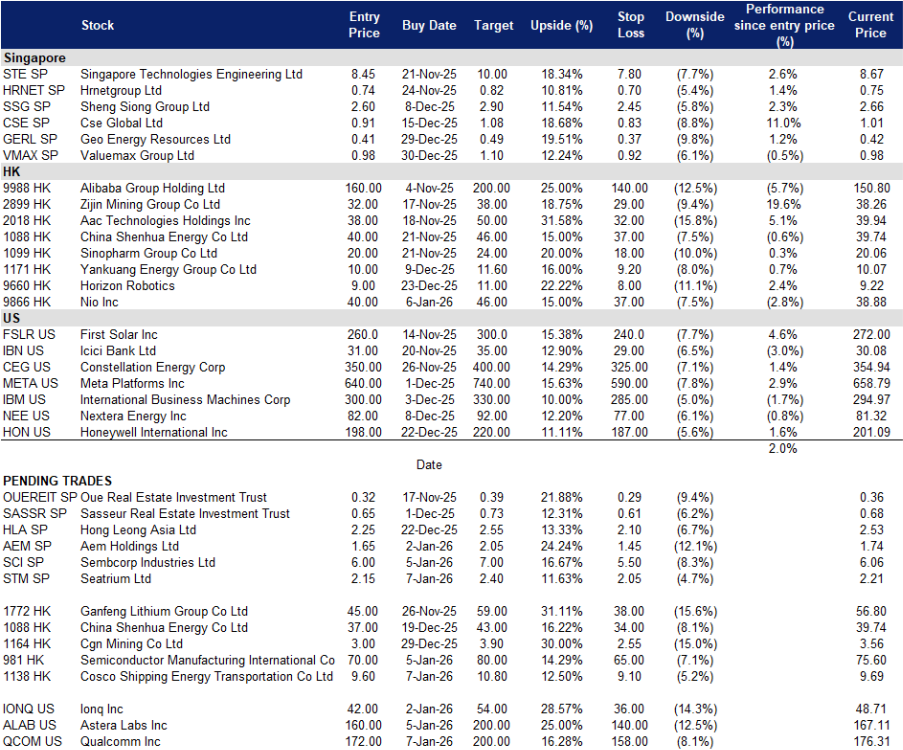

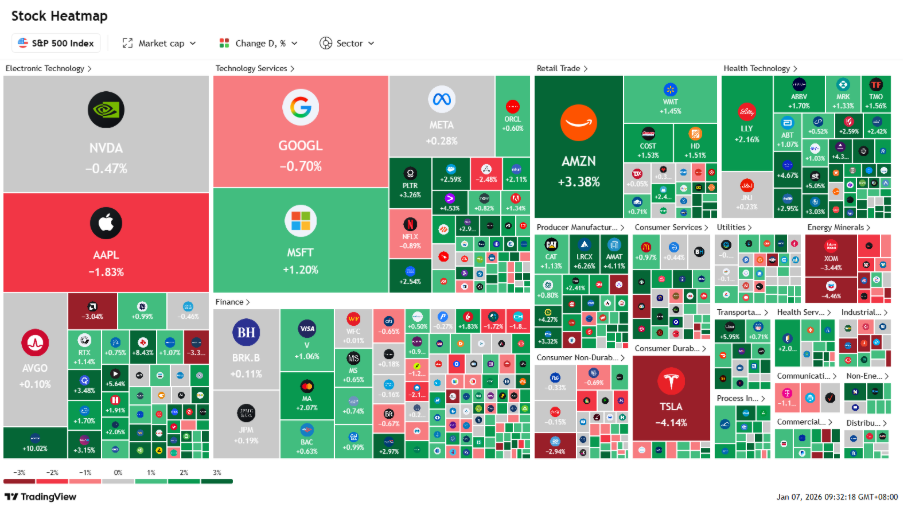

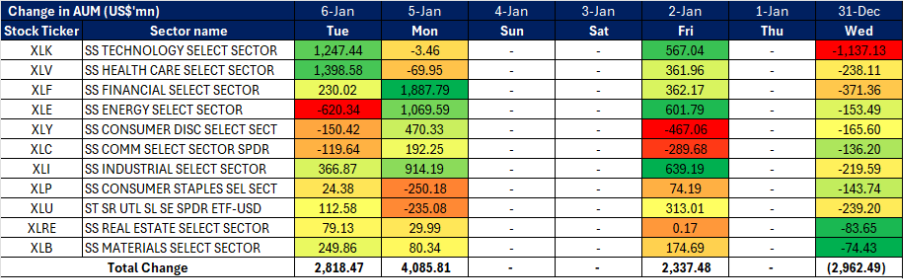

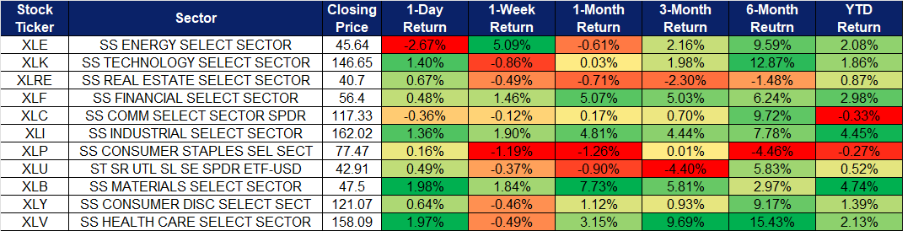

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

Seatrium Ltd. (STM SP): Seatrium Oil Security Premium Lifts FPSO Cycle. Order Cover To 2031. Transition Projects Add Balance

- BUY Entry – 2.15 Target – 2.40 Stop Loss – 2.05

- Seatrium Ltd offers engineering solutions for the offshore, marine, and energy industries. The Company provides rigs and floaters, repairs and upgrades, offshore platforms, and specialized shipbuilding. Seatrium serves customers worldwide.

- Venezuela disruption tightens heavy supply and keeps offshore spend high. Sanctions escalation and the U.S. blockade have sharply curtailed Venezuelan exports and forced PDVSA to cut production, removing a key heavy supply source and lifting the medium-term premium on reliable offshore barrels in Brazil, Guyana and the Gulf of Mexico. This is supportive for FPSO awards where Seatrium is already the lead contractor on Petrobras P-84 and P-85. A prolonged Venezuelan outage and any eventual rebuild both bias demand toward large yard capacity.

- Diversified backlog and improving mix argue for rerate. Net order book stood at about S$16.6B as of the 3Q update with deliveries through 2031 and a visible pipeline across FPSOs, platforms and grid related systems. Management is targeting better margins via project mix and cost programs after resolving the Brazil legacy probe, which removes a governance overhang. This combination increases earnings visibility without relying on a single segment.

- Offshore wind and grid platforms complement oil and gas cycle. Beyond hydrocarbons, Seatrium is delivering converter platforms for TenneT in the Dutch North Sea and other offshore wind assets in Europe and Asia. These programs diversify the backlog and create medium term balance as energy transition spending resumes.

