Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

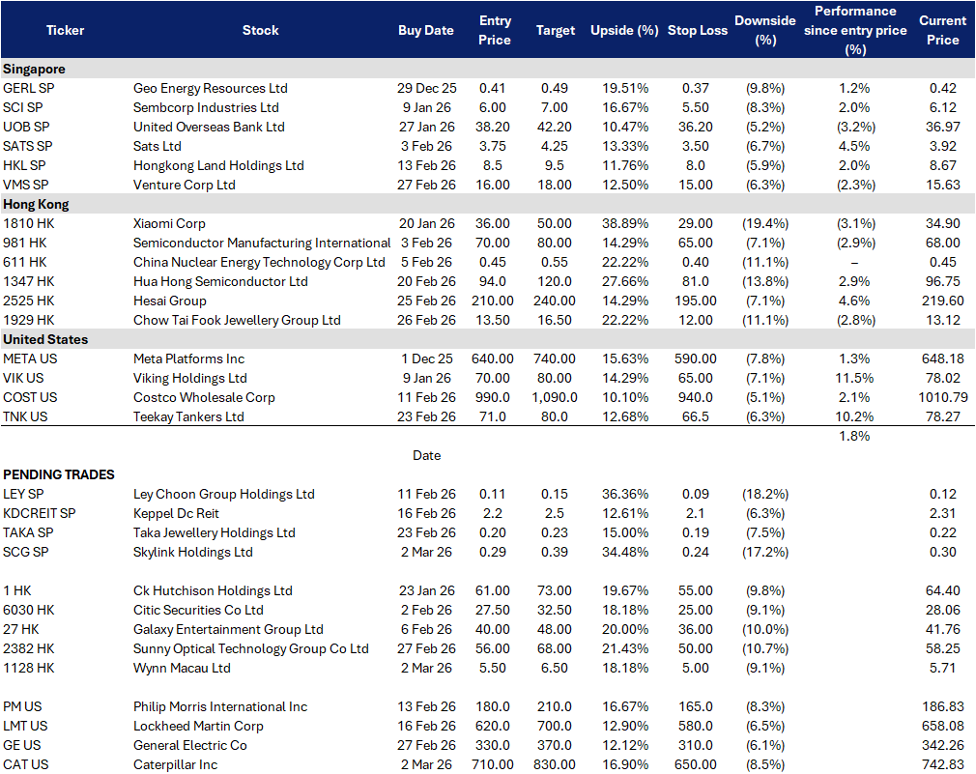

Skylink Holdings Ltd (SCG SP)

RE-ITERATE BUY

Taka Jewellery Holdings Ltd (TAKA SP)

| Entry: 0.29 Target: 0.39 Stop Loss: 0.24 |

| Commercial-vehicle financing flywheel, post-RTO cleanup, and funding catalysts |

| Key Insights |

- SME fleet demand and asset-backed financing remain structurally supported. Skylink sits in a practical, recurring-use segment of Singapore’s economy: commercial vehicles for logistics, construction, and services SMEs. That makes demand more tied to business activity and fleet replacement than discretionary consumer sentiment. The company’s positioning as a one-stop leasing + financing + workshop ecosystem supports retention and cross-sell in a market where uptime matters more than headline pricing.

- Funding and capital-market actions can accelerate growth capacity. Skylink has been active on funding. The 1H26 interim filing shows higher cash balances supported by placement and convertible-bond proceeds, and management highlighted no liquidity covenant breaches. Separately, recent company coverage and financial-highlights pages referenced a proposed placement to raise up to S$7.02M at S$0.27 per share, which is completed, and will support fleet growth and working capital for the financing book.

| Entry: 0.200 Target: 0.230 Stop Loss: 0.185 |

| Riding record gold demand with diversified earnings growth |

| Key Insights |

- Retail expansion and strong gold demand drive top-line growth. Taka Jewellery is benefiting from record gold demand in Singapore and higher gold prices, with 1H26 revenue surging 44.3% YoY to S$119.9mn, driven by stronger retail sales, outlet expansion, and increased trading volumes. As local consumers continue to accumulate gold amid price volatility and geopolitical uncertainty, Taka’s expanding store network and resilient brand positioning support sustained market share gains despite margin pressures from product mix and higher operating costs.

- Financial services and exhibition segments enhance earnings resilience. Beyond retail, Taka’s financial services and wholesale/exhibition segments provide diversified growth, with pawn broking income rising 60.2% YoY and exhibition revenue up 42.0% YoY in 1H26. While rising gold prices have increased working capital needs and short-term borrowings, disciplined cost management and improved operating performance position the group to sustain profitability and cash flow momentum into FY26.

