Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

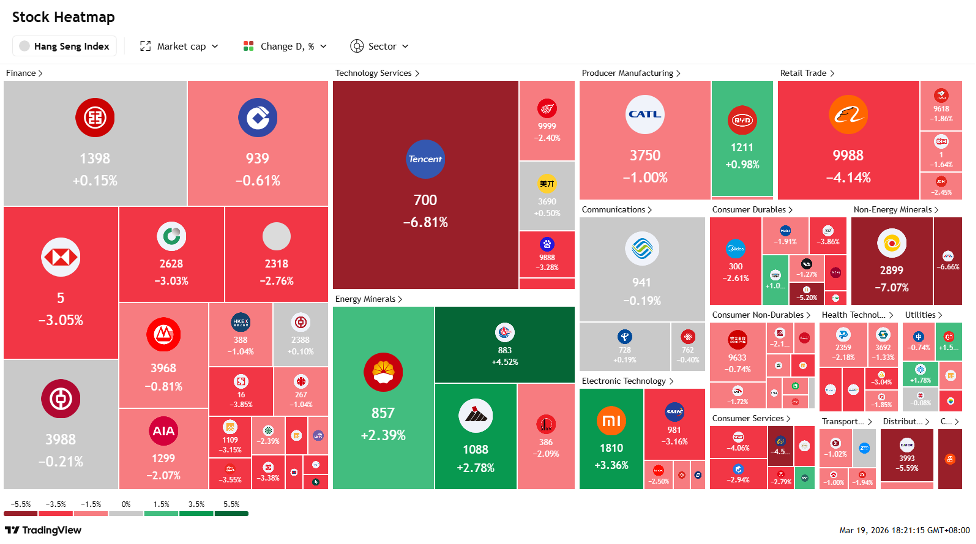

Hong Kong

BUY

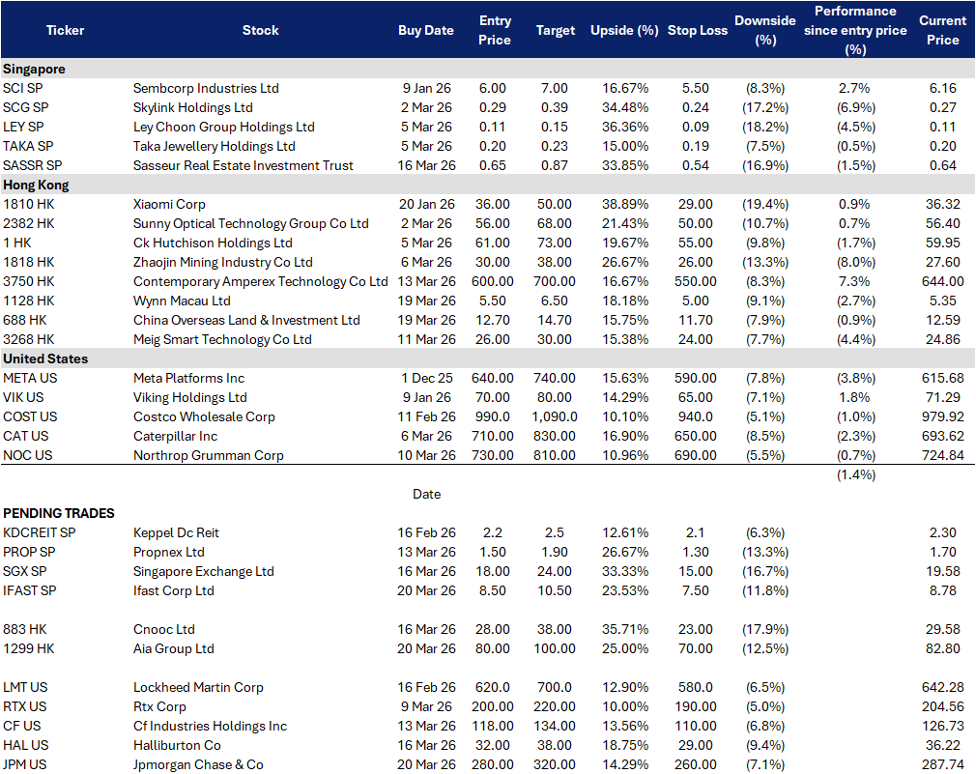

iFAST Corporation Ltd (IFAST SP)

| Entry: 8.5 Target: 10.5 Stop Loss: 7.5 |

| Recurring AUA compounder, bank turns profitable, and platform scale is back |

| Key Insights |

- Recurring fee tailwind is back as AUA and flows reaccelerate. The core setup is a higher quality risk asset tape plus platform share gains. Management highlighted FY2025 profitability was driven by continued growth in the core wealth management platform and the Hong Kong ePension business, which is consistent with a recurring revenue model that scales with AUA and customer activity.

- Bank inflection is the rerating lever, not just an incremental business line. iFAST Global Bank delivered its first full year of profitability in FY2025 with profit before tax of S$3.11M, after a FY2024 loss. This matters because the market has historically discounted the group on the view that banking would be a drag. A credible profitability run rate can compress the conglomerate discount and improve valuation support through cycles.

