Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

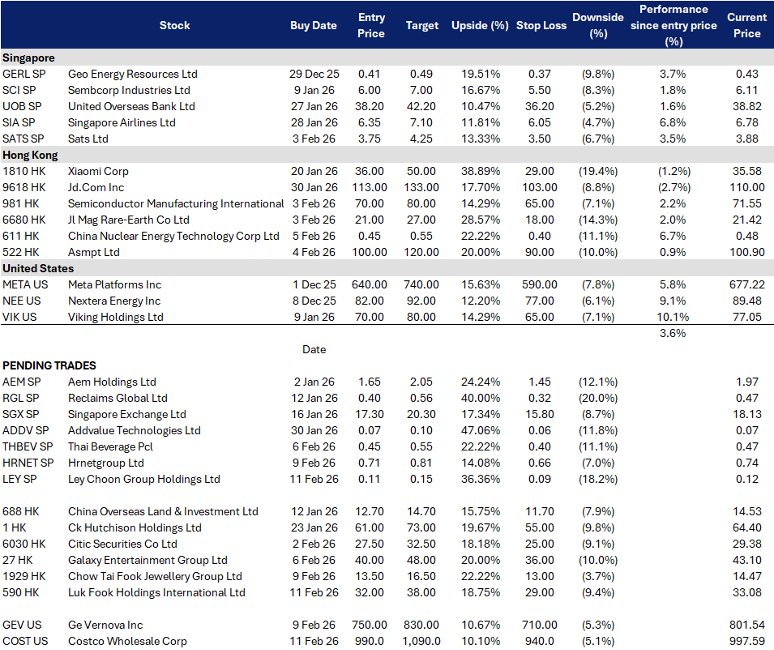

BUY

Ley Choon Group Holdings (LEY SP)

RE-ITERATE BUY

Hrnetgroup Ltd (HRNET SP)

| Entry: 0.11 Target: 0.15 Stop Loss: 0.09 |

| Backlog visibility meets a Mainboard re-rating setup |

| Key Insights |

- Singapore construction demand stays resilient and keeps tender flow active. Building and Construction Authority guides 2026 total construction demand at S$47B to S$53B, broadly steady versus 2025 preliminary S$50.5B, supported by large public sector packages and extensions. That backdrop is constructive for contractors leveraged to utilities and road related scopes, where tender visibility is typically better than discretionary private building cycles.

- Mainboard transfer is a credible catalyst for liquidity, coverage, and multiple expansion. The company has received in principle approval from the Singapore Exchange Securities Trading Limited for a proposed transfer from Catalist to Mainboard, subject to shareholder approval and other conditions. For small caps, this type of step up can act as a valuation catalyst through a broader investor base and better institutional investability.

| Entry: 0.71 Target: 0.81 Stop Loss: 0.66 |

| Hiring Tightness, Cash Buffer, Tech Upside |

| Key Insights |

- Labour market stays tight, so staffing demand does not need a boom to grind higher. Macro conditions in Singapore remain supportive for staffing volumes even if corporates are cautious. Total employment growth in 2025 was 57,300, and unemployment in Dec 2025 stayed at 2.0% overall. Importantly, 26.4% of firms expected to raise wages in the next three months (as of Dec 2025), which usually keeps churn and replacement hiring active. This environment tends to favour flexible staffing as employers keep headcount agile while still needing to fill roles.

- Public sector tech wins are building proof points for Octomate. Since late 2025, management has been pushing HR tech distribution into national workforce infrastructure. One example is EASEJobs integrating with the Careers and Skills Passport, and being one of only three job platforms in Singapore to offer that integration. More recently, Octomate won a workforce management implementation at Outward Bound Singapore for 250 staff, focused on roster scheduling and leave planning. It is not immediately material on its own, but repeated wins plus the ISO IEC 27001 and ISO IEC 27018 certifications strengthen credibility in data security, which is often a gating factor for government linked and regulated customers.

