Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

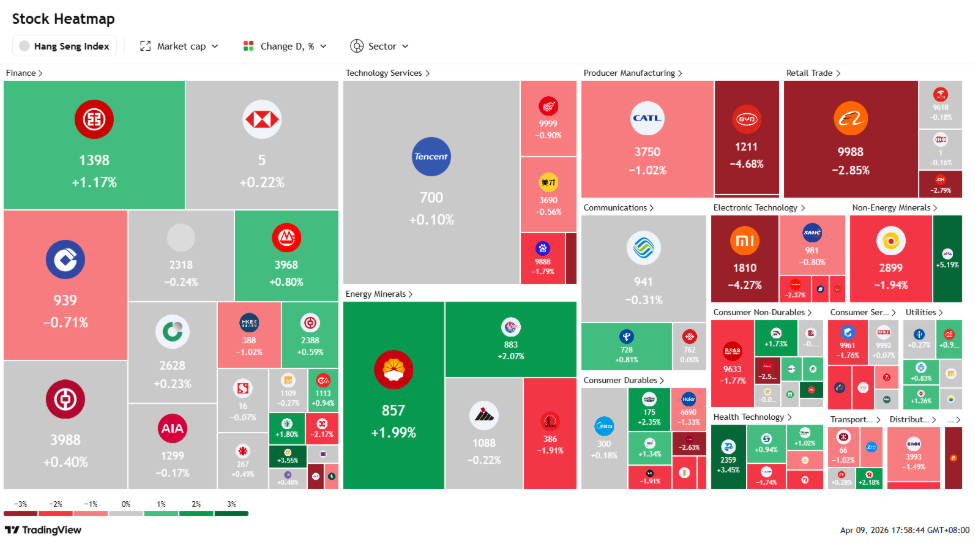

Hong Kong

BUY

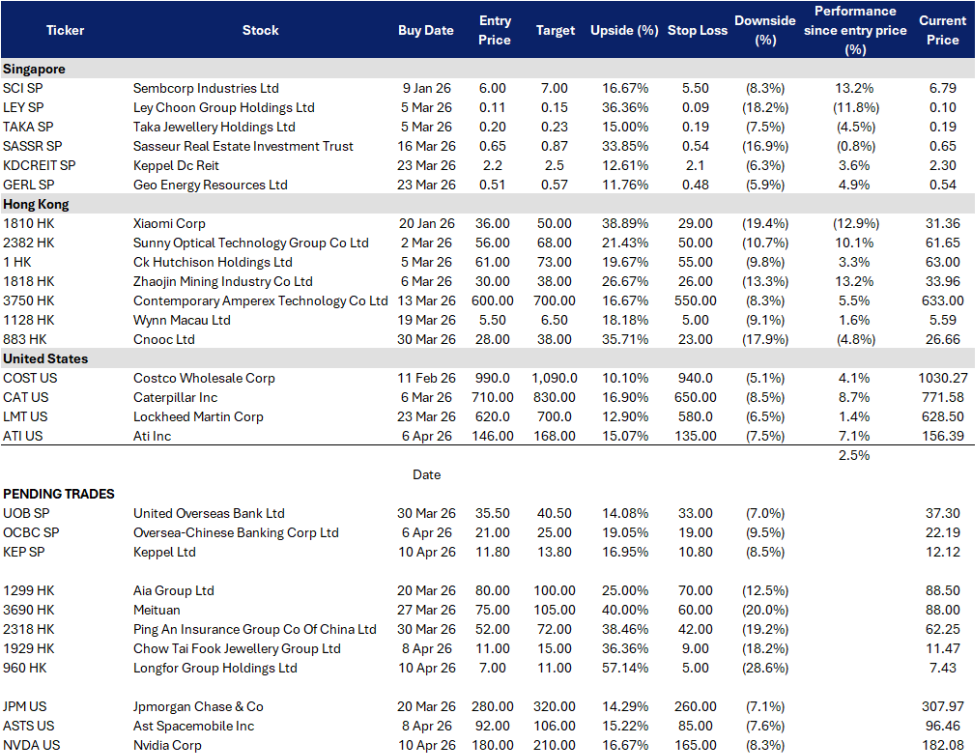

Keppel Ltd (KEP SP)

| Entry: 11.8 Target: 13.8 Stop Loss: 10.8 |

| Capital recycling engine, infrastructure earnings resilience, and buybacks tightening the float |

| Key Insights |

- Infrastructure is behaving like a cash engine, not a cyclical swing factor. Infrastructure segment net profit was S$803M in 2025, up 18% YoY, despite moderating spark spreads, reflecting resilience in integrated power and growing contributions from decarbonisation and sustainability solutions. This keeps earnings quality intact even if real estate or connectivity gains are lumpy.

