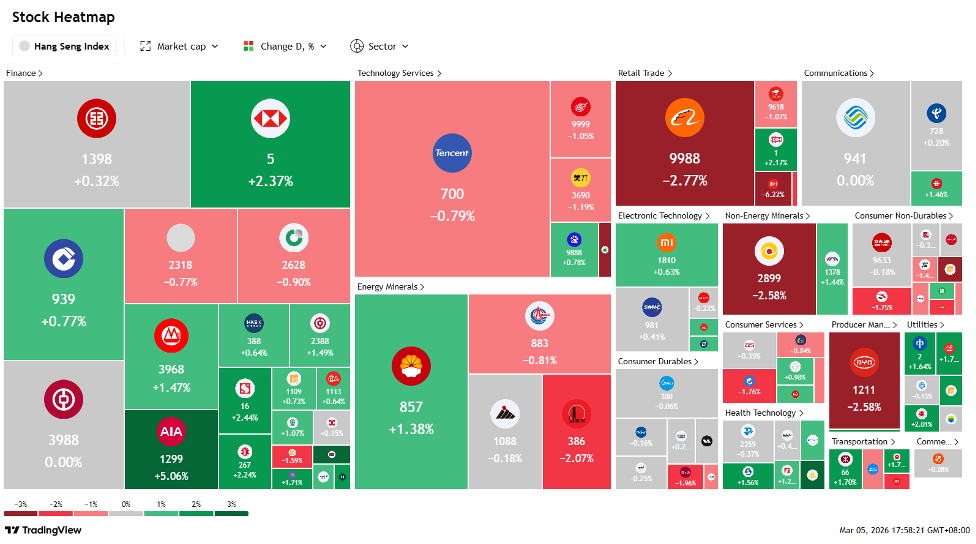

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

RE-ITERATE BUY

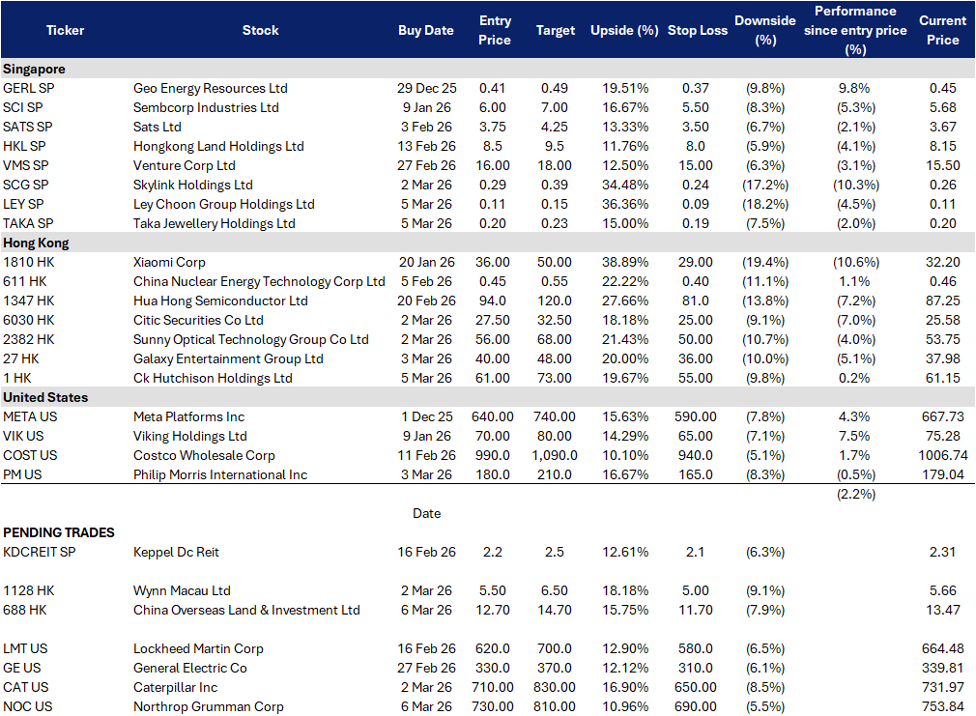

Geo Energy Resources Ltd (GEO SP)

