Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

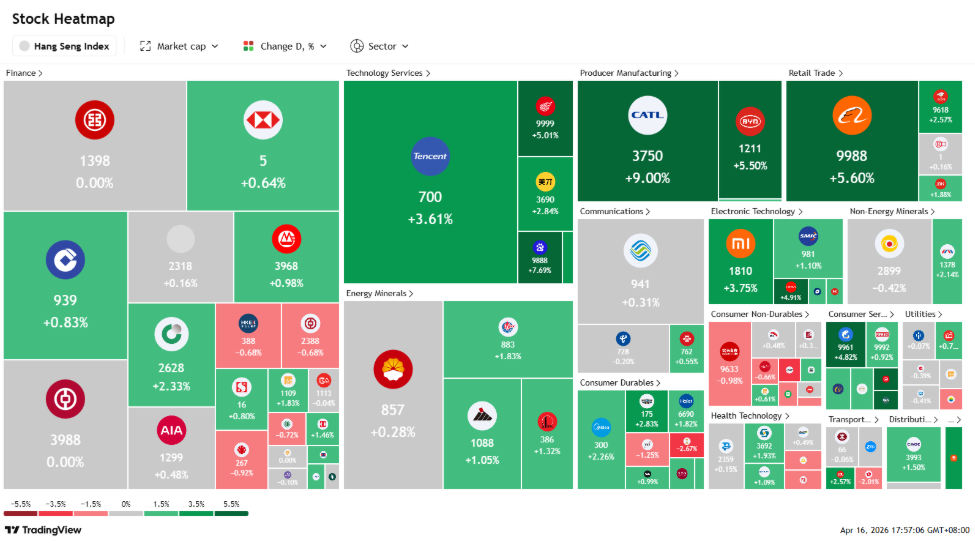

Hong Kong

BUY

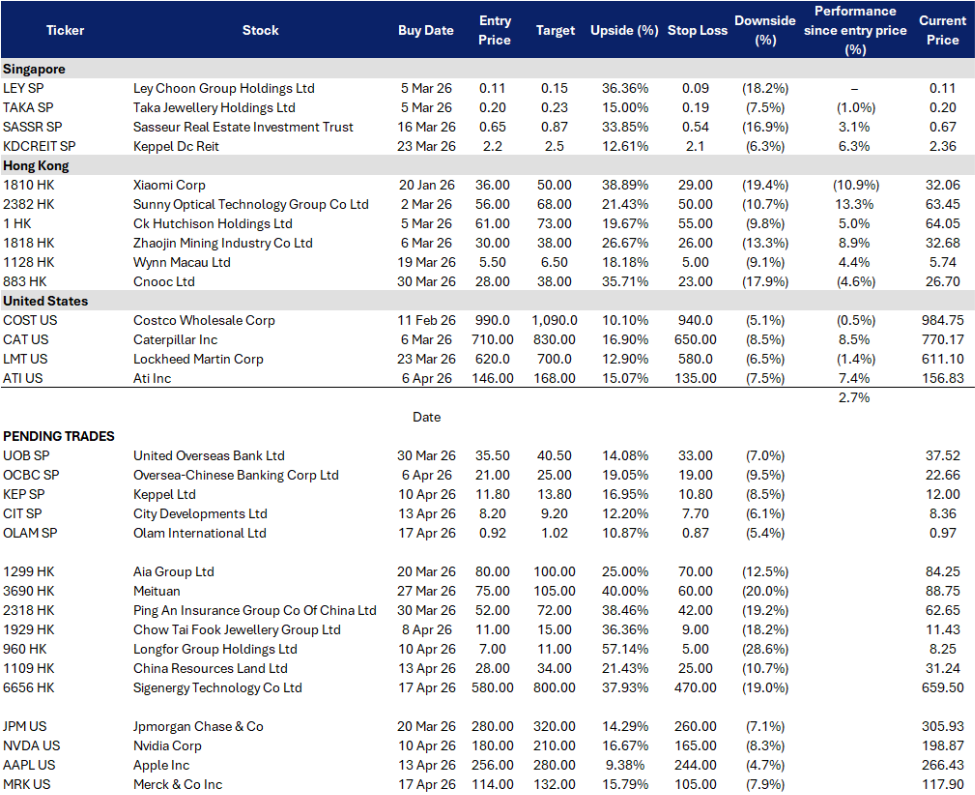

Olam Group Ltd (OLAM SP)

| Entry: 0.92 Target: 1.02 Stop Loss: 0.87 |

| Re-org catalyst tightens holdco discount, buybacks back on, earnings recovery visible |

| Key Insights |

- Re-org is now the primary value driver, not commodity beta. The 2025 results deck reiterates the updated re-organisation plan: clear separation, monetise Remaining Olam Group over time, and progressively return proceeds via special dividends. The biggest mechanical unlock is the planned sale of the 64.57% stake in Olam Agri with gross cash proceeds estimated at US$2.58B (including Tranche 2 call/put mechanics), alongside a stated goal to make Remaining Olam Group debt-free and self-sustaining. This is the cleanest narrative for a near-term re-rating in a market that still prices a holdco discount.

- Earnings recovery reduces the “value trap” perception. For FY2025, Olam reported PATMI S$444.1M (+414%) and operational PATMI S$510.9M (+136.2%). Reported EBIT from continuing operations rose 37.9% to S$1.3B, while ofi delivered steady EBIT of ~S$1.1B. This improves baseline credibility as the group transitions from restructuring narrative to demonstrable cash generation.