- Buybacks plus dividends amplify TSR when the tape improves. Keppel launched a S$500M buyback programme in Jul 2025 and repurchased 13.2M shares worth S$116M in 2H25. At the same time, FY2025 dividends comprised an interim S$0.15, a proposed final S$0.19, and a proposed special cash dividend S$0.02, implying total FY2025 dividend of about S$0.47 per share. Buybacks reduce float and improve per-share optics, while the dividend policy and special distribution framework provide carry while waiting for the next monetisation cycle.

RE-ITERATE BUY

OCBC Bank (OCBC SP)

| Entry: 21 Target: 25 Stop Loss: 19 |

| Rate reset plus capital returns, with MAS Jan 29 as the policy anchor |

| Key Insights |

- Capital return is a real rerating lever and management is leaning on it. OCBC proposed ordinary dividend 42 cents and special dividend 16 cents for FY25, taking the total payout to 60% of earnings. Management also reaffirmed the ongoing S$2.5B two-year capital return plan through FY26, using special dividends and share buybacks, with commentary indicating a bias to special dividends when excess capital is available. This framework tightens downside and keeps the equity story simple even if NIM drifts lower.

- Diversified income is offsetting the NII downcycle. IFY25 profit before tax hit a new high of S$9.12B despite net profit being slightly lower year on year, as record total income and noninterest income strength partially offset lower net interest income in a declining rate environment. This matters because the market has historically underwritten OCBC at higher multiples when fees and insurance carry the slope.

BUY

Longfor Group (960 HK)

| Entry: 7 Target: 11 Stop Loss: 5 |

| Quality consolidation winner as policy thaw meets peer distress |

| Key Insights |

- Policy thaw is real, but banks still discriminate. Reuters reporting suggests the three red lines regime has been effectively ended, and policymakers are leaning on mechanisms like the project whitelist with potential multiyear loan extensions for favoured projects. That helps the sector at the margin, but the bigger point is that credit still flows selectively, which again favours higher quality private developers over distressed names.

- Balance sheet optics are investable and management is explicitly prioritising debt safety in 2026. In Longfor’s FY2025 results, net debt to equity was stated at 52.2%, with average finance cost 3.51% and long average debt tenor, which supports a debt safety narrative versus peers. Management commentary around 2026 has been framed around fully repaying related debts and further reducing liabilities, which is the right messaging for a sector still trading on solvency confidence.

RE-ITERATE BUY

Chow Tai Fook Jewellery Group (1929 HK)

| Entry: 11 Target: 15 Stop Loss: 9 |

| Mix upgrade is working, recovery tape is improving, overseas option value is rising |

| Key Insights |

- Mix upgrade is the real margin lever and it is showing up in the numbers. Fixed-price jewellery contribution expanded to 40.1% of retail sales value from 29.4% a year ago. This is the key margin driver because it reduces sensitivity to volatile gold prices and lifts gross profit per transaction. The market typically underwrites this late, meaning the mix shift can still support further multiple expansion if it holds through 1H26.

- Overseas expansion adds a second narrative and improves brand equity ahead of the centenary runway. The group opened a flagship store in Bangkok and communicated plans to open stores in Australia and Canada by end June 2026, with Middle East entry targeted within two years. Even if earnings contribution is initially modest, this builds option value and supports the brand transformation angle that the market is now paying for.