RE-ITERATE BUY

Taka Jewellery Holdings Ltd (TAKA SP)

| Entry: 0.41 Target: 0.49 Stop Loss: 0.37 |

| Coal-price stabilisation, MBJ cost reset, and volume ramp set up 2026 |

| Key Insights |

- Coal prices have stabilised off the trough while Indonesia supply policy tightens the backdrop. Geo’s 3Q25 update flagged ICI4 recovering from the US$40–41/t area in Jul-25 to around the high-US$40s to ~US$50/t into Dec-25, with 2026 expected to be more rangebound rather than collapsing further. The same note also highlighted Indonesia’s planned production curtailment stance from 2026 and a proposed coal export tax, which improves supply discipline and supports low-cost producers. This is the key macro setup for RE4.

- Execution visibility is improving on production, dividends, and FY25 close. Geo’s 3Q25 business update showed 9M25 production at 9.6Mt, tracking ahead of the company’s FY25 target of 10.5–11.5Mt, and the company declared a 0.10 SG cent interim dividend for 3Q25, bringing YTD interim dividends to 0.45 SG cent. SGX also shows the FY25 full-year results were released on 27 Feb 2026, keeping the stock in an event-driven window.

- KGI have also assumed coverage on Geo Energy Group which can be found here.

| Entry: 0.200 Target: 0.230 Stop Loss: 0.185 |

| Riding record gold demand with diversified earnings growth |

| Key Insights |

- Retail expansion and strong gold demand drive top-line growth. Taka Jewellery is benefiting from record gold demand in Singapore and higher gold prices, with 1H26 revenue surging 44.3% YoY to S$119.9mn, driven by stronger retail sales, outlet expansion, and increased trading volumes. As local consumers continue to accumulate gold amid price volatility and geopolitical uncertainty, Taka’s expanding store network and resilient brand positioning support sustained market share gains despite margin pressures from product mix and higher operating costs.

- Financial services and exhibition segments enhance earnings resilience. Beyond retail, Taka’s financial services and wholesale/exhibition segments provide diversified growth, with pawn broking income rising 60.2% YoY and exhibition revenue up 42.0% YoY in 1H26. While rising gold prices have increased working capital needs and short-term borrowings, disciplined cost management and improved operating performance position the group to sustain profitability and cash flow momentum into FY26.

BUY

China Overseas Land & Investment Ltd. (688 HK)

RE-ITERATE BUY

Wynn Macau Ltd. (1128 HK)

| Entry: 12.7 Target: 14.7 Stop Loss: 11.7 |

| SOE safe-haven in China property as Vanke restructuring deepens |

| Key Insights |

- China property stabilisation is turning more forceful, which favours stronger SOEs. China’s property policy tone has become more supportive again, with Reuters reporting authorities have reportedly dropped the “three red lines” borrowing policy that had constrained developers for years. This matters because policy easing typically channels liquidity and buyer confidence first toward stronger, state-backed names. COLI remains one of the clearest liquid beneficiaries of that relative-quality trade in Hong Kong.

- Vanke debt restructuring headlines reinforce consolidation logic and relative rerating for COLI. Vanke has moved deeper into liability management mode, with Reuters reporting creditor-approved repayment deferrals, interest-payment deferrals, and growing market expectations of broader restructuring. This is exactly the kind of sector stress that tends to redirect capital, land opportunities, and buyer trust toward stronger SOEs. For COLI, the thesis is less about direct Vanke exposure and more about relative positioning as one of the few scaled names with funding access and execution capacity during consolidation.

| Entry: 5.5 Target: 6.5 Stop Loss: 5.0 |

| Macau GGR re-accelerates, premium-mass upside remains, but 4Q miss tempers the pace |

| Key Insights |

- Macau momentum is back in the tape, and monthly GGR is the key macro trigger. Macau started 2026 strongly with January GGR at MOP22.633B, up 24% YoY and about 8% MoM, which is an important sentiment catalyst for the whole Macau gaming complex. The market typically re-rates Macau names when monthly GGR prints beat expectations, especially into peak travel windows. This improves the backdrop for Wynn Macau even if company-specific hold rates can remain noisy quarter to quarter.