BUY

Luk Fook Holdings (International) Ltd (0590 HK)

RE-ITERATE BUY

Chow Tai Fook Jewellery Group (1929 HK)

| Entry: 32 Target: 38 Stop Loss: 29 |

| Sales momentum is back, mix upgrade can re rate margins |

| Key Insights |

- Mix upgrade is the hidden margin lever, and the operating leverage is already visible. The market still anchors on weight based gold volatility, but Luk Fook is pushing a higher margin mix and tightening opex. In 1H FY2026, gross margin expanded 2.0 ppts to 34.7% and operating margin expanded 1.6 ppts to 11.4%, with total opex to revenue down 2.2 ppts to 19.1%. 3Q FY2026 data reinforces that fixed price categories are not just holding, they are growing on a high base, with fixed price gold SSS +32% and gem set SSS +66%.

- Overseas expansion adds a second narrative, while same store sales keep compounding. Store optimisation continues, but the overseas footprint is building. As at 31 Dec 2025, the group had 3,073 shops globally and opened new licensed shops in overseas regions including Thailand, Vietnam, the US and Cambodia during the quarter, with 17 new overseas shops opened in the nine months. This matters because overseas growth can diversify earnings away from a single consumption cycle, and a sustained SSS run rate tends to drive rerating faster than absolute store count.

| Entry: 13.5 Target: 16.5 Stop Loss: 13 |

| Hard luxury rebound with mix driven margin upside |

| Key Insights |

- Demand Inflection. In the quarter ended 31 Dec 2025, Group retail sales value rose 17.8% YoY, with the Mainland up 16.9% and Hong Kong Macau plus other markets up 22.9%. Same store sales also turned decisively positive, up 21.4% in the Mainland and 14.3% in Hong Kong and Macau. This is a clear signal that discretionary appetite for jewellery is recovering even with a high gold price backdrop, which typically pressures unit volumes but supports ticket size.

- Offshore optionality is emerging as a credible second engine. The flagship store in Bangkok and plans on further store openings in Australia and Canada by end June 2026, with Middle East expansion targeted over the next two years are key progress to watch. This is strategically important because it gives the market a second narrative beyond Mainland store density and domestic consumption, and it can also help brand elevation, a key requirement for sustaining fixed price mix and pricing power.

BUY

Costco Wholesale Corp. (COST US)

RE-ITERATE BUY

GE Vernova Inc. (GEV US)

| Entry: 990 Target: 1,090 Stop Loss: 940 |

| Membership-led resilience with scalable global growth |

| Key Insights |

- Membership engine supports stable and defensive growth. Costco’s membership model continues to anchor earnings stability, with 1Q26 membership fees up 14% YoY to US$1.33bn and renewal rates at 92.2% in the U.S. and Canada. Growth in paid and executive members, alongside strong value positioning, drove 6.4% same-store sales growth and supports resilient demand from higher-income consumers.

- Warehouse expansion and digital upgrades sustain sales momentum. Costco’s global expansion and efficiency initiatives remain key growth drivers, with 921 warehouses, 28 planned FY26 openings, and first-year store sales averaging US$192mn. Faster store ramp-ups, AI-enabled productivity gains, and digital enhancements are strengthening customer experience and supporting continued market share gains.

| Entry: 750 Target: 830 Stop Loss: 710 |

| Vertical powerhouse of the electrification super-cycle |

| Key Insights |

- The AI Energy Anchor. GE Vernova acts as the critical backbone for the AI revolution, utilizing its $150 billion backlog and F-class gas turbines to meet the surging demand for 24/7 “always-on” data center power. By anchoring these hardware sales with high-margin Long-Term Service Agreements (LTSAs), the company transforms traditional equipment cycles into a resilient, software-like recurring revenue stream.

- Vertical Integration and Grid Orchestration. The $5.275bn acquisition of Prolec GE vertically integrates GEV into the high-margin transformer market, securing a critical supply chain bottleneck essential for global grid upgrades. This structural dominance is further fortified by the Xcel Energy Strategic Alliance and the GridOS platform, which lock in multi-gigawatt capacity and position GEV as the “partner of choice” for intelligent grid orchestration.

Trading Dashboard Update: No changes to Trading Dashboard.