BUY

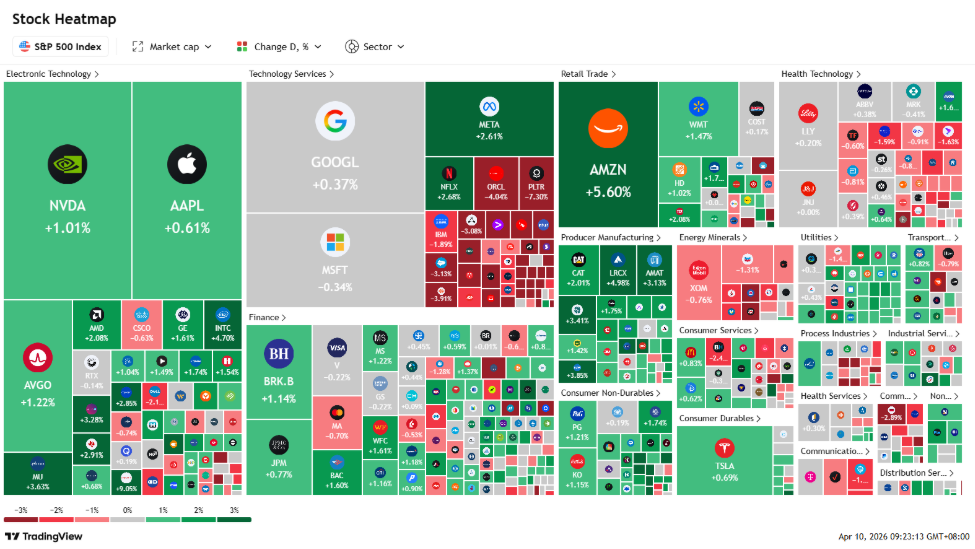

NVIDIA Corp. (NVDA US)

| Entry: 180 Target: 210 Stop Loss: 165 |

| AI compute demand keeps expanding |

| Key Insights |

- Nvidia’s revenue opportunity keeps rising as AI demand shifts from training to inference. Nvidia has raised its AI chip revenue opportunity from US$500bn through 2026 to more than US$1tn through 2027, driven by strong order momentum for Blackwell and Rubin and the growing shift from AI training toward large-scale inference deployment. As hyperscalers and AI developers move from experimentation into real-time production workloads, Nvidia remains the core supplier of the compute, systems and networking stack needed to support that demand.

- Platform leadership makes Nvidia a relative safe haven in AI. Even in a more uncertain macro environment, Nvidia remains relatively defensive within tech because it is no longer just a chip supplier, but the core platform underpinning AI infrastructure across GPUs, CPUs, networking, software, and full-rack systems. That ecosystem depth raises switching costs and makes Nvidia one of the clearest ways for investors to stay exposed to AI spending without taking as much execution risk on downstream names.

RE-ITERATE BUY

AST SpaceMobile Inc. (ASTS US)

| Entry: 92 Target: 106 Stop Loss: 85 |

| From technology validation to commercial constellation buildout |

| Key Insights |

- Commercialization is accelerating as AST moves from proof-of-concept to scaled deployment. AST SpaceMobile is entering its most important transition phase, moving from technology validation into early commercialization, with US$70.9mn of FY25 revenue, over US$1.2bn of contracted revenue commitments, and a launch cadence targeting 45 to 60 satellites in orbit by end-2026. The company’s recent milestones, including successful deployment of BlueBird 6, expected peak speeds above 120 Mbps, and new commercial agreements such as TELUS in Canada, support the case that AST is evolving into a real operating satellite network rather than a pure development story.

- Government and telecom partnerships strengthen funding, demand visibility, and strategic relevance. AST’s partner base now includes major telecom operators such as TELUS, Orange, Telefónica, CK Hutchison, Taiwan Mobile, Sunrise, Vodafone initiatives, and stc, while U.S. government traction is also building through a US$30mn SDA HALO Europa contract and positioning on the Missile Defense Agency’s SHIELD program. Combined with more than US$3.9bn of pro forma liquidity after its February 2026 financing, AST has both the strategic backing and the capital base to bridge toward broader commercial service activation by 2026.

TAKE PROFIT

- Viking Holdings Ltd (VIK US) at US$80

- Citigroup Inc (C US) at US$122

ADD

–

CUT

- Occidental Petroleum Corp (OXY US) at US$57

- Cheniere Energy Inc (LNG US) at US$270