Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

RE-ITERATE BUY

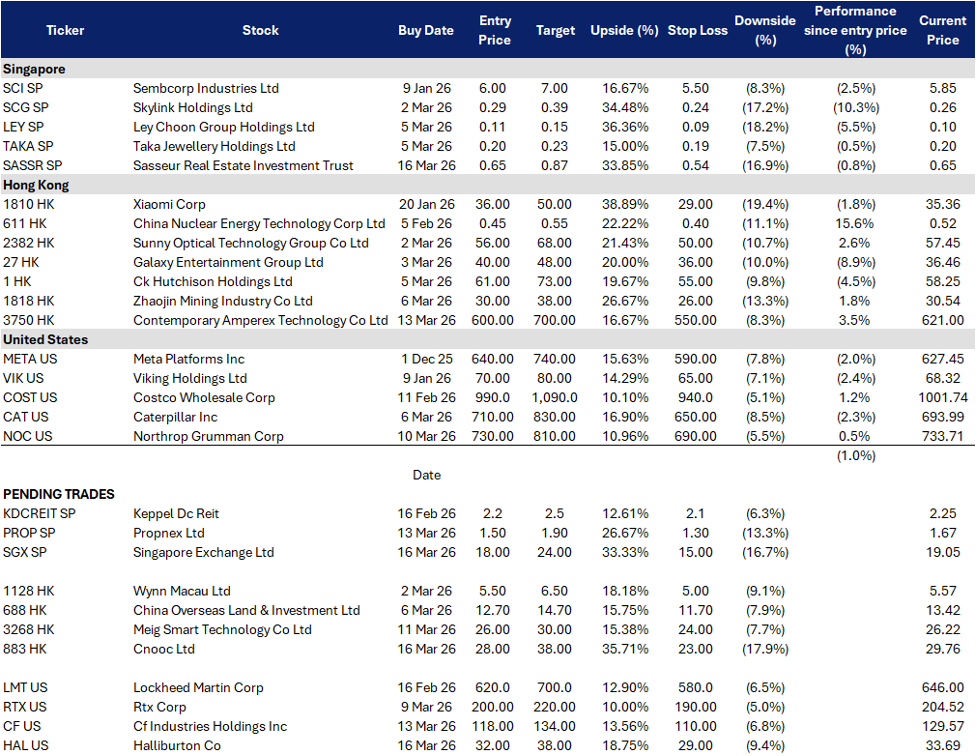

Singapore Exchange Ltd (SGX SP)

| Entry: 18 Target: 24 Stop Loss: 15 |

| Regulated risk hedging playbook, new product cadence, dividend compounding |

| Key Insights |

- Volatility monetisation, Asia is paying up for hedging tools. SGX is leaning into higher volatility regimes with new risk-management products. Reuters reports SGX plans to introduce Asian government bond futures in the coming weeks, framed explicitly as a response to geopolitical-driven bond volatility and hedging demand. This fits SGX’s multi-asset strategy: when rates, FX, or commodities swing, clearing and derivatives activity typically re-rates faster than cash equities.

- Regulated crypto derivatives optionality without retail conduct risk. SGX launched Bitcoin and Ether perpetual futures on 24 Nov 2025, and access is restricted to accredited, expert, and institutional investors. In practice, BTC up plus vol up tends to pull forward hedging, basis trading, and flows into perpetuals. A regulated venue with clearing infrastructure can capture incremental volumes and clearing economics without needing to chase retail. This is not the core earnings driver today, but it is a credible narrative lever in risk-on tapes.

RE-ITERATE BUY

PropNex Ltd (PROP SP)

| Entry: 1.5 Target: 1.9 Stop Loss: 1.3 |

| New-launch wave and a “goldilocks” resale market keep earnings elevated into FY26 |

| Key Insights |

- New-launch supply is back, which is the highest margin revenue pool. PropNex framed Singapore residential as entering a “goldilocks” phase in 2025, driven by a strong pick-up in private residential launches and sales. FY2025 revenue hit S$1.12B (+42.6% YoY) and PATMI S$70.4M (+72% YoY), which is consistent with a new-launch-driven cycle rather than a one-off. Management said it expects a good FY2026 on the back of revenue recognition from strong new project sales and a healthy launch pipeline.

- Dividend is the valuation anchor and it is now at peak payout. PropNex proposed a final dividend of 4.5 cents, taking FY2025 DPS to 9.5 cents and a 99.9% payout ratio, with a stated yield of about 5.1% at the reference price in its release. This creates a clear total-return floor while the market waits for 1H26 launch conversions. The trade-off is that payout is already near the ceiling, so re-rating needs either sustained earnings or another volume leg up.

