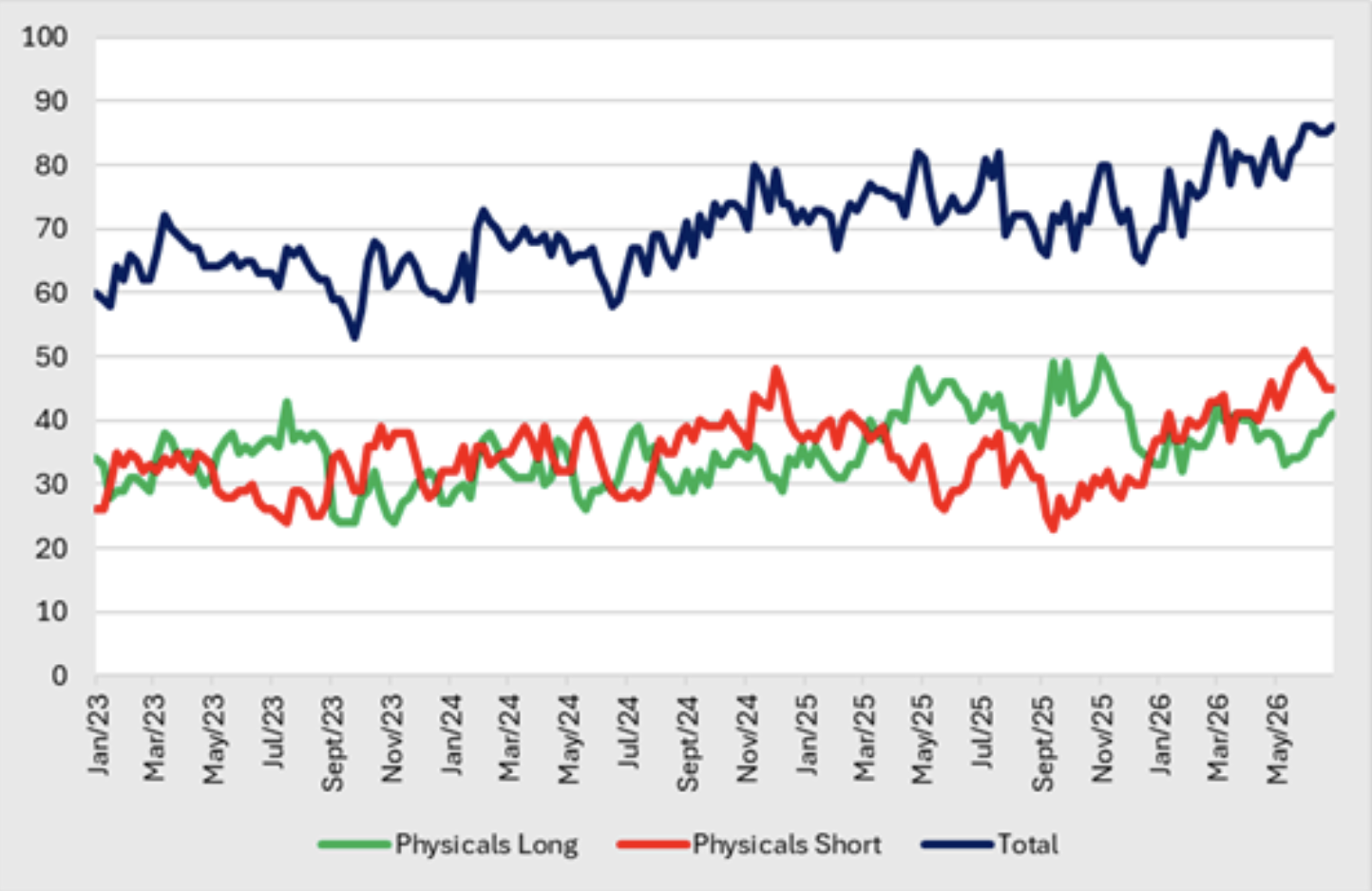

| Physicals | An entity that predominantly engages in the physical markets and uses futures to