- Headline beta to Macau recovery remains high, which supports tactical upside. Wynn Macau remains one of the cleaner listed ways to express a Macau recovery trade. As long as monthly GGR stays firm and travel/tourism demand holds, investors tend to re-price operators ahead of full earnings normalisation. The company has also kept a steady disclosure cadence via parent Wynn Resorts’ quarterly releases, which can support near-term catalysts and sentiment.

BUY

Northrop Grumman Corp. (NOC US)

RE-ITERATE BUY

Caterpillar Inc (CAT US)

| Entry: 730 Target: 810 Stop Loss: 690 |

| Benefiting from rising weapon demand |

| Key Insights |

- Defence stockpile replenishment and production push support procurement growth. Northrop Grumman stands to benefit from the Pentagon’s effort to accelerate weapons production as the U.S. works to rebuild military inventories depleted by recent conflicts. The Trump administration’s meeting with major defence contractors to increase manufacturing capacity, combined with a potential US$50bn supplemental defence budget, highlights the urgency to replenish critical defence capabilities. As a key supplier of advanced aerospace, missile defence and command systems, Northrop is well positioned to participate in this production ramp as governments prioritize readiness and strategic deterrence.

- ISR and Command Systems demand strengthens strategic defence position. Rising geopolitical tensions and modern warfare’s increasing reliance on intelligence, surveillance and reconnaissance (ISR) capabilities are supporting long-term demand for Northrop’s advanced defence technologies. The recently secured US$255mn E-130J airborne command and control training system contract with the U.S. Department of War reflect growing investment in integrated battle management, mission readiness and real-time operational intelligence, reinforcing Northrop’s role as a critical provider of defence systems for the U.S. military and allied forces.

| Entry: 710 Target: 830 Stop Loss: 650 |

| Commodity upswing and industrial AI reinforce record backlog visibility |

| Key Insights |

- Record $51.2B backlog and mining capex cycle support revenue durability. Caterpillar ended 4Q25 with a record order backlog of US$51.2bn, following its highest full-year sales and revenues in company history and a single-quarter sales record of US$19.1bn. The ongoing metals and critical minerals upcycle, driven by electrification, infrastructure buildout and energy transition, has led mining customers to expand capital expenditure, directly supporting Caterpillar’s Resource Industries segment. This record backlog provides strong revenue visibility for 2026 and cushions potential macro volatility.

- Transformation into a tech-enabled industrial leader. Caterpillar is accelerating its shift toward digital and autonomous solutions, having invested US$30bn in R&D over the past 20 years, with plans to increase digital and technology investment 2.5x through 2030.Through AI-powered solutions such as Cat AI Assistant, autonomous heavy equipment, expanded collaboration with NVIDIA and the acquisition of mining software firm RPMGlobal, Caterpillar is transforming from a pure equipment manufacturer into a data-driven industrial technology leader, enhancing productivity, margin resilience and long-term competitive differentiation.

TAKE PROFIT

–

ADD

- Ley Choon Group Holdings Ltd (LEY SP) at SG$0.11

- Taka Jewellery Holdings Ltd (TAKA SP) at SG$0.2

- Ck Hutchison Holdings Ltd (1 HK) at HK$61

- Philip Morris International Inc (PM US) at US$180

CUT

- Hesai Group (2525 HK) at HK$195

- Chow Tai Fook Jewellery Group Ltd (1929 HK) at HK$12