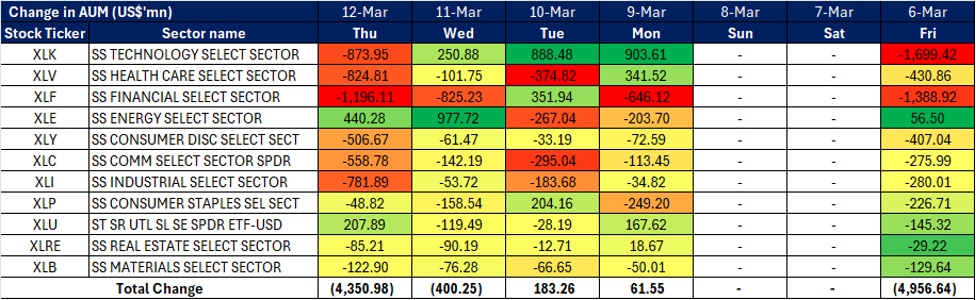

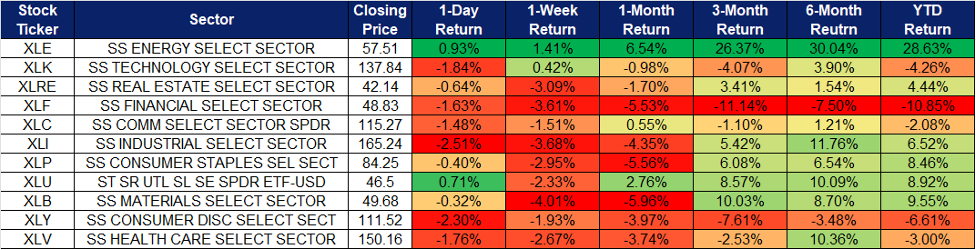

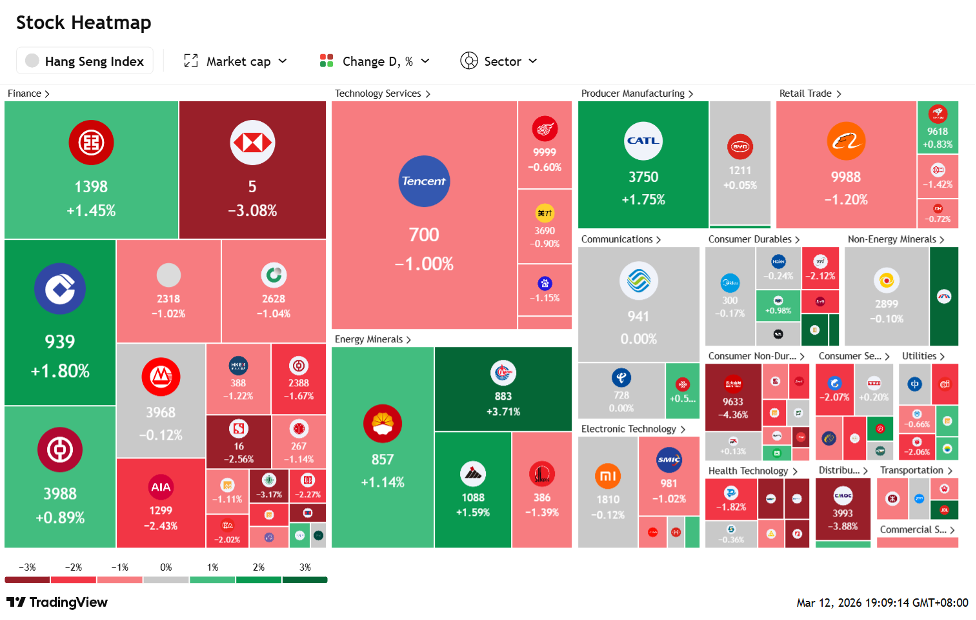

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

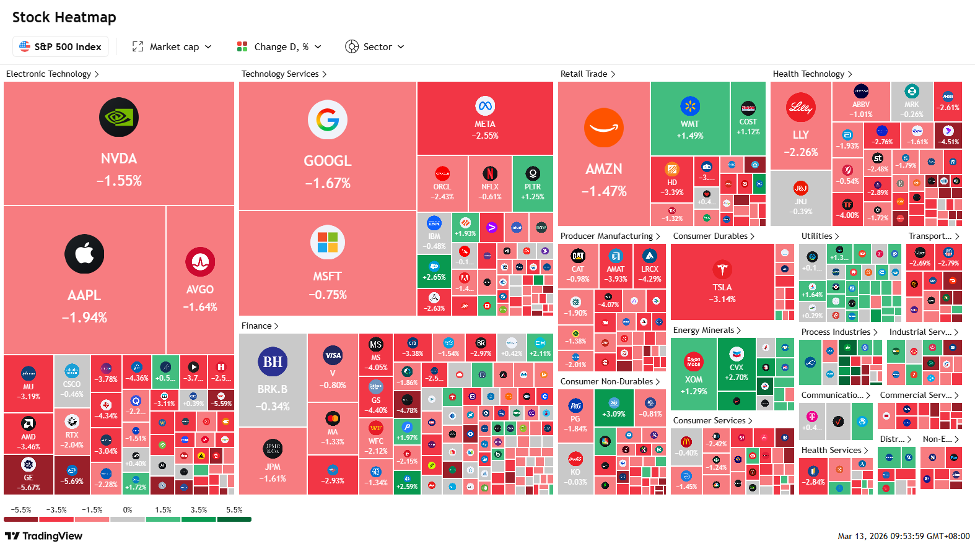

United States

Hong Kong

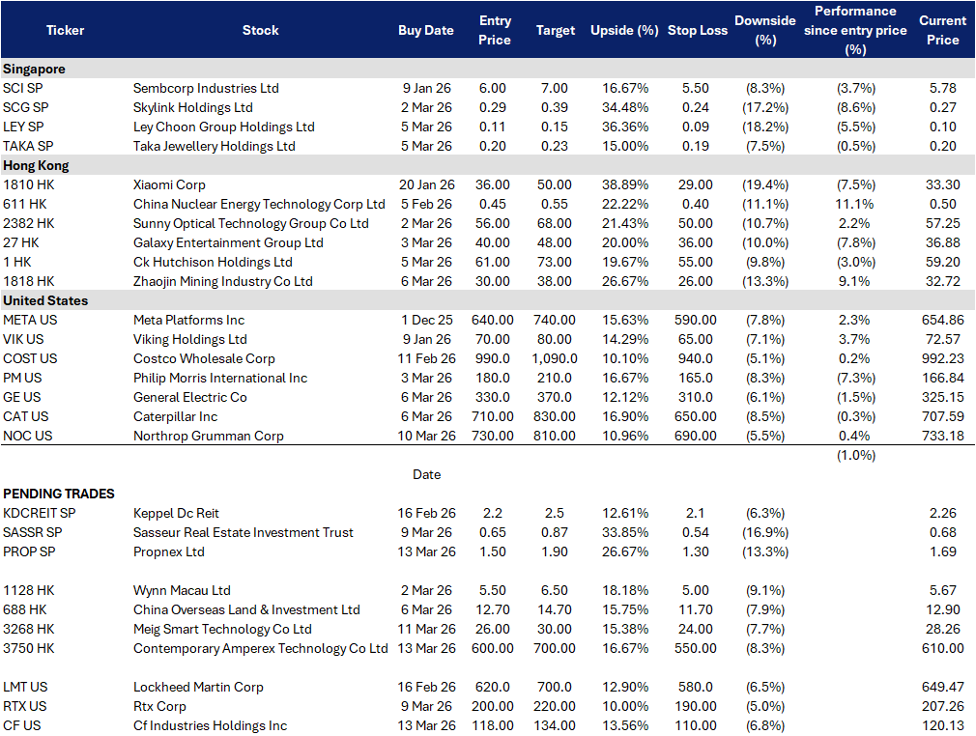

BUY

PropNex Ltd (PROP SP)

RE-ITERATE BUY

Sasseur REIT (SASSR SP)

| Entry: 1.5 Target: 1.9 Stop Loss: 1.3 |

| New-launch wave and a “goldilocks” resale market keep earnings elevated into FY26 |

| Key Insights |

- New-launch supply is back, which is the highest margin revenue pool. PropNex framed Singapore residential as entering a “goldilocks” phase in 2025, driven by a strong pick-up in private residential launches and sales. FY2025 revenue hit S$1.12B (+42.6% YoY) and PATMI S$70.4M (+72% YoY), which is consistent with a new-launch-driven cycle rather than a one-off. Management said it expects a good FY2026 on the back of revenue recognition from strong new project sales and a healthy launch pipeline.

- Dividend is the valuation anchor and it is now at peak payout. PropNex proposed a final dividend of 4.5 cents, taking FY2025 DPS to 9.5 cents and a 99.9% payout ratio, with a stated yield of about 5.1% at the reference price in its release. This creates a clear total-return floor while the market waits for 1H26 launch conversions. The trade-off is that payout is already near the ceiling, so re-rating needs either sustained earnings or another volume leg up.

| Entry: 0.65 Target: 0.87 Stop Loss: 0.54 |

| Defensive outlet cashflows, capital discipline, and a lower cost of debt |

| Key Insights |

- China consumption beta with downside cushion. Outlet retail has held up better than broader discretionary in a choppy China consumer tape. Sasseur’s EMA structure captures variable upside when tenant sales improve but retains a fixed base that stabilises distributions. The FY2025 print reinforces that stability with DPU still edging higher despite FX headwinds.

