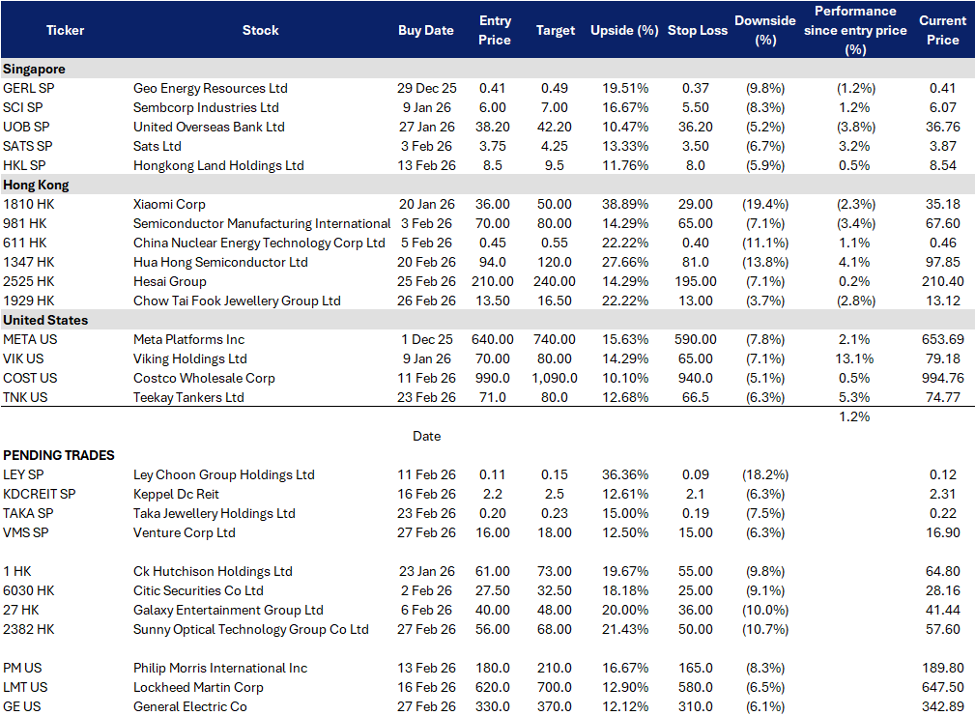

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

Venture Corporation Ltd (VMS SP)

RE-ITERATE BUY

Taka Jewellery Holdings Ltd (TAKA SP)

| Entry: 16.0 Target: 18.0 Stop Loss: 15.0 |

| Electronics recovery broadens, margin discipline holds, cash returns remain the anchor |

| Key Insights |

- Singapore electronics cycle is turning up, which improves the tape for quality EMS names. Singapore’s January 2026 manufacturing output rose 16.6% YoY, with electronics +44% YoY and semiconductors up sharply, extending the recent recovery momentum. This matters for Venture because it improves sentiment and order visibility across electronics supply chains even if its mix is more diversified and higher value than pure-volume EMS peers. Venture’s own 1H25 management commentary also pointed to sequential improvement from 1Q25 to 2Q25 across many technology domains, with Life Science & Medical helping offset weaker consumer-related demand.

- Margin resilience and solution mix remain the key differentiator, not headline topline alone. Street commentary after 3Q25 highlighted that Venture’s net margin stayed stable at around 8.9% despite softer topline conditions in some consumer-linked segments, supported by its focus on differentiated, higher value-added solutions. This is the central investment case versus commoditised EMS names. In other words, Venture does not need a full-blown demand boom to defend earnings quality. As the cycle normalises, operating leverage can improve without sacrificing margin discipline.

| Entry: 0.200 Target: 0.230 Stop Loss: 0.185 |

| Riding record gold demand with diversified earnings growth |

| Key Insights |

- Retail expansion and strong gold demand drive top-line growth. Taka Jewellery is benefiting from record gold demand in Singapore and higher gold prices, with 1H26 revenue surging 44.3% YoY to S$119.9mn, driven by stronger retail sales, outlet expansion, and increased trading volumes. As local consumers continue to accumulate gold amid price volatility and geopolitical uncertainty, Taka’s expanding store network and resilient brand positioning support sustained market share gains despite margin pressures from product mix and higher operating costs.

- Financial services and exhibition segments enhance earnings resilience. Beyond retail, Taka’s financial services and wholesale/exhibition segments provide diversified growth, with pawn broking income rising 60.2% YoY and exhibition revenue up 42.0% YoY in 1H26. While rising gold prices have increased working capital needs and short-term borrowings, disciplined cost management and improved operating performance position the group to sustain profitability and cash flow momentum into FY26.

BUY

Sunny Optical Technology (2382 HK)

RE-ITERATE BUY

Hesai Group (2525 HK)

| Entry: 56 Target: 68 Stop Loss: 50 |

| Handset optical recovery, auto lens growth, and a profit alert reset |

| Key Insights |

- Optics demand is improving, with auto still a structural leg. Sunny Optical’s December 2025 shipment disclosure still showed vehicle lens sets up 17.7% YoY, even as handset-related categories saw year-end inventory effects. This reinforces the view that automotive optics remains a durable growth pillar while handset demand normalises. The company later announced it will stop publishing monthly shipment updates because they no longer fully reflect operating performance, which suggests investors will increasingly focus on earnings quality and segment mix rather than noisy monthly prints.

