Sector Performance | Singapore | Hong Kong | United States | Trading Dashboard

United States

Hong Kong

BUY

UMS Integration Ltd (UMSH SP)

RE-ITERATE BUY

Addvalue Technologies (ADDV SP)

| Entry: 1.30 Target: 1.45 Stop Loss: 1.24 |

| AMAT-linked beta, Bursa dual-listing liquidity, and a 2026 WFE upturn |

| Key Insights |

- AI buildout is pulling forward WFE orders into 2026. SEMI’s year-end outlook lifts 2025 total semiconductor equipment to $125–133B and projects $138B+ in 2026, with WFE up on HBM memory and leading-edge logic adds. Tool leaders like ASML are guiding for stronger 2026 sales on record orders. UMS’s core is chamber and precision assemblies for AMAT’s Endura deposition line, which should benefit as foundry and memory capex normalises upward into 2026.

- Prints show resilience; dividends intact while mix improves. 1H FY2025 revenue S$125.0M (+14% YoY) with a 1.0-cent interim DPS. 3Q FY2025 revenue S$59.3M (−9% YoY) as some semiconductor and aerospace lines softened, yet YTD EPS improved and NAV per share rose to 60.25 cents by Sep-2025, underscoring balance-sheet strength into the upcycle.

| Entry: 0.068 Target: 0.100 Stop Loss: 0.060 |

| IDRS lead, turnaround momentum, and contract pipeline support 2026 carry |

| Key Insights |

- Real-time LEO ops are moving from nice-to-have to must-have. Earth observation, asset monitoring and responsive space missions increasingly need continuous command, telemetry and payload data outside ground-station passes. Addvalue’s IDRS is advertised as the only space-proven commercial option delivering always-on IP sessions over GEO L-band with session continuity across spot-beam handovers. As more smallsat operators prioritize latency and uptime, attach rates for relay terminals and airtime can rise, supporting recurring service revenue on top of hardware.

- Installed base and airtime scale can compound. AGM disclosures indicate a growing on-orbit terminal base with additional units awaiting launch, which should translate into higher airtime adoption as fleets scale. The combination of new terminals shipped and rising in-service units expands recurring revenue and improves working-capital turns as the model shifts toward services.

BUY

ASMPT Ltd (522 HK)

RE-ITERATE BUY

CITIC Securities Co Ltd (6030 HK)

| Entry: 100 Target: 120 Stop Loss: 90 |

| Advanced packaging upcycle, SMT options, and AI orders momentum |

| Key Insights |

- AI packaging tide. AI spend is lifting advanced packaging demand into 2026. Industry work points to rising HBM4, hybrid bonding, and panel or glass transitions, all supportive for SEMI where ASMPT cites TCB leadership in logic and memory. Bookings have shown six straight quarters of YoY growth on AI exposure and gross margin ran above 40% in 1H25, indicating pricing power returning as mix improves.

- SMT strategic options can unlock value. On 21 Jan 2026 management began assessing options for the SMT Solutions segment including divestiture, JV, spin-off or listing. A decision that sharpens focus on SEMI or crystallises value in SMT could raise group ROIC and reduce earnings cyclicality.

| Entry: 27.5 Target: 32.5 Stop Loss: 25.0 |

| China deal engine with policy tailwinds and fee leadership |

| Key Insights |

- Policy push and market plumbing support activity. The CSRC’s 2026 work plan prioritises market stability, deeper long-term capital and wider two way opening including QFII optimisation and broader futures access. Recent fine tuning to curb leverage while keeping the rally durable indicates a preference for steady turnover and higher quality issuance rather than boom bust swings. That backdrop is constructive for a scaled franchise that earns across brokerage, underwriting and FICC.

- Fee leadership with diversified engines. CITIC Securities ranked number one in APAC ex Japan investment banking fees in 2025, supported by bond and equity underwriting depth. Scale in asset management and market making augments earnings when primary markets pause and positions the group to capture any revival in IPOs and refinancings.

RE-ITERATE BUY

Coherent Corp. (COHR US)

RE-ITERATE BUY

Lumentum Holdings Inc. (LITE US)

| Entry: 200 Target: 230 Stop Loss: 185 |

| Embedded winner in the AI optics supply chain |

| Key Insights |

- Component-level leverage to expanding datacentre optics demand. AI workloads are expected to drive a surge in optical interconnect and sensing needs. Coherent’s position as a leading supplier of critical laser chips, EMLs, VCSEL arrays, and advanced photonic materials makes it a direct beneficiary regardless of which module vendors gain share. With datacentre & communications revenue up 26% YoY in Q1, Coherent captures demand at the component level where substitution risk is lowest, and pricing power is highest during shortages.