- Cost of debt is easing, which supports carry into FY2026. Finance costs have become less of a headwind as refinancing initiatives take effect. The 3Q25 update flagged a weighted average cost of debt around 4.6% and management expected it to fall below 4.5% by 4Q25, supporting distributable income even if RMB stays soft.

- KGI have also assumed coverage on Sasseur REIT which can be found here.

BUY

CATL (3750 HK)

RE-ITERATE BUY

MeiG Smart Technology Co., Ltd. (3268 HK)

| Entry: 600 Target: 700 Stop Loss: 550 |

| World’s largest EV battery maker and a leading energy storage battery supplier, spanning power batteries, ESS, and related services. |

| Key Insights |

- Energy storage is now the incremental growth engine. CATL’s energy storage battery shipments rose 80% YoY in 2025 and contributed 14.7% of revenue, with the company maintaining around 30% global share in energy storage. This mix shift matters because ESS demand is less dependent on China passenger EV price wars and tends to carry longer project pipelines.

- Sodium ion and swap. CATL has been pushing sodium ion toward commercialisation, including claims around mass production for commercial vehicles, and management has positioned 2026 as a year of broader sodium battery adoption across swapping, passenger vehicles, commercial vehicles and energy storage. This is a genuine optionality lever because sodium can improve cost and supply chain resilience for certain use cases versus lithium, especially when lithium input volatility returns.

| Entry: 26 Target: 30 Stop Loss: 24 |

| High-compute smart modules ride on-device AI and 5G-A upgrade |

| Key Insights |

- “AI at the edge” narrative can re-rate quickly. The company sits directly in the on-device AI narrative (AI shifting from cloud to edge devices), a theme that has been attracting fast re-pricing in HK tech listings when demand is strong and float is tight.

- Competitive positioning is unusually clean in a crowded IoT stack. Prospectus disclosures highlight leadership in high-compute smart modules (48–64 TOPS portfolio) and first-mover claims in running text-to-image models on such modules. It also claims a leading position in 5G in-vehicle module shipments with 35.1% global share in 2024. This is the differentiated moat versus commoditised data-transmission modules.

BUY

CF Industries Holdings Inc. (CF US)

RE-ITERATE BUY

RTX Corp. (RTX US)

| Entry: 118 Target: 134 Stop Loss: 110 |

| Fertilizer supply disruptions driving pricing power |

| Key Insights |

- Fertilizer supply disruptions drive nitrogen pricing power. Escalating geopolitical tensions in the Middle East are tightening global fertilizer supply chains as disruptions through the Strait of Hormuz, responsible for roughly one-third of global fertilizer trade, threaten shipments of key nutrients such as urea and nitrogen. As farmers enter the critical planting season, supply shortages have already driven urea fertilizer prices up roughly 30% within a week, tightening global availability and raising agricultural input costs. As one of the largest nitrogen fertilizer producers in North America, CF Industries is well positioned to benefit from higher global fertilizer prices and increased demand as farmers prioritize maintaining crop yields despite rising input costs.

- Low-carbon fertilizer and industrial partnerships support long-term growth. Beyond cyclical fertilizer pricing, CF Industries is expanding into low-carbon fertilizer production through partnerships with companies such as POET and agricultural cooperatives, developing cleaner ammonia and nitrogen solutions that reduce carbon intensity in ethanol and agricultural supply chains. As agriculture and energy industries increasingly focus on decarbonization and sustainable fuel production, CF’s leadership in ammonia production and carbon capture integration positions the company to benefit from long-term structural demand for low-carbon fertilizers and industrial decarbonization solutions.

| Entry: 200 Target: 220 Stop Loss: 190 |

| Scaling defence production amid global conflict |

| Key Insights |

- Accelerating U.S. weapons production supports missile demand. RTX is positioned to benefit from the U.S. government’s push to accelerate weapons manufacturing as the Trump administration convenes major defence contractors to address munitions shortages following conflicts in Ukraine, Gaza and recent strikes on Iran. With billions of dollars’ worth of missiles, artillery and anti-tank weapons drawn from U.S. inventories, the Pentagon is preparing a supplemental defence budget of roughly US$50bn to replenish stockpiles. As Raytheon is a key supplier of missile and air-defence systems, including Tomahawk cruise missiles, RTX stands to benefit from higher procurement and sustained demand for precision strike capabilities.

- Global air and missile defence demand expands growth runway. Beyond U.S. replenishment programs, rising geopolitical tensions and military modernization across Europe, the Middle East and Asia are driving demand for missile defence systems and integrated air defence networks. A recent US$183.7mn contract with the UAE for the Patriot system underscores RTX’s ability to capture rising international spending as nations move to secure critical infrastructure and military assets.

TAKE PROFIT

- Geo Energy Resources Ltd (GEO SP) at SG$0.49

ADD

- Northrop Grumman Corp (NOC US) at US$730

CUT

–