- Corporate optionality via proposed spin-off adds a second narrative. Sunny Optical announced a proposed spin-off (inside information disclosure on 5 Jan 2026), which introduces a potential value-unlock angle beyond the cyclical recovery in core optics. Even before details are finalised, spin-off processes often help investors reassess sum-of-parts value and strategic focus, especially when core earnings momentum is improving at the same time.

| Entry: 210 Target: 240 Stop Loss: 195 |

| Scaling the “eyes” of autonomous and robotic intelligence |

| Key Insights |

- Automotive scale drives cost leadership. Hesai is leveraging rapid LiDAR adoption in China’s EV and ADAS market to scale production toward 4 million units annually, reinforcing its cost leadership and positioning it to benefit as autonomous driving penetration increases globally. With multiple OEM design wins, multi-million unit orders for its ATX sensor, and expanding robotaxi partnerships, Hesai is emerging as a key supplier in the global race toward higher-level autonomy.

- Robotics expansion unlocks the next growth leg. Beyond automotive, Hesai is capitalizing on rising demand for robotics and embodied AI, highlighted by strong consumer and industry interest following high-profile humanoid robot showcases and growing deployment across logistics and mobility. Its exclusive Southeast Asia partnership with Grab accelerates regional commercialization, positioning Hesai to benefit as LiDAR becomes foundational infrastructure for autonomous machines across industries.

BUY

GE Aerospace. (GE US)

RE-ITERATE BUY

Teekay Tankers Ltd. (TNK US)

| Entry: 330 Target: 370 Stop Loss: 310 |

| Aviation cash engine with expanding defence & AI capabilities |

| Key Insights |

- $190B backlog and narrow-body engine dominance anchor multi-year earnings growth. GE Aerospace enters FY26 with a backlog of approximately US$190bn, following FY25 revenue growth of 21%, EPS growth of 38% and free cash flow conversion exceeding 100%. Its dominant position in the narrow-body engine market (via CFM platforms powering Boeing and Airbus fleets) provides high-margin aftermarket revenue as global flight hours normalize and airlines prioritize fleet renewal. The combination of accelerating equipment deliveries and long-duration service contracts creates durable cash generation and strong earnings visibility into 2026 and beyond.

- U.S. defence contracts and next-gen propulsion expand growth runway. GE is strengthening its defence exposure through digitally enabled sustainment and next-generation propulsion. Its AI-driven TrueChoice Defence contract for the J85 engine integrates data across more than 6,000 engine parts, improving readiness and supply optimization. In addition, GE and Kratos secured a US$12.4mn U.S. Air Force contract to design the GEK1500 engine for Collaborative Combat Aircraft, building on GEK800 testing advancements. As the U.S. prioritizes affordable autonomous combat systems and logistics modernization, GE is positioned to benefit from higher defence spending and digital fleet management demand.

| Entry: 71.0 Target: 80.0 Stop Loss: 66.5 |

| Levered to strong spot rates and geopolitical trade disruptions |

| Key Insights |

- Dirty tanker rates at 3-year highs drive earnings upside. The recent surge in tanker markets, with the Baltic Exchange Dirty Tanker Index hitting a three-year high of 1,743 points, reflects tightening vessel availability and elevated crude flows. Teekay Tankers is directly benefiting from this strength, with its Q4 spot rates averaging US$53,500/day for Suezmax and US$43,600/day for Aframax/LR2 vessels, rising further in 1Q26 to US$56,900/day and US$51,400/day respectively (for ~65% of booked days). With FY25 GAAP net income of US$351.2mn and continued strong spot momentum, Teekay Tankers remains highly levered to sustained rate strength in the mid-size crude segment.

- Geopolitical disruptions and sanctions boost compliant fleet demand. Escalating geopolitical tensions alongside tighter U.S. sanctions and shifting crude trade flows, are increasing tonne-mile demand and diverting cargoes away from the “dark fleet” toward compliant operators like Teekay. With ~20% of global oil supply moving through the Strait of Hormuz and heightened risks of disruption, oil trade inefficiencies are supporting mid-size tanker utilization and pricing. Combined with projected 1.1 mb/d global oil demand growth in 2026 and continued non-OPEC supply expansion, the company is positioned to benefit from structurally firm tanker fundamentals amid elevated geopolitical volatility.

TAKE PROFIT

- Singapore Airlines Ltd (SIA SP) at SG$7.10

- Jl Mag Rare-Earth Co Ltd (6680 HK) at HK$23.92

- ASMPT Ltd (522 HK) at HK$115.5

ADD

- Hesai Group (2525 HK) at HK$210

- Chow Tai Fook Jewellery Group Ltd (1929 HK) at HK$13.5

CUT

- Ondas Inc (ONDS US) at US$9.6

- Jd.Com Inc (9618 HK) at HK$104.8

- Luk Fook Holdings International Ltd (590 HK) at HK$29.38

- Meitu Inc (1357 HK) at HK$5.70