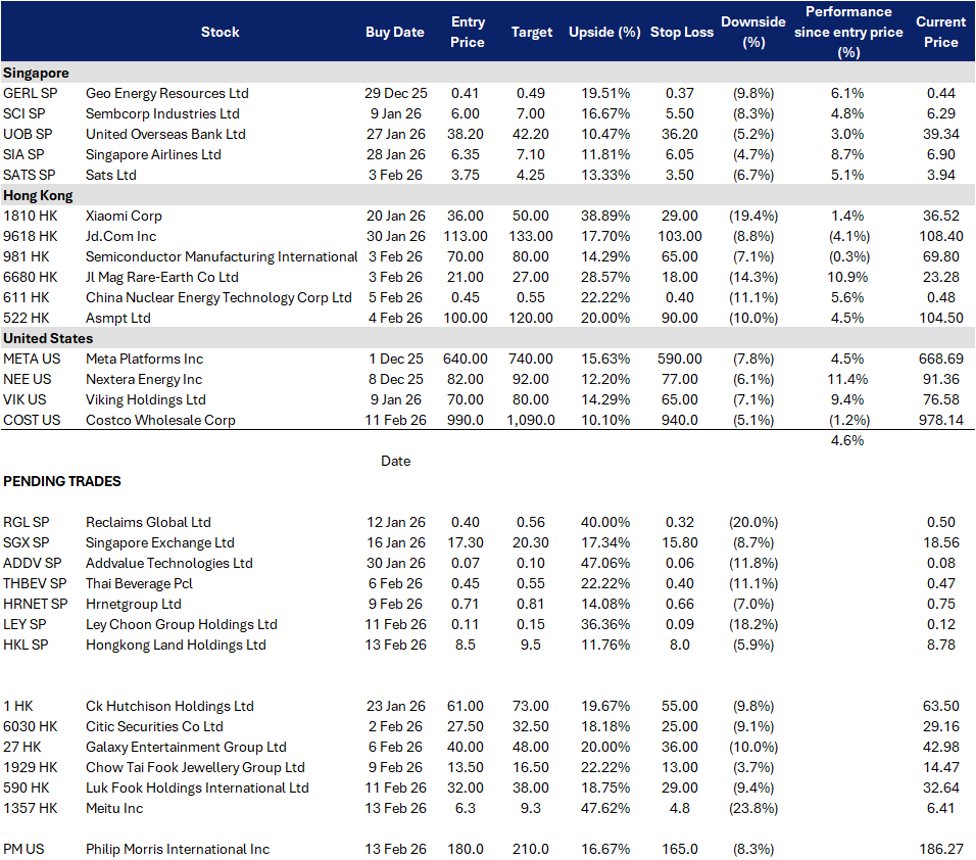

Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

Hongkong Land Holdings Limited (HKL SP)

RE-ITERATE BUY

Ley Choon Group Holdings (LEY SP)

| Entry: 8.5 Target: 9.5 Stop Loss: 8.0 |

| Central office stabilisation is real, capital recycling adds a shareholder return bid |

| Key Insights |

- Signs of a Hong Kong office floor are emerging, and the market is still sceptical. Management flagged improving enquiry levels in 1H25, with committed vacancy in the Central office portfolio down to 6.9% at end June and further to 6.4% by end September, meaningfully better than wider Central Grade A vacancy (11.8% in June and 11.0% in September).

- Singapore offices are quietly a stabiliser, while LANDMARK disruption is time bound. Singapore office vacancy is low and rental reversions remained positive, offering earnings ballast while Hong Kong offices work through negative reversions. Management disclosed 2.0% physical vacancy in Singapore at end June with average rents up YoY.

| Entry: 0.11 Target: 0.15 Stop Loss: 0.09 |

| Backlog visibility meets a Mainboard re-rating setup |

| Key Insights |

- Singapore construction demand stays resilient and keeps tender flow active. Building and Construction Authority guides 2026 total construction demand at S$47B to S$53B, broadly steady versus 2025 preliminary S$50.5B, supported by large public sector packages and extensions. That backdrop is constructive for contractors leveraged to utilities and road related scopes, where tender visibility is typically better than discretionary private building cycles.

