KEY INSIGHTS #2

H-share listing creates a scarcity premium, but also makes this a high-beta tape trade.

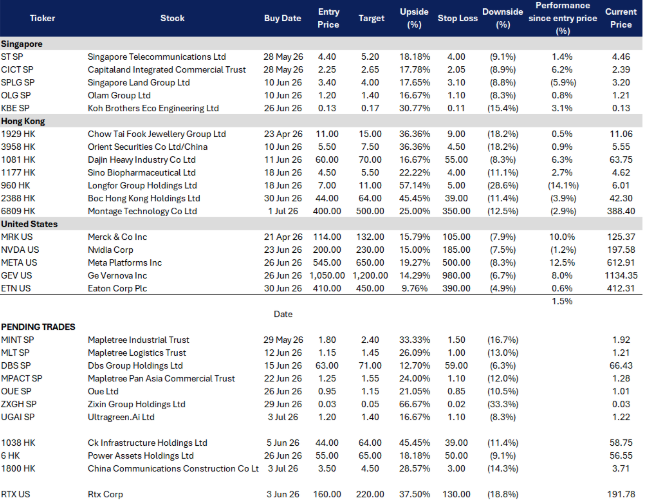

Montage listed in Hong Kong in February 2026, raising about HK$7.04B, with the stock closing 64% above its IPO price on debut. The retail tranche was more than 700x oversubscribed, while the international tranche was more than 37x covered, showing unusually strong institutional and retail appetite for liquid China AI semiconductor exposure. That scarcity premium can persist, but it also means valuation is vulnerable when the AI-chip tape de-rates.