RE-ITERATE BUY

CNOOC Ltd (883 HK)

| Entry: 28 Target: 38 Stop Loss: 23 |

| Oil shock beta with production growth, project cadence, and dividend carry |

| Key Insights |

- Oil volatility has repriced, and upstream cashflows re-rate first. Oil is back in a volatility regime. Reuters reports Brent is already around US$100/bbl with recent spikes driven by Middle East supply disruptions and Strait of Hormuz stress, and Goldman lifted near-term averages and tail-risk scenarios. The IEA’s March 2026 oil report also flagged major supply disruption impacts and marked down 2026 demand growth to +640 kb/d YoY, while highlighting the sensitivity to conflict duration and macro. In this tape, low-cost upstream names with visible production growth tend to re-rate quickly on cashflow and dividends.

- Project cadence and reserve replacement are the differentiated edge. CNOOC has kept a steady drumbeat of new discoveries and start-ups. It announced a hundred-million-tonne-class discovery at Qinhuangdao 29-6 in Bohai, described as the 7th consecutive such discovery in Bohai since 2019. It also continues to bring projects onstream, including a South China Sea offshore project commencing production per Reuters (Dec 2025). This underwrites volume growth and helps keep unit costs competitive, improving dividend visibility through the cycle.

RE-ITERATE BUY

MeiG Smart Technology Co., Ltd. (3268 HK)

| Entry: 26 Target: 30 Stop Loss: 24 |

| High-compute smart modules ride on-device AI and 5G-A upgrade |

| Key Insights |

- “AI at the edge” narrative can re-rate quickly. The company sits directly in the on-device AI narrative (AI shifting from cloud to edge devices), a theme that has been attracting fast re-pricing in HK tech listings when demand is strong and float is tight.

- Competitive positioning is unusually clean in a crowded IoT stack. Prospectus disclosures highlight leadership in high-compute smart modules (48–64 TOPS portfolio) and first-mover claims in running text-to-image models on such modules. It also claims a leading position in 5G in-vehicle module shipments with 35.1% global share in 2024. This is the differentiated moat versus commoditised data-transmission modules.

RE-ITERATE BUY

Halliburton (HAL US)

| Entry: 32 Target: 38 Stop Loss: 29 |

| International margin resilience vs North America price pressure, with FCF and buybacks doing the work |

| Key Insights |

- Global upstream spend is holding up better than the US tape. The current OFS setup is bifurcated. North America activity is more sensitive to completion intensity and service pricing, while International spend is steadier on multi-year development cycles. Halliburton’s Q4 commentary and segment margins reinforced that the Eastern Hemisphere remains the stabiliser as North America faces tighter pricing and cadence.

- Any marginal improvement in North America pricing drops fast to earnings. The bear narrative is that US pressure pumping stays competitive and caps margins. The bull trade is that even a modest inflection in pricing or completion intensity improves blended margins quickly given HAL’s operating leverage. This is the swing factor that can turn the stock from “cash-yield carry” into “cycle re-rate.”

RE-ITERATE BUY

CF Industries Holdings Inc. (CF US)

| Entry: 118 Target: 134 Stop Loss: 110 |

| Fertilizer supply disruptions driving pricing power |

| Key Insights |

- Fertilizer supply disruptions drive nitrogen pricing power. Escalating geopolitical tensions in the Middle East are tightening global fertilizer supply chains as disruptions through the Strait of Hormuz, responsible for roughly one-third of global fertilizer trade, threaten shipments of key nutrients such as urea and nitrogen. As farmers enter the critical planting season, supply shortages have already driven urea fertilizer prices up roughly 30% within a week, tightening global availability and raising agricultural input costs. As one of the largest nitrogen fertilizer producers in North America, CF Industries is well positioned to benefit from higher global fertilizer prices and increased demand as farmers prioritize maintaining crop yields despite rising input costs.

- Low-carbon fertilizer and industrial partnerships support long-term growth. Beyond cyclical fertilizer pricing, CF Industries is expanding into low-carbon fertilizer production through partnerships with companies such as POET and agricultural cooperatives, developing cleaner ammonia and nitrogen solutions that reduce carbon intensity in ethanol and agricultural supply chains. As agriculture and energy industries increasingly focus on decarbonization and sustainable fuel production, CF’s leadership in ammonia production and carbon capture integration positions the company to benefit from long-term structural demand for low-carbon fertilizers and industrial decarbonization solutions.

TAKE PROFIT

–

ADD

- Sasseur REIT (SASSR SP) at S$0.65

CUT

–