- 1H25 results review. Revenue S$5.4B, +34% YoY. Net profit S$144M, +301% YoY. Gross margin improved on higher margin projects and efficiencies. Net order book at S$18.6B at end June with deliveries to 2031. Company reiterated progress toward 2028 targets and highlighted stable demand for offshore energy infrastructure and steady activity in offshore wind and repair.

- Market consensus

(Source: Bloomberg)

Sembcorp Industries Ltd. (SCI SP): Data Center Power Upcycle, Carbon Tax Pricing Power, India FDRE Pipeline

- RE-ITERATE BUY Entry – 6.0 Target – 7.0 Stop Loss – 5.5

- Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

- DC load rising, carbon tax steps up, system needs firm capacity. EMA projects continued demand growth and a 5-year capacity plan that preserves reserve margins as electrification and data centers scale. Singapore’s carbon tax rises to S$45/tCO₂ in 2026–2027, supporting wholesale price structures and rewarding efficient fleets and firming assets. Regional FDRE and RTC tenders in India add a structural market for renewables plus storage. Together, these forces support Sembcorp’s portfolio earnings into 2026.

- Mix shift plus disciplined capital unlock a rerate. Management is executing a renewables scale-up while keeping underlying earnings resilient. The 25 GW by 2028 pathway and asset recycling create room to fund storage and grid-adjacent capex without stressing equity. Raised interim DPS signals confidence in cash generation, while Singapore market reforms on flexibility and DR expand merchant optionality around the core contract book.

- India FDRE wins and acquisitions add bankable growth. Sembcorp won a 150 MW firm and dispatchable renewable award in India and completed the ReNew Sun Bright acquisition in Dec-2025, lifting contracted renewable megawatts and adding long-tenor PPAs. This improves visibility on returns and accelerates the glidepath toward the 2028 target.

- 1H25 results review. Net profit S$536m (−1% YoY). Underlying net profit S$491m. Interim dividend 9.0 cents. Segments: Gas and Related Services S$330m NPI before EI (−3% YoY) on softer Singapore spreads offset by Senoko; Renewables S$132m (+27% YoY) on India wind and higher operational capacity; Integrated Urban Solutions S$74m (+1% YoY). Gross installed renewables 13.8 GW vs 10.0 GW a year ago.

