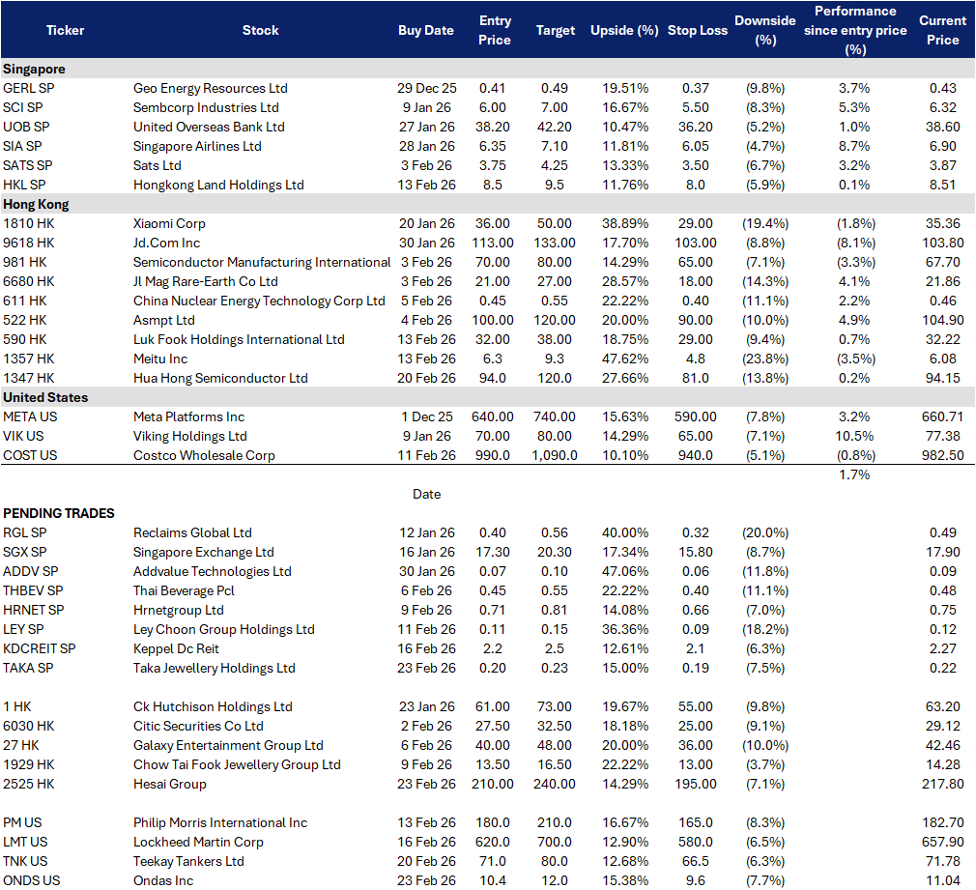

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

Taka Jewellery Holdings Ltd (TAKA SP)

RE-ITERATE BUY

Keppel DC REIT (KDCREIT SP)

| Entry: 0.200 Target: 0.230 Stop Loss: 0.185 |

| Riding record gold demand with diversified earnings growth |

| Key Insights |

- Retail expansion and strong gold demand drive top-line growth. Taka Jewellery is benefiting from record gold demand in Singapore and higher gold prices, with 1H26 revenue surging 44.3% YoY to S$119.9mn, driven by stronger retail sales, outlet expansion, and increased trading volumes. As local consumers continue to accumulate gold amid price volatility and geopolitical uncertainty, Taka’s expanding store network and resilient brand positioning support sustained market share gains despite margin pressures from product mix and higher operating costs.

- Financial services and exhibition segments enhance earnings resilience. Beyond retail, Taka’s financial services and wholesale/exhibition segments provide diversified growth, with pawn broking income rising 60.2% YoY and exhibition revenue up 42.0% YoY in 1H26. While rising gold prices have increased working capital needs and short-term borrowings, disciplined cost management and improved operating performance position the group to sustain profitability and cash flow momentum into FY26.

| Entry: 2.22 Target: 2.50 Stop Loss: 2.08 |

| The AI infrastructure yield compounder |

| Key Insights |

- AI capex cycle keeps the asset class tight, and DC landlords still price power scarcity. Industry data continues to point to a multiyear supply demand gap, increasingly driven by power constraints rather than just real estate availability. A recent JLL cited projection points to global data centre capacity expanding by 97GW from 2026 to 2030, effectively doubling sector capacity, with APAC capacity rising from 32GW to 57GW by 2030.

- Sponsor flywheel plus DPU accretive deployment remains the core rerating engine. The manager is explicitly scaling through hyperscale acquisitions and has guided to meaningful inorganic activity, citing about $1.1B of acquisitions including Tokyo Data Centre 3 and remaining interests in Keppel DC Singapore assets, and noting the remaining interests in Keppel DC Singapore 3 and 4 are expected to complete by 1Q26.