BUY

Wynn Macau, Ltd. (1128 HK)

RE-ITERATE BUY

Sunny Optical Technology (2382 HK)

| Entry: 5.5 Target: 6.5 Stop Loss: 5.0 |

| Macau GGR re-accelerates, premium-mass upside remains, but 4Q miss tempers the pace |

| Key Insights |

- Macau momentum is back in the tape, and monthly GGR is the key macro trigger. Macau started 2026 strongly with January GGR at MOP22.633B, up 24% YoY and about 8% MoM, which is an important sentiment catalyst for the whole Macau gaming complex. The market typically re-rates Macau names when monthly GGR prints beat expectations, especially into peak travel windows. This improves the backdrop for Wynn Macau even if company-specific hold rates can remain noisy quarter to quarter.

- Headline beta to Macau recovery remains high, which supports tactical upside. Wynn Macau remains one of the cleaner listed ways to express a Macau recovery trade. As long as monthly GGR stays firm and travel/tourism demand holds, investors tend to re-price operators ahead of full earnings normalisation. The company has also kept a steady disclosure cadence via parent Wynn Resorts’ quarterly releases, which can support near-term catalysts and sentiment.

| Entry: 56 Target: 68 Stop Loss: 50 |

| Handset optical recovery, auto lens growth, and a profit alert reset |

| Key Insights |

- Optics demand is improving, with auto still a structural leg. Sunny Optical’s December 2025 shipment disclosure still showed vehicle lens sets up 17.7% YoY, even as handset-related categories saw year-end inventory effects. This reinforces the view that automotive optics remains a durable growth pillar while handset demand normalises. The company later announced it will stop publishing monthly shipment updates because they no longer fully reflect operating performance, which suggests investors will increasingly focus on earnings quality and segment mix rather than noisy monthly prints.

- Corporate optionality via proposed spin-off adds a second narrative. Sunny Optical announced a proposed spin-off (inside information disclosure on 5 Jan 2026), which introduces a potential value-unlock angle beyond the cyclical recovery in core optics. Even before details are finalised, spin-off processes often help investors reassess sum-of-parts value and strategic focus, especially when core earnings momentum is improving at the same time.

BUY

Caterpillar Inc (CAT US)

RE-ITERATE BUY

GE Aerospace. (GE US)

| Entry: 710 Target: 830 Stop Loss: 650 |

| Commodity upswing and industrial AI reinforce record backlog visibility |

| Key Insights |

- Record $51.2B backlog and mining capex cycle support revenue durability. Caterpillar ended 4Q25 with a record order backlog of US$51.2bn, following its highest full-year sales and revenues in company history and a single-quarter sales record of US$19.1bn. The ongoing metals and critical minerals upcycle, driven by electrification, infrastructure buildout and energy transition, has led mining customers to expand capital expenditure, directly supporting Caterpillar’s Resource Industries segment. This record backlog provides strong revenue visibility for 2026 and cushions potential macro volatility.

- Transformation into a tech-enabled industrial leader. Caterpillar is accelerating its shift toward digital and autonomous solutions, having invested US$30bn in R&D over the past 20 years, with plans to increase digital and technology investment 2.5x through 2030.Through AI-powered solutions such as Cat AI Assistant, autonomous heavy equipment, expanded collaboration with NVIDIA and the acquisition of mining software firm RPMGlobal, Caterpillar is transforming from a pure equipment manufacturer into a data-driven industrial technology leader, enhancing productivity, margin resilience and long-term competitive differentiation.

| Entry: 330 Target: 370 Stop Loss: 310 |

| Aviation cash engine with expanding defence & AI capabilities |

| Key Insights |

- $190B backlog and narrow-body engine dominance anchor multi-year earnings growth. GE Aerospace enters FY26 with a backlog of approximately US$190bn, following FY25 revenue growth of 21%, EPS growth of 38% and free cash flow conversion exceeding 100%. Its dominant position in the narrow-body engine market (via CFM platforms powering Boeing and Airbus fleets) provides high-margin aftermarket revenue as global flight hours normalize and airlines prioritize fleet renewal. The combination of accelerating equipment deliveries and long-duration service contracts creates durable cash generation and strong earnings visibility into 2026 and beyond.

- U.S. defence contracts and next-gen propulsion expand growth runway. GE is strengthening its defence exposure through digitally enabled sustainment and next-generation propulsion. Its AI-driven TrueChoice Defence contract for the J85 engine integrates data across more than 6,000 engine parts, improving readiness and supply optimization. In addition, GE and Kratos secured a US$12.4mn U.S. Air Force contract to design the GEK1500 engine for Collaborative Combat Aircraft, building on GEK800 testing advancements. As the U.S. prioritizes affordable autonomous combat systems and logistics modernization, GE is positioned to benefit from higher defence spending and digital fleet management demand.

ADD

- Venture Corp Ltd (VMS SP) at SG$16.