RE-ITERATE BUY

Singapore Exchange Ltd (SGX SP)

| Entry: 18 Target: 24 Stop Loss: 15 |

| Regulated risk hedging playbook, new product cadence, dividend compounding |

| Key Insights |

- Volatility monetisation, Asia is paying up for hedging tools. SGX is leaning into higher volatility regimes with new risk-management products. Reuters reports SGX plans to introduce Asian government bond futures in the coming weeks, framed explicitly as a response to geopolitical-driven bond volatility and hedging demand. This fits SGX’s multi-asset strategy: when rates, FX, or commodities swing, clearing and derivatives activity typically re-rates faster than cash equities.

- Regulated crypto derivatives optionality without retail conduct risk. SGX launched Bitcoin and Ether perpetual futures on 24 Nov 2025, and access is restricted to accredited, expert, and institutional investors. In practice, BTC up plus vol up tends to pull forward hedging, basis trading, and flows into perpetuals. A regulated venue with clearing infrastructure can capture incremental volumes and clearing economics without needing to chase retail. This is not the core earnings driver today, but it is a credible narrative lever in risk-on tapes.

BUY

AIA Group Ltd (1299 HK)

| Entry: 80 Target: 100 Stop Loss: 70 |

| Pan-Asia life and health insurer with leading franchises across Hong Kong, China, Thailand, Singapore and other Asian markets |

| Key Insights |

- Asia protection cycle is re-rating again, and AIA is printing record new business. AIA delivered record 2025 VONB of US$5.516B (+15%) with operating ROEV 15.8% and EV equity US$79.7B, up 14% per share on an actual exchange rate basis. The macro set-up remains supportive: protection and health remain under-penetrated across Asia, while rates and risk appetite are stabilising, which tends to sustain savings and protection demand in AIA’s core markets.

- Capital return is a credible re-rating tool, not just a yield story. Alongside the record VONB print, AIA announced a US$1.7B share buyback and raised the final dividend to 144.08 HK cents (up from 130.98 HK cents previously). This matters because AIA’s valuation tends to respond when management pairs growth with visible capital return, tightening the floor for the equity even if China macro stays choppy.

RE-ITERATE BUY

CNOOC Ltd (883 HK)

| Entry: 28 Target: 38 Stop Loss: 23 |

| Oil shock beta with production growth, project cadence, and dividend carry |

| Key Insights |

- Oil volatility has repriced, and upstream cashflows re-rate first. Oil is back in a volatility regime. Reuters reports Brent is already around US$100/bbl with recent spikes driven by Middle East supply disruptions and Strait of Hormuz stress, and Goldman lifted near-term averages and tail-risk scenarios. The IEA’s March 2026 oil report also flagged major supply disruption impacts and marked down 2026 demand growth to +640 kb/d YoY, while highlighting the sensitivity to conflict duration and macro. In this tape, low-cost upstream names with visible production growth tend to re-rate quickly on cashflow and dividends.

- Project cadence and reserve replacement are the differentiated edge. CNOOC has kept a steady drumbeat of new discoveries and start-ups. It announced a hundred-million-tonne-class discovery at Qinhuangdao 29-6 in Bohai, described as the 7th consecutive such discovery in Bohai since 2019. It also continues to bring projects onstream, including a South China Sea offshore project commencing production per Reuters (Dec 2025). This underwrites volume growth and helps keep unit costs competitive, improving dividend visibility through the cycle.

BUY

JPMorgan Chase & Co (JPM US)

| Entry: 280 Target: 320 Stop Loss: 260 |

| Stable rates support NIM resilience |

| Key Insights |

- Stable Fed rates should keep NIM firm. The Fed kept rates at 3.50%-3.75% on March 18 and still signalled only one cut this year, while raising its 2026 PCE inflation forecast to 2.7% and maintaining a cautious stance because of the Iran war and oil-price uncertainty. That matters for JPM because a slower easing path reduces the risk of another leg down in margins; management already expects 2026 NII excluding Markets of about US$95bn, and Q4 NII rose 7% to US$25.1bn, suggesting NIM should remain relatively stable.

- Payments and market-share gains add growth even without falling rates. JPM is not relying only on rate cuts, its trading franchise remained strong and it continues to deepen fee-based growth through payments and commercial cards, including the new virtual card launch in Europe with Mastercard. That gives JPM another lever for earnings growth if rates stay higher for longer, while its scale across cards, treasury services, prime brokerage and investment banking helps defend returns even in a flatter-rate environment.

RE-ITERATE BUY

Halliburton (HAL US)

| Entry: 32 Target: 38 Stop Loss: 29 |

| International margin resilience vs North America price pressure, with FCF and buybacks doing the work |

| Key Insights |

- Global upstream spend is holding up better than the US tape. The current OFS setup is bifurcated. North America activity is more sensitive to completion intensity and service pricing, while International spend is steadier on multi-year development cycles. Halliburton’s Q4 commentary and segment margins reinforced that the Eastern Hemisphere remains the stabiliser as North America faces tighter pricing and cadence.

- Any marginal improvement in North America pricing drops fast to earnings. The bear narrative is that US pressure pumping stays competitive and caps margins. The bull trade is that even a modest inflection in pricing or completion intensity improves blended margins quickly given HAL’s operating leverage. This is the swing factor that can turn the stock from “cash-yield carry” into “cycle re-rate.”

TAKE PROFIT

- China Nuclear Energy Technology Corp Ltd (611 HK) at HK$0.50

ADD

- Wynn Macau Ltd (1128 HK) at HK$5.50

- China Overseas Land & Investment Ltd (688 HK) at HK$12.70

- Meig Smart Technology Co Ltd (3268 HK) at HK$26.0

CUT

- Galaxy Entertainment Group Ltd (27 HK) at HK$36