manage or hedge risks associated with production, processing, trading, packing, handling, transportation, warehousing or distribution of a physical commodity. |

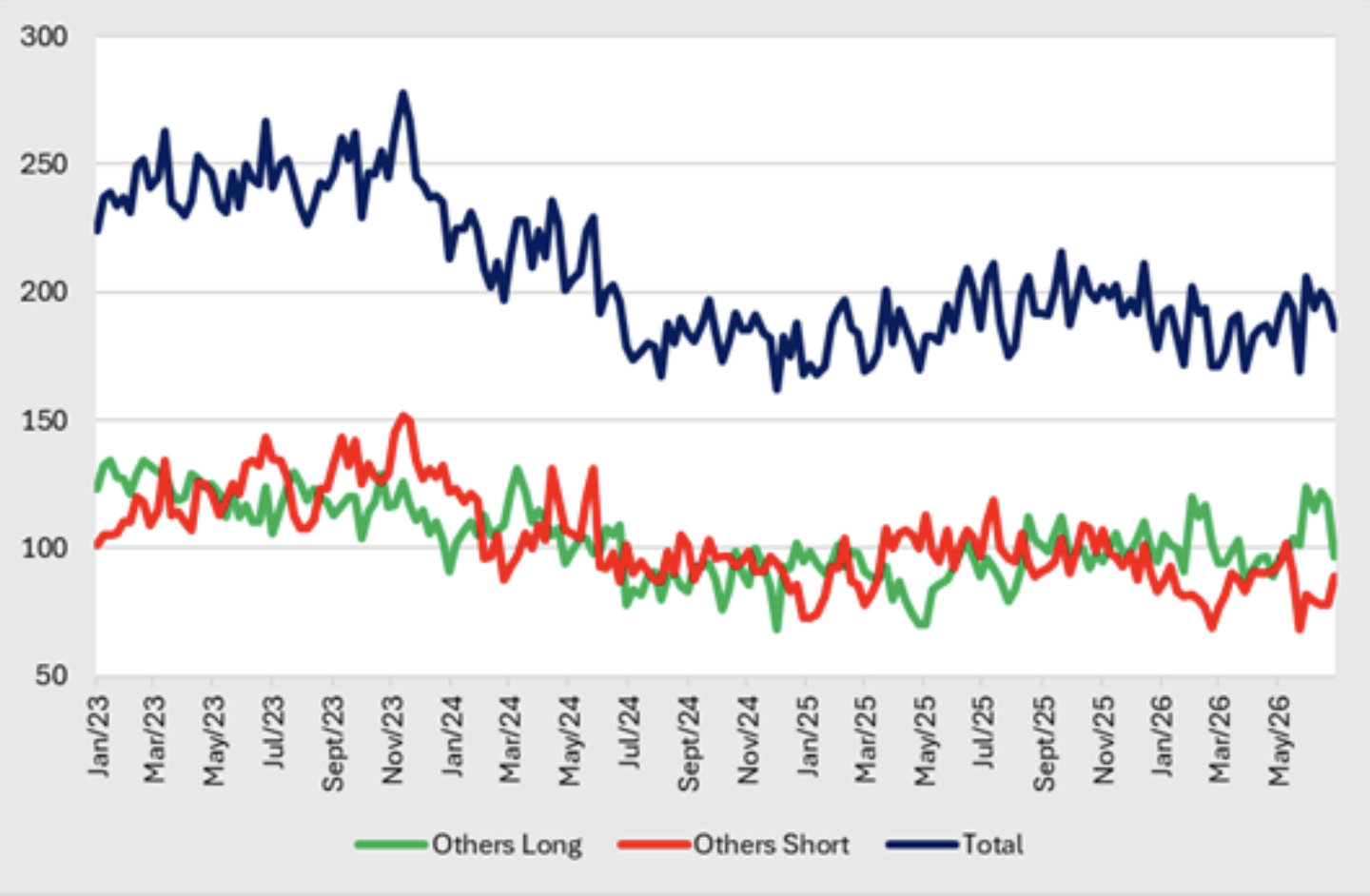

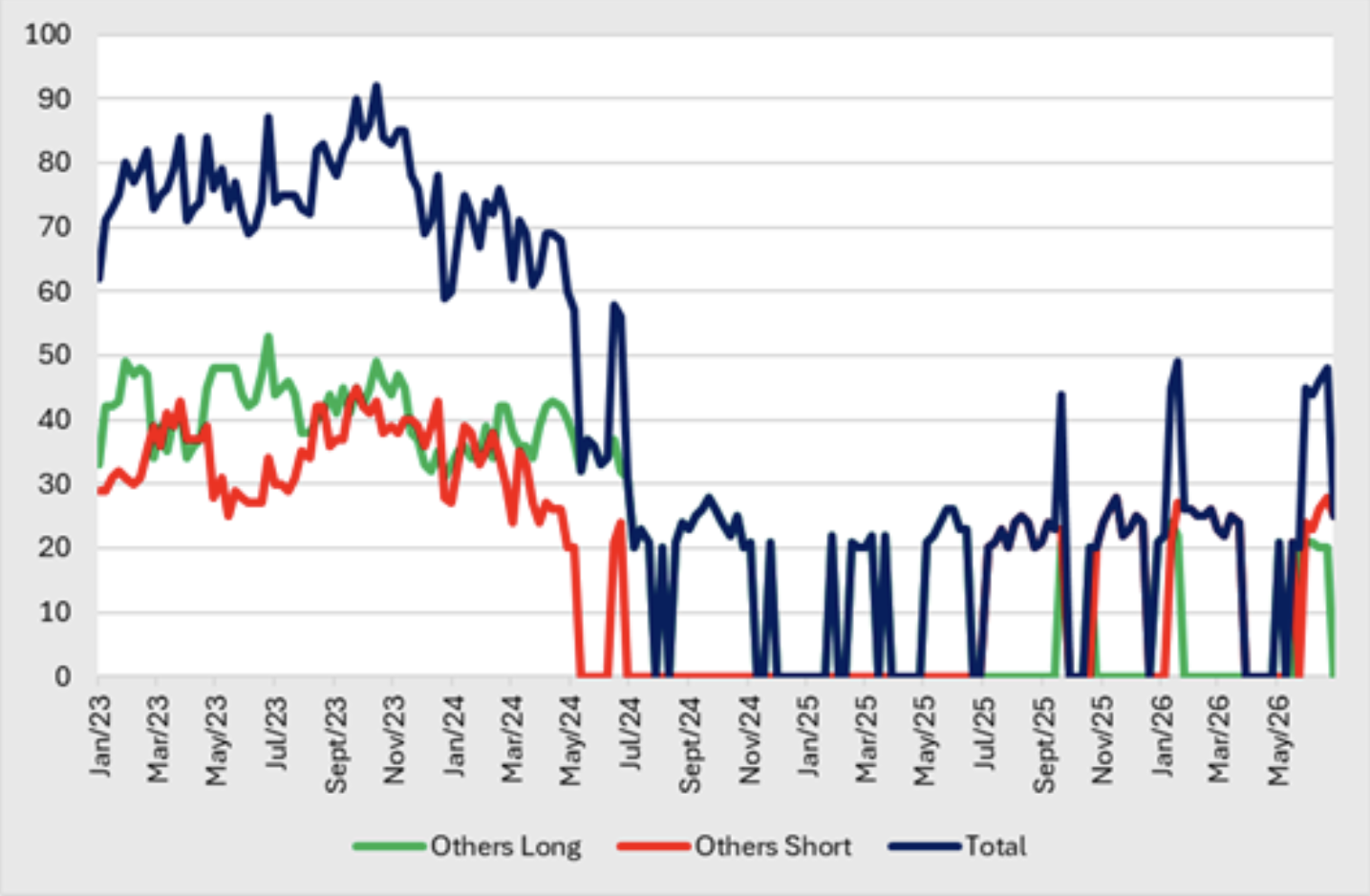

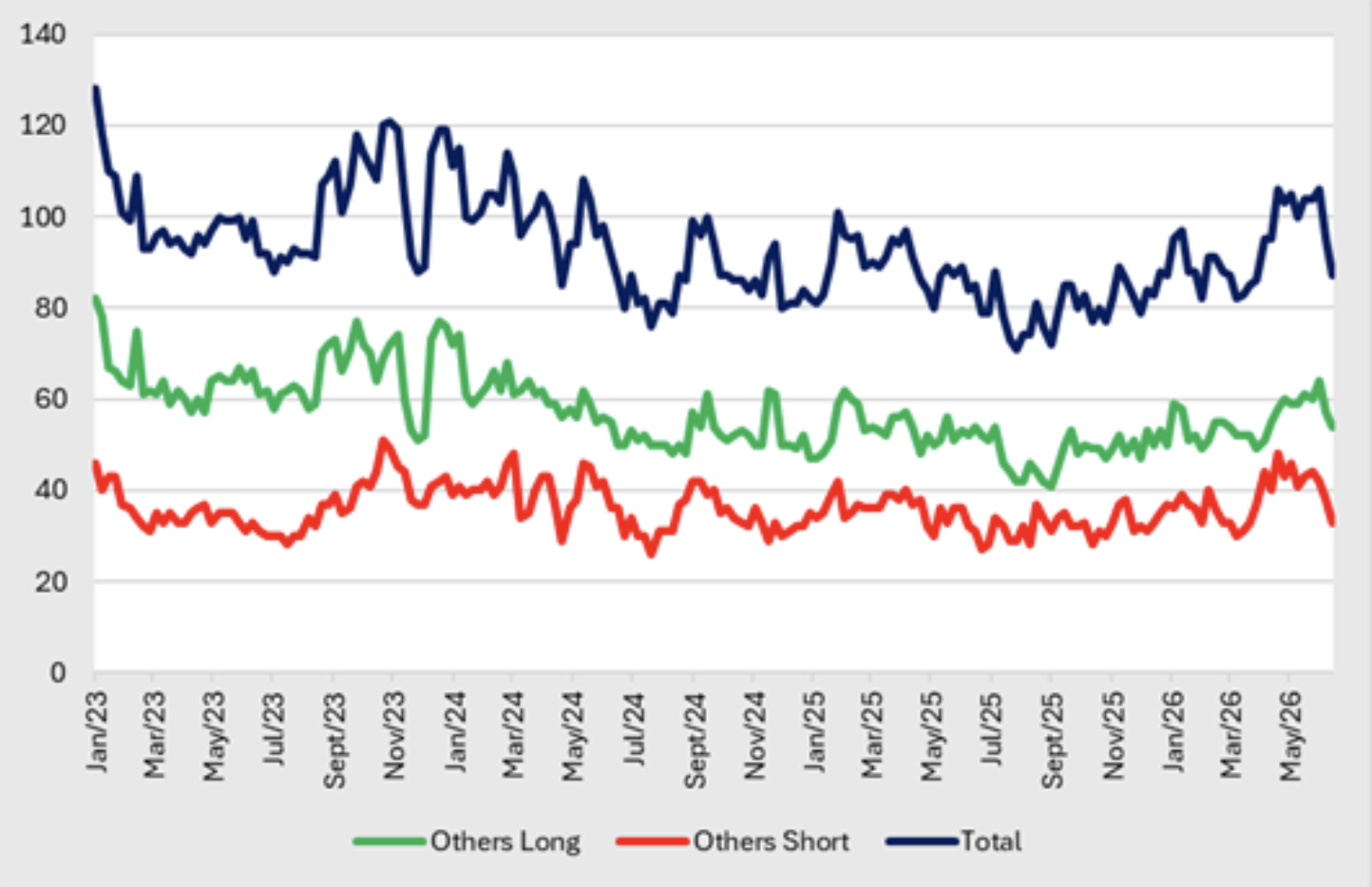

| Others | Every other trader not placed into the other three categories. E.g., Broker Agency, Bank Agency, Inter-Dealer Brokers, etc. |