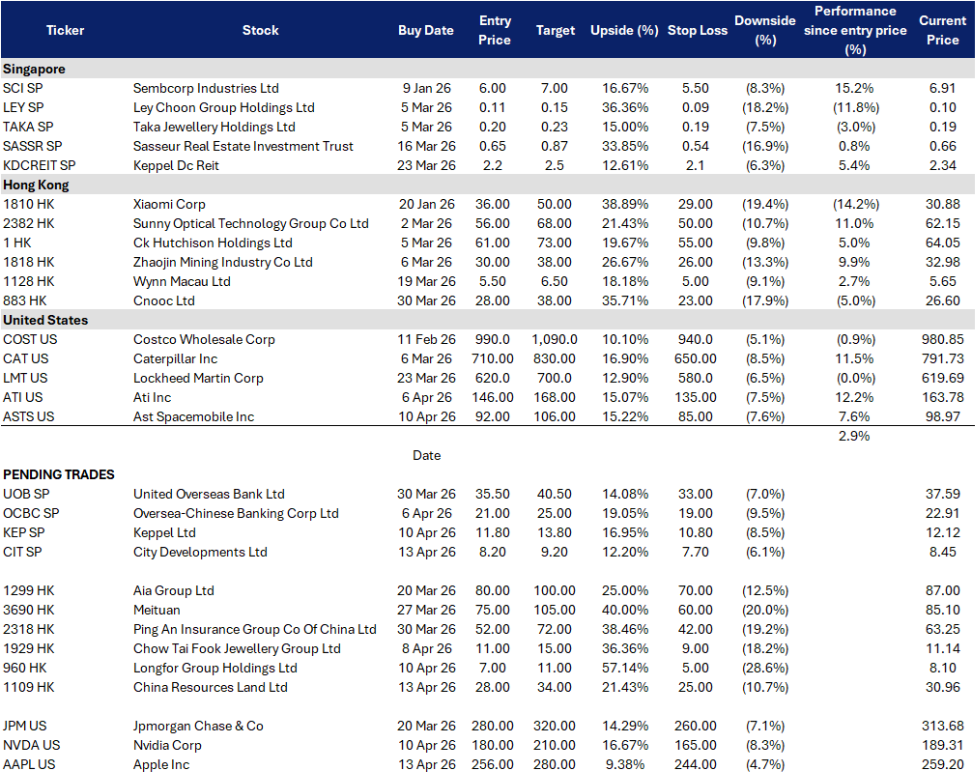

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

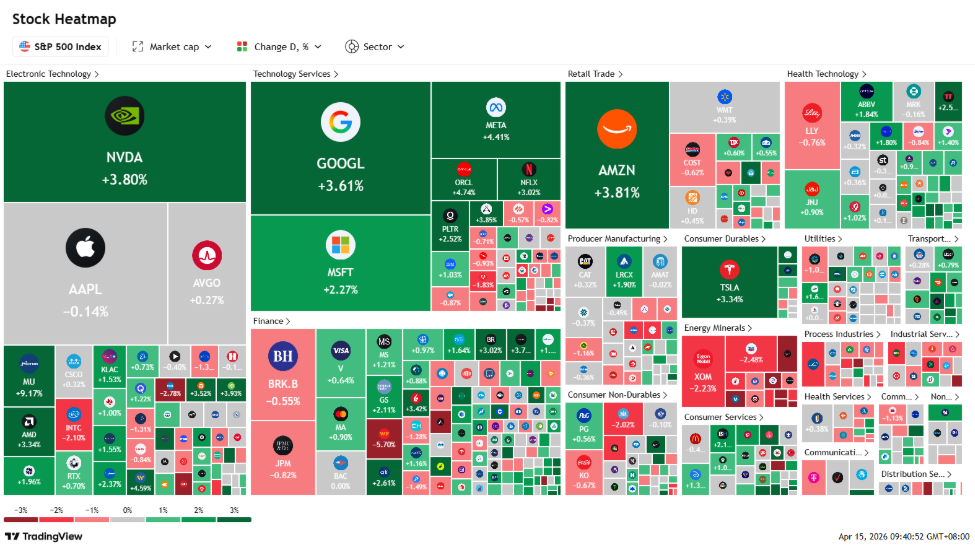

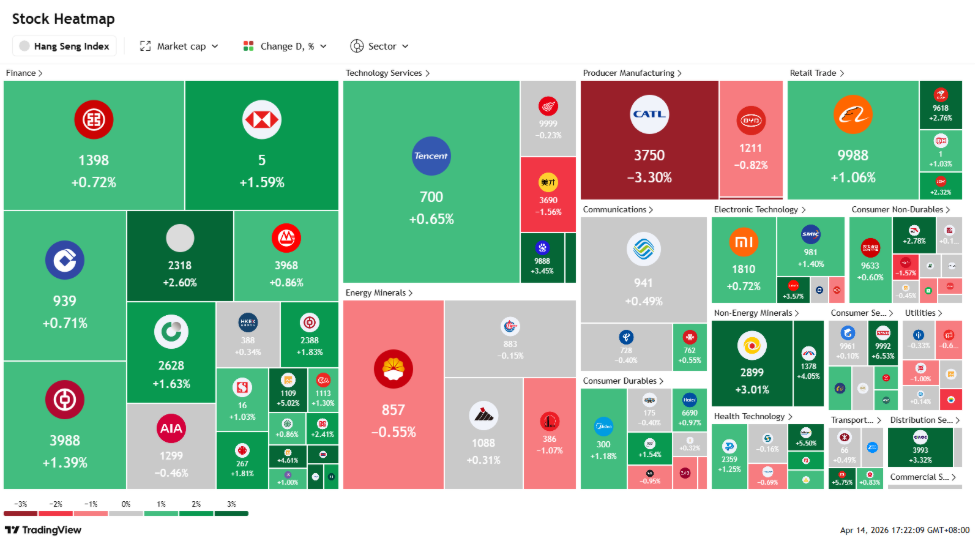

Hong Kong

RE-ITERATE BUY

City Developments Ltd (CIT SP)

| Entry: 8.2 Target: 9.2 Stop Loss: 7.7 |

| Capital recycling rebound, balance-sheet optionality, and a FY25 earnings reset |

| Key Insights |

- Earnings reset is real and driven by monetisation, not just accounting noise. CDL tripled FY2025 PATMI to S$629.7M from S$201.3M in FY2024, with a very strong 2H25 PATMI of S$538.5M. Revenue rose 9.7% to S$3.6B and property development revenue grew 24.1% on higher Singapore project contributions. This improves near-term earnings credibility and keeps the stock sensitive to any follow-through in Singapore launch monetisation.

- Portfolio actions are becoming repeatable, which is the real rerating mechanism. Management has been explicit about proactive portfolio management and capital recycling, including divestments such as the US$143.5M Silicon Valley multifamily sale by its hotel unit. The market tends to re-rate CDL when monetisation becomes a habit rather than a one-off, especially given the latent value embedded across its global hotel and investment property footprint.

RE-ITERATE BUY

Keppel Ltd (KEP SP)

| Entry: 11.8 Target: 13.8 Stop Loss: 10.8 |

| Capital recycling engine, infrastructure earnings resilience, and buybacks tightening the float |

| Key Insights |

- Infrastructure is behaving like a cash engine, not a cyclical swing factor. Infrastructure segment net profit was S$803M in 2025, up 18% YoY, despite moderating spark spreads, reflecting resilience in integrated power and growing contributions from decarbonisation and sustainability solutions. This keeps earnings quality intact even if real estate or connectivity gains are lumpy.

- Buybacks plus dividends amplify TSR when the tape improves. Keppel launched a S$500M buyback programme in Jul 2025 and repurchased 13.2M shares worth S$116M in 2H25. At the same time, FY2025 dividends comprised an interim S$0.15, a proposed final S$0.19, and a proposed special cash dividend S$0.02, implying total FY2025 dividend of about S$0.47 per share. Buybacks reduce float and improve per-share optics, while the dividend policy and special distribution framework provide carry while waiting for the next monetisation cycle.