BUY

Hesai Group (2525 HK)

RE-ITERATE BUY

Hua Hong Semiconductor (1347 HK)

| Entry: 210 Target: 240 Stop Loss: 195 |

| Scaling the “eyes” of autonomous and robotic intelligence |

| Key Insights |

- Automotive scale drives cost leadership. Hesai is leveraging rapid LiDAR adoption in China’s EV and ADAS market to scale production toward 4 million units annually, reinforcing its cost leadership and positioning it to benefit as autonomous driving penetration increases globally. With multiple OEM design wins, multi-million unit orders for its ATX sensor, and expanding robotaxi partnerships, Hesai is emerging as a key supplier in the global race toward higher-level autonomy.

- Robotics expansion unlocks the next growth leg. Beyond automotive, Hesai is capitalizing on rising demand for robotics and embodied AI, highlighted by strong consumer and industry interest following high-profile humanoid robot showcases and growing deployment across logistics and mobility. Its exclusive Southeast Asia partnership with Grab accelerates regional commercialization, positioning Hesai to benefit as LiDAR becomes foundational infrastructure for autonomous machines across industries.

| Entry: 94 Target: 120 Stop Loss: 81 |

| Mature node pricing power is back, but guidance sets up a near term shakeout then rerate |

| Key Insights |

- China onshoring plus AI spillover keeps mature node demand tighter than feared. China’s domestic semiconductor supply chain is still in build mode, and demand is being pulled forward by local design houses, while AI driven memory tightness is also creating second order supply constraints elsewhere in the stack. Semiconductor Manufacturing International Corp is expanding capacity to meet strong demand, but flagged margin pressure from higher depreciation, which is a useful read through for the whole China foundry complex.

- ASP and mix are the real margin lever, not just volume. Management explicitly attributed FY25 gross margin expansion to improved ASP plus cost reduction, and highlighted strength in specialty platforms such as standalone NVM and power management. A key macro tailwind is that memory being in high demand can tighten broader foundry capacity allocations, which can improve pricing for mature logic products at the margin.

BUY

Ondas Inc. (ONDS US)

RE-ITERATE BUY

Teekay Tankers Ltd. (TNK US)

| Entry: 10.4 Target: 12.0 Stop Loss: 9.6 |

| Leveraging global security tailwinds |

| Key Insights |

- Counter-UAS solutions capture multi-billion-dollar infrastructure market. Ondas is emerging as a differentiated player in the rapidly expanding counter-UAS market, leveraging its Sentrycs cyber-over-RF technology and Iron Drone Raider™ interceptor system to deliver lawful, non-jamming drone mitigation for sensitive civil environments. Recent deployments with the German State Police and a major NATO-country airport customer validate real-world adoption, while entry into the handheld C-UAS segment (estimated ~US$9.8bn five-year TAM) and expanding European infrastructure protection demand position Ondas to capitalize on rising drone-related security threats across airports, borders, and critical infrastructure.

- Autonomous defence ecosystem positioned for growth. With the global military drone market projected to grow from ~US$15bn in 2024 toward ~US$30-47bn by 2030+, Ondas’ integrated portfolio, aligns with accelerating defence modernization and AI-driven battlefield requirements. As governments increase procurement of autonomous, networked, and resilient systems in contested environments, Ondas’ System-of-Systems approach strengthens its positioning within the broader UAV value chain and enhances long-term revenue visibility from both defence and homeland security programs.

| Entry: 71.0 Target: 80.0 Stop Loss: 66.5 |

| Levered to strong spot rates and geopolitical trade disruptions |

| Key Insights |

- Dirty tanker rates at 3-year highs drive earnings upside. The recent surge in tanker markets, with the Baltic Exchange Dirty Tanker Index hitting a three-year high of 1,743 points, reflects tightening vessel availability and elevated crude flows. Teekay Tankers is directly benefiting from this strength, with its Q4 spot rates averaging US$53,500/day for Suezmax and US$43,600/day for Aframax/LR2 vessels, rising further in 1Q26 to US$56,900/day and US$51,400/day respectively (for ~65% of booked days). With FY25 GAAP net income of US$351.2mn and continued strong spot momentum, Teekay Tankers remains highly levered to sustained rate strength in the mid-size crude segment.

- Geopolitical disruptions and sanctions boost compliant fleet demand. Escalating geopolitical tensions alongside tighter U.S. sanctions and shifting crude trade flows, are increasing tonne-mile demand and diverting cargoes away from the “dark fleet” toward compliant operators like Teekay. With ~20% of global oil supply moving through the Strait of Hormuz and heightened risks of disruption, oil trade inefficiencies are supporting mid-size tanker utilization and pricing. Combined with projected 1.1 mb/d global oil demand growth in 2026 and continued non-OPEC supply expansion, the company is positioned to benefit from structurally firm tanker fundamentals amid elevated geopolitical volatility.

Trading Dashboard Update: No changes to the trading dashboard.