- Strategic focus and technology leadership align with optical expansion trends. The divestment of the Aerospace & Defense business has sharpened Coherent’s focus on high-growth AI datacentre and communications markets, lifting margins and EPS. Combined with new award-winning 400G/1.6T optical technologies and expanded production capacity, Coherent is well positioned to monetise the projected AI infrastructure supercycle as hyperscalers deploy nearly 100GW of new datacentre capacity through 2030.

| Entry: 450 (buy stop) Target: 500 Stop Loss: 425 |

| Leveraging the AI interconnect bottleneck |

| Key Insights |

- Optics bottleneck and hyperscale network buildouts to drive demand growth. With JLL forecasting nearly 100 GW of new data-centre capacity from 2026-2030 and a 14% CAGR for the global data-centre sector through 2030, optics are becoming the next infrastructure constraint after compute, particularly in AI scale-up and inference workloads. Meta’s multi-year US$6bn fibre deal with Corning reinforces the trend toward massive fibre and transceiver deployment, positioning Lumentum’s high-speed 1.6T transceivers, EML lasers, and optical switching technology for both volume growth and upward pricing as hyperscalers race to interconnect tens of thousands of AI nodes with high-bandwidth optics.

- Strong execution and next-generation optics inflect revenue and margin. Lumentum’s first quarter revenue growth of 58% YoY and more than 1,500bps non-GAAP margin expansion, highlight early success in data-centre optics, with guidance indicating more than 20% sequential revenue growth ahead of broader ramps of optical circuit switches and co-packaged optics. As data-centre capacity grows, its broad optical portfolio will enable Lumentum to capture both near-term demand and long-term growth tied to the global AI infrastructure supercycle.

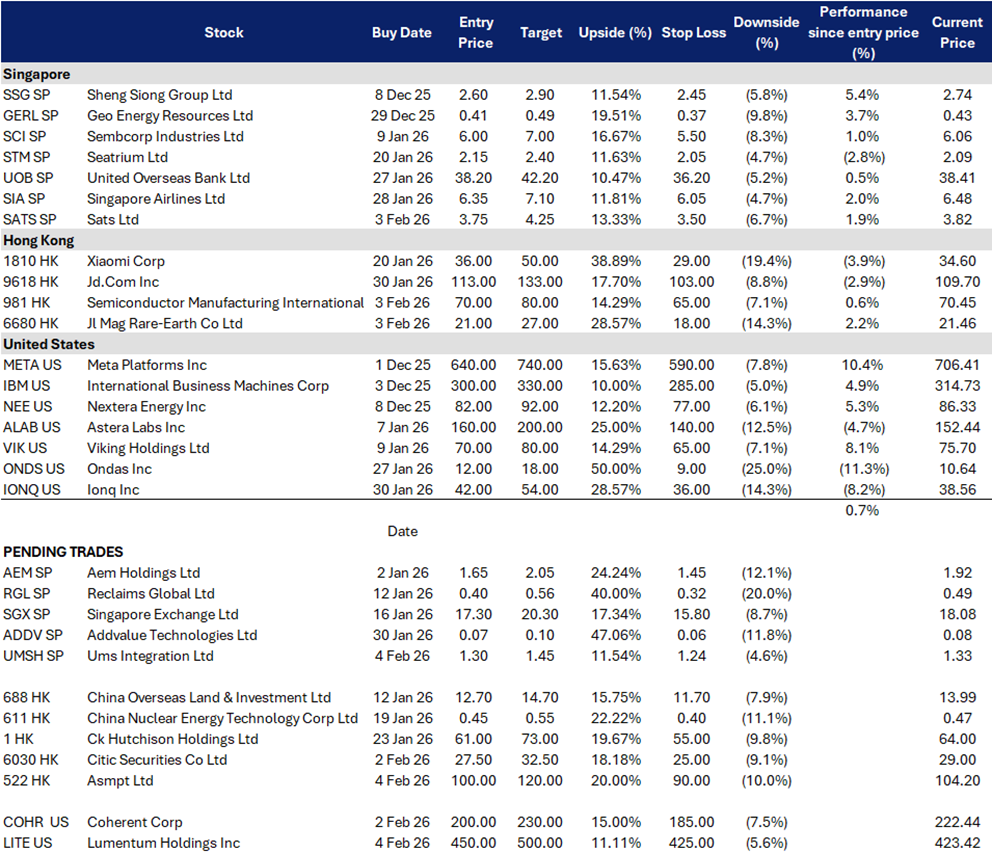

Trading Dashboard Update: Add SATS Limited (SATS SP) at S$3.75, Semiconductor Manufacturing International Corp (981 HK) at HK$70 and Jl Mag Rare-Earth Co Ltd (6680 HK) at HK$21. Cut Horizon Robotics (9660 HK) at HK$8.