- Mainboard transfer is a credible catalyst for liquidity, coverage, and multiple expansion. The company has received in principle approval from the Singapore Exchange Securities Trading Limited for a proposed transfer from Catalist to Mainboard, subject to shareholder approval and other conditions. For small caps, this type of step up can act as a valuation catalyst through a broader investor base and better institutional investability.

BUY

Meitu, Inc. (1357 HK)

RE-ITERATE BUY

Luk Fook Holdings (International) Ltd (0590 HK)

| Entry: 6.3 Target: 9.3 Stop Loss: 4.8 |

| AI creator tools are reaccelerating, profitability guide resets the narrative |

| Key Insights |

- Profitability guide is the near-term catalyst that the market is still digesting. Meitu guided FY25 adjusted net profit attributable to owners up 60% to 66% YoY on non IFRS metrics, driven by rapid revenue growth in the core photo, video and design products plus a meaningful increase in global paying subscribers, especially overseas.

- Monetisation mix is improving. 1H25 revenue was RMB1.8B, up 12.3% YoY, while adjusted net profit attributable to owners rose 71.3% YoY to RMB467M, implying meaningful operating leverage as AI features drive conversion and retention.

| Entry: 32 Target: 38 Stop Loss: 29 |

| Sales momentum is back, mix upgrade can re rate margins |

| Key Insights |

- Mix upgrade is the hidden margin lever, and the operating leverage is already visible. The market still anchors on weight based gold volatility, but Luk Fook is pushing a higher margin mix and tightening opex. In 1H FY2026, gross margin expanded 2.0 ppts to 34.7% and operating margin expanded 1.6 ppts to 11.4%, with total opex to revenue down 2.2 ppts to 19.1%. 3Q FY2026 data reinforces that fixed price categories are not just holding, they are growing on a high base, with fixed price gold SSS +32% and gem set SSS +66%.

- Overseas expansion adds a second narrative, while same store sales keep compounding. Store optimisation continues, but the overseas footprint is building. As at 31 Dec 2025, the group had 3,073 shops globally and opened new licensed shops in overseas regions including Thailand, Vietnam, the US and Cambodia during the quarter, with 17 new overseas shops opened in the nine months. This matters because overseas growth can diversify earnings away from a single consumption cycle, and a sustained SSS run rate tends to drive rerating faster than absolute store count.

BUY

Philip Morris International Inc. (PM US)

RE-ITERATE BUY

Costco Wholesale Corp. (COST US)

| Entry: 180 Target: 210 Stop Loss: 165 |

| Demand resilience and smoke-free momentum drive growth |

| Key Insights |

- Nicotine demand anchors long-term revenue stability. Philip Morris benefits from structurally resilient nicotine demand, with consumers continuing to purchase cigarettes while increasingly adopting smoke-free and nicotine pouch products. The expansion of these alternatives across more than 100 markets helps offset traditional volume declines and makes the company’s revenues less sensitive to economic cycles.

- Strong FY25 results, growth to continue. Philip Morris delivered solid Q4 and FY25 results, with full-year net revenue exceeding US$40bn, driven by pricing power and growing smoke-free volumes. With smoke-free products now contributing over 40% of revenue and margins improving, management expects continued growth momentum into FY26. The company expects to achieve a CAGR of 6%-8% for FY26-FY28.

| Entry: 990 Target: 1,090 Stop Loss: 940 |

| Membership-led resilience with scalable global growth |

| Key Insights |

- Membership engine supports stable and defensive growth. Costco’s membership model continues to anchor earnings stability, with 1Q26 membership fees up 14% YoY to US$1.33bn and renewal rates at 92.2% in the U.S. and Canada. Growth in paid and executive members, alongside strong value positioning, drove 6.4% same-store sales growth and supports resilient demand from higher-income consumers.

- Warehouse expansion and digital upgrades sustain sales momentum. Costco’s global expansion and efficiency initiatives remain key growth drivers, with 921 warehouses, 28 planned FY26 openings, and first-year store sales averaging US$192mn. Faster store ramp-ups, AI-enabled productivity gains, and digital enhancements are strengthening customer experience and supporting continued market share gains.

Trading Dashboard Update: Add Costco Wholesale Corp (COST US) at US$990.