Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

Keppel DC REIT (KDCREIT SP)

RE-ITERATE BUY

Hongkong Land Holdings Limited (HKL SP)

| Entry: 2.22 Target: 2.50 Stop Loss: 2.08 |

| The AI infrastructure yield compounder |

| Key Insights |

- AI capex cycle keeps the asset class tight, and DC landlords still price power scarcity. Industry data continues to point to a multiyear supply demand gap, increasingly driven by power constraints rather than just real estate availability. A recent JLL cited projection points to global data centre capacity expanding by 97GW from 2026 to 2030, effectively doubling sector capacity, with APAC capacity rising from 32GW to 57GW by 2030.

- Sponsor flywheel plus DPU accretive deployment remains the core rerating engine. The manager is explicitly scaling through hyperscale acquisitions and has guided to meaningful inorganic activity, citing about $1.1B of acquisitions including Tokyo Data Centre 3 and remaining interests in Keppel DC Singapore assets, and noting the remaining interests in Keppel DC Singapore 3 and 4 are expected to complete by 1Q26.

| Entry: 8.5 Target: 9.5 Stop Loss: 8.0 |

| Central office stabilisation is real, capital recycling adds a shareholder return bid |

| Key Insights |

- Signs of a Hong Kong office floor are emerging, and the market is still sceptical. Management flagged improving enquiry levels in 1H25, with committed vacancy in the Central office portfolio down to 6.9% at end June and further to 6.4% by end September, meaningfully better than wider Central Grade A vacancy (11.8% in June and 11.0% in September).

- Singapore offices are quietly a stabiliser, while LANDMARK disruption is time bound. Singapore office vacancy is low and rental reversions remained positive, offering earnings ballast while Hong Kong offices work through negative reversions. Management disclosed 2.0% physical vacancy in Singapore at end June with average rents up YoY.

BUY

Hua Hong Semiconductor (1347 HK)

RE-ITERATE BUY

Chow Tai Fook Jewellery Group (1929 HK)

| Entry: 94 Target: 120 Stop Loss: 81 |

| Mature node pricing power is back, but guidance sets up a near term shakeout then rerate |

| Key Insights |

- China onshoring plus AI spillover keeps mature node demand tighter than feared. China’s domestic semiconductor supply chain is still in build mode, and demand is being pulled forward by local design houses, while AI driven memory tightness is also creating second order supply constraints elsewhere in the stack. Semiconductor Manufacturing International Corp is expanding capacity to meet strong demand, but flagged margin pressure from higher depreciation, which is a useful read through for the whole China foundry complex.

- ASP and mix are the real margin lever, not just volume. Management explicitly attributed FY25 gross margin expansion to improved ASP plus cost reduction, and highlighted strength in specialty platforms such as standalone NVM and power management. A key macro tailwind is that memory being in high demand can tighten broader foundry capacity allocations, which can improve pricing for mature logic products at the margin.

| Entry: 13.5 Target: 16.5 Stop Loss: 13 |

| Hard luxury rebound with mix driven margin upside |

| Key Insights |

- Demand Inflection. In the quarter ended 31 Dec 2025, Group retail sales value rose 17.8% YoY, with the Mainland up 16.9% and Hong Kong Macau plus other markets up 22.9%. Same store sales also turned decisively positive, up 21.4% in the Mainland and 14.3% in Hong Kong and Macau. This is a clear signal that discretionary appetite for jewellery is recovering even with a high gold price backdrop, which typically pressures unit volumes but supports ticket size.

- Offshore optionality is emerging as a credible second engine. The flagship store in Bangkok and plans on further store openings in Australia and Canada by end June 2026, with Middle East expansion targeted over the next two years are key progress to watch. This is strategically important because it gives the market a second narrative beyond Mainland store density and domestic consumption, and it can also help brand elevation, a key requirement for sustaining fixed price mix and pricing power.

BUY

Lockheed Martin Corp. (LMT US)

RE-ITERATE BUY

Philip Morris International Inc. (PM US)

| Entry: 620 Target: 700 Stop Loss: 580 |

| Geopolitical tailwinds fuel backlog and defence innovation |

| Key Insights |

- Rising global defence spending underpins long-term demand. Lockheed Martin is benefiting from elevated geopolitical tensions, including pressure for increased Taiwan defence spending, renewed focus on Middle East security, and broader great-power competition, which are translating into sustained government commitments to modernize and expand military capabilities. With the U.S. and allies earmarking more funds for advanced fighter jets, air defence systems, and integrated weapon suites, Lockheed’s diversified portfolio positions it to capture multi-year demand across air, naval, missile defence and space domains.