- Market consensus

(Source: Bloomberg)

COSCO SHIPPING Energy Transportation Co., Ltd. (1138 HK): Ton-mile Tailwinds, Disciplined Supply, LNG Ballast

- BUY Entry – 9.6 Target – 10.8 Stop Loss – 9.1

- COSCO SHIPPING Energy Transportation Co., Ltd. offers marine shipping services. The Company provides refined oil transportation, crude oil transportation, and other services. COSCO SHIPPING Energy Transportation also ships iron ores, dry bulks, coal, and other products.

- Tanker cycle still constructive; longer voyages and tight effective supply. Dirty tanker earnings remain healthy with the Baltic Dirty Tanker Index around 1,319 late December, while VLCC TCEs over the last year averaged ~$39,400 per day, above cash break-evens. The VLCC orderbook sits near 11.5% of the fleet, limiting net supply through 2027. Geopolitics are adding distance: shifting Atlantic-to-Asia crude flows and cautious routing continue to raise ton miles. This backdrop supports COSCO Energy’s core crude exposure into 2026.

Baltic Dirty Tanker Index

(Source: Bloomberg)

- Venezuela shock creates two-way support for ton miles. Fresh sanctions enforcement and irregular Venezuelan liftings are disrupting trade patterns. Reports show multiple Venezuelan cargoes departing in “dark mode,” while Chevron cargoes resumed after a brief halt. Tighter enforcement curbs straightforward short-haul sales and pushes buyers to source farther barrels, which typically lifts VLCC demand; a future normalization would also be positive by reopening very long-haul Venezuela-to-Asia routes. Either path is constructive for mainstream owners with global networks.

- LNG ballast and capital discipline. The company controls a leading LNG JV portfolio alongside crude and product fleets, adding earnings ballast as LNG trade expands. Management’s contracted capex schedule and large but manageable vessel commitments through 2028 support balance sheet resilience while preserving operating leverage to the tanker cycle.

- 1H25 results review. Revenue RMB11.573B −2.5% YoY. Profit attributable to equity holders RMB1.894B. Capital commitments RMB19.31B for vessels scheduled 2025–2028.

- Market consensus

(Source: Bloomberg)

Semiconductor Manufacturing International Corp. (981 HK): Policy Localisation Plus Record Revenue Outlook Support Mature Node Leadership

- RE-ITERATE BUY Entry – 70 Target – 80 Stop Loss – 65

- Semiconductor Manufacturing International Corporation operates as a semiconductor foundry. The Company provides integrated circuit foundry and technology services including the testing, development, design, manufacturing, packaging, and sale of integrated circuits. Semiconductor Manufacturing International offers its products and services around the world.

- Policy push lifts domestic share and capacity approvals. Beijing has directed that at least 50% of tools used in new wafer capacity be domestically produced. Combined with the Big Fund’s latest capital round, this accelerates approvals and anchors capex for mature nodes where domestic tools are viable. Into 2026, WSTS projects the global semiconductor market to approach about $975B, with Logic and Memory leading. This backdrop supports China localisation and stable demand for SMIC’s core nodes as supply chains rebalance.

- Tailwind on portfolio consolidation and asset quality. SMIC is taking full control of SMNC via a CNY40.6B share deal, simplifying the structure and adding 12-inch capability directly onto the parent balance sheet. The move should improve capital allocation, utilisation planning and disclosure at group level as domestic equipment share increases under the new policy regime.

- Localisation of handset silicon and mature node mix. China smartphone leaders are regaining share and raising domestic content, which supports local foundry demand for modem, RF, power management and application processors on mature processes. While handset shipment trends are uneven, Huawei’s resurgence and ongoing contract wins in China provide a more dependable local order book into 2026.

- 3Q25 results review. Revenue $2.38B, +9.7% YoY, ahead of consensus. Net profit $191.8M, +28.9% YoY. Management and trackers flagged a full year revenue outlook above $9B. Gross margin around 22% with utilisation near 96%.

- Market consensus

(Source: Bloomberg)

Qualcomm Inc. (QCOM US): AI PC Ramp Meets Nvidia CES Halo, Auto Pipeline Compounds Edge AI Narrative

- BUY Entry – 172 Target – 200 Stop Loss – 158

- Qualcomm Incorporated operates as a multinational semiconductor and telecommunications equipment company. The Company develops and delivers digital wireless communications products and services based on CDMA digital technology. Qualcomm serves customers worldwide.

- CES 2026 sets an “AI everywhere” tone that lifts Qualcomm’s edge story. Nvidia’s CES keynote emphasized “physical AI” and unveiled next-gen platforms for autonomous systems. This keeps investor focus on on-device and vehicle-grade inference, a lane where Qualcomm already ships efficient NPUs in phones and is now scaling AI PCs and automotive compute. In parallel, Qualcomm used CES to expand its Windows-on-Arm lineup with Snapdragon X2 Elite and X2 Plus, signaling broader OEM support and higher NPU TOPS this cycle. The net effect is a stronger demand backdrop