RE-ITERATE BUY

City Developments Ltd (CIT SP)

| Entry: 8.2 Target: 9.2 Stop Loss: 7.7 |

| Capital recycling rebound, balance-sheet optionality, and a FY25 earnings reset |

| Key Insights |

- Earnings reset is real and driven by monetisation, not just accounting noise. CDL tripled FY2025 PATMI to S$629.7M from S$201.3M in FY2024, with a very strong 2H25 PATMI of S$538.5M. Revenue rose 9.7% to S$3.6B and property development revenue grew 24.1% on higher Singapore project contributions. This improves near-term earnings credibility and keeps the stock sensitive to any follow-through in Singapore launch monetisation.

- Portfolio actions are becoming repeatable, which is the real rerating mechanism. Management has been explicit about proactive portfolio management and capital recycling, including divestments such as the US$143.5M Silicon Valley multifamily sale by its hotel unit. The market tends to re-rate CDL when monetisation becomes a habit rather than a one-off, especially given the latent value embedded across its global hotel and investment property footprint.

BUY

SIGENERGY (6656 HK)

| Entry: 580 Target: 800 Stop Loss: 470 |

| AI native PV storage disruptor with extreme IPO momentum |

| Key Insights |

- Energy security headlines are re-pricing storage adoption. Today’s debut was a clean read-through on investor appetite for storage. Sigenergy raised about HK$4.4B in its IPO and the stock closed +103.4% versus the offer price, reflecting strong demand for the energy storage theme amid renewed energy security concerns.

- IPO technicals can keep the rerate running, but you must respect volatility. The offer price was HK$324.20 and the first day close was HK$659.50. This kind of first-day move typically attracts follow-through flows, but also raises pullback risk once stabilisation flows fade. The trade is best expressed via disciplined levels rather than chasing highs.

RE-ITERATE BUY

China Resources Land (1109 HK)

| Entry: 28 Target: 34 Stop Loss: 25 |

| Quality SOE consolidator, recurring earnings mix, and dividend carry in a still-fragile sector |

| Key Insights |

- Policy thaw helps, but credit still discriminates, so SOEs keep taking share. China has reportedly ended the “three red lines” framework that constrained developer leverage, which is supportive at the sector level. However, the market is still dealing with weak demand and inventory overhang, and bank/market funding remains selective. That combination typically channels incremental liquidity and project flow to stronger SOEs. This is the clean macro framing for owning CR Land rather than broad property beta.

- Dividend carry remains credible while the sector works through volatility. FY25 final dividend was declared at RMB0.966/share with an unchanged payout ratio of about 37% on reported core profit per DBS. Market data services also show the ex-date and pay-date schedule for the final dividend cycle, reinforcing income visibility. In a choppy China property tape, that carry is a meaningful support while investors wait for policy transmission and sales stabilisation.

BUY

Merck & Co Inc. (MRK US)

| Entry: 114 Target: 132 Stop Loss: 105 |

| Strong near-term Keytruda earnings, with active steps to manage the 2028 patent cliff |

| Key Insights |

- Keytruda continues to anchor earnings, but FY26 marks a transition period. Keytruda remains Merck’s core earnings driver, generating $31.7bn in 2025, or about 48.7% of total revenue, and continues to benefit from new approvals and the newer under-the-skin Keytruda Qlex version ahead of the 2028 patent expiry. However, despite a strong Q4 performance, Merck’s FY26 revenue guidance of $65.5bn-$67.0bn came in below expectations, reflecting a ~$2.5bn headwind from generic competition, Medicare price negotiations, and weaker COVID treatment sales, suggesting the company is entering a near-term transition phase before its next growth drivers scale.

- Active mitigation of patent cliff and tariff risks supports longer-term resilience. Merck is actively working to soften the impact of the 2028 patent cliff through additional patent filings and lifecycle management of Keytruda, while also building alternative growth drivers across its broader portfolio. At the same time, the company is reducing policy and supply chain risk through U.S. localisation, having announced over $70bn of planned U.S. investment in 2025, which could help mitigate exposure to potential 100% tariffs on patented pharmaceutical products, especially for firms committing to domestic production.

RE-ITERATE BUY

Apple Inc. (AAPL US)

| Entry: 256 Target: 280 Stop Loss: 244 |

| Cash flow stability with measured AI exposure |

| Key Insights |

- Apple’s restrained AI spending is an advantage in a risk-off market. In a more volatile macro environment where investors are placing greater value on cash flow certainty, Apple’s relatively disciplined AI infrastructure spending has become a strength rather than a weakness. Unlike peers committing enormous capital to AI buildouts, Apple can advance its AI roadmap more gradually while preserving its free cash flow, margins, and shareholder return capacity, making it attractive to investors who still want equity exposure but with a more defensive profile.

- Strong iPhone demand and services resilience support Apple’s defensive growth profile. Apple’s latest quarter reinforced that defensive profile, with revenue rising 16% to US$143.8bn, EPS of US$2.84, and March-quarter revenue growth guided to 13%-16%, driven by strong iPhone demand, a rebound in China, and accelerating growth in India. With an installed base of 2.5 billion devices, Apple continues to monetize both hardware and high-margin ecosystem services, giving it a more resilient earnings base than most consumer tech names amid broader uncertainty.

TAKE PROFIT

- Sembcorp Industries Ltd (SCI SP) at SG$ 7.00

ADD

–

CUT

- AST Spacemobile Inc (ASTS US) at US$85