- Backlog strength, U.S. government support and global partnerships drive earnings visibility. Lockheed Martin’s upbeat 2026 outlook reflects strong backlog visibility, pricing power, and sustained support from the U.S. government through long-term defence programs, while disciplined execution on platforms such as fighter jets, missile defence, and naval systems underpins resilient cash flows. At the same time, strategic international partnerships, including its collaboration with Fujitsu on Japan’s SPY-7 radar program, expand its footprint in allied markets, diversify revenue streams, and embed the company into critical global defence supply chains.

| Entry: 180 Target: 210 Stop Loss: 165 |

| Demand resilience and smoke-free momentum drive growth |

| Key Insights |

- Nicotine demand anchors long-term revenue stability. Philip Morris benefits from structurally resilient nicotine demand, with consumers continuing to purchase cigarettes while increasingly adopting smoke-free and nicotine pouch products. The expansion of these alternatives across more than 100 markets helps offset traditional volume declines and makes the company’s revenues less sensitive to economic cycles.

- Strong FY25 results, growth to continue. Philip Morris delivered solid Q4 and FY25 results, with full-year net revenue exceeding US$40bn, driven by pricing power and growing smoke-free volumes. With smoke-free products now contributing over 40% of revenue and margins improving, management expects continued growth momentum into FY26. The company expects to achieve a CAGR of 6%-8% for FY26-FY28.

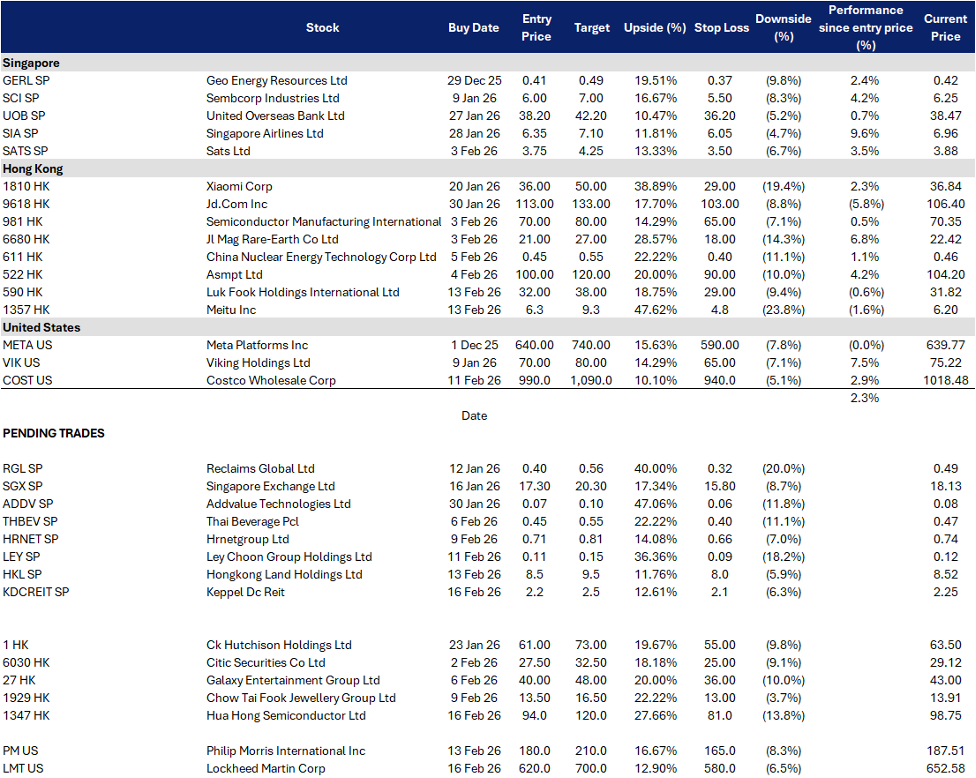

Trading Dashboard Update: Add Luk Fook Holdings International Ltd (590 HK) at HK$32 and Meitu Inc (1357 HK) at HK$6.3. Take profit on Nextera Energy Inc (NEE US) at US$92.