RE-ITERATE BUY

China Resources Land (1109 HK)

| Entry: 28 Target: 34 Stop Loss: 25 |

| Quality SOE consolidator, recurring earnings mix, and dividend carry in a still-fragile sector |

| Key Insights |

- Policy thaw helps, but credit still discriminates, so SOEs keep taking share. China has reportedly ended the “three red lines” framework that constrained developer leverage, which is supportive at the sector level. However, the market is still dealing with weak demand and inventory overhang, and bank/market funding remains selective. That combination typically channels incremental liquidity and project flow to stronger SOEs. This is the clean macro framing for owning CR Land rather than broad property beta.

- Dividend carry remains credible while the sector works through volatility. FY25 final dividend was declared at RMB0.966/share with an unchanged payout ratio of about 37% on reported core profit per DBS. Market data services also show the ex-date and pay-date schedule for the final dividend cycle, reinforcing income visibility. In a choppy China property tape, that carry is a meaningful support while investors wait for policy transmission and sales stabilisation.

RE-ITERATE BUY

Longfor Group (960 HK)

| Entry: 7 Target: 11 Stop Loss: 5 |

| Quality consolidation winner as policy thaw meets peer distress |

| Key Insights |

- Policy thaw is real, but banks still discriminate. Reuters reporting suggests the three red lines regime has been effectively ended, and policymakers are leaning on mechanisms like the project whitelist with potential multiyear loan extensions for favoured projects. That helps the sector at the margin, but the bigger point is that credit still flows selectively, which again favours higher quality private developers over distressed names.

- Balance sheet optics are investable and management is explicitly prioritising debt safety in 2026. In Longfor’s FY2025 results, net debt to equity was stated at 52.2%, with average finance cost 3.51% and long average debt tenor, which supports a debt safety narrative versus peers. Management commentary around 2026 has been framed around fully repaying related debts and further reducing liabilities, which is the right messaging for a sector still trading on solvency confidence.

RE-ITERATE BUY

Apple Inc. (AAPL US)

| Entry: 256 Target: 280 Stop Loss: 244 |

| Cash flow stability with measured AI exposure |

| Key Insights |

- Apple’s restrained AI spending is an advantage in a risk-off market. In a more volatile macro environment where investors are placing greater value on cash flow certainty, Apple’s relatively disciplined AI infrastructure spending has become a strength rather than a weakness. Unlike peers committing enormous capital to AI buildouts, Apple can advance its AI roadmap more gradually while preserving its free cash flow, margins, and shareholder return capacity, making it attractive to investors who still want equity exposure but with a more defensive profile.

- Strong iPhone demand and services resilience support Apple’s defensive growth profile. Apple’s latest quarter reinforced that defensive profile, with revenue rising 16% to US$143.8bn, EPS of US$2.84, and March-quarter revenue growth guided to 13%-16%, driven by strong iPhone demand, a rebound in China, and accelerating growth in India. With an installed base of 2.5 billion devices, Apple continues to monetize both hardware and high-margin ecosystem services, giving it a more resilient earnings base than most consumer tech names amid broader uncertainty.

RE-ITERATE BUY

NVIDIA Corp. (NVDA US)

| Entry: 180 Target: 210 Stop Loss: 165 |

| AI compute demand keeps expanding |

| Key Insights |

- Nvidia’s revenue opportunity keeps rising as AI demand shifts from training to inference. Nvidia has raised its AI chip revenue opportunity from US$500bn through 2026 to more than US$1tn through 2027, driven by strong order momentum for Blackwell and Rubin and the growing shift from AI training toward large-scale inference deployment. As hyperscalers and AI developers move from experimentation into real-time production workloads, Nvidia remains the core supplier of the compute, systems and networking stack needed to support that demand.

- Platform leadership makes Nvidia a relative safe haven in AI. Even in a more uncertain macro environment, Nvidia remains relatively defensive within tech because it is no longer just a chip supplier, but the core platform underpinning AI infrastructure across GPUs, CPUs, networking, software, and full-rack systems. That ecosystem depth raises switching costs and makes Nvidia one of the clearest ways for investors to stay exposed to AI spending without taking as much execution risk on downstream names.

TAKE PROFIT

- Geo Energy Resources Ltd (GERL SP) at SG$0.57

- Contemporary Amperex Technology Co Ltd (3750 HK) at HK$700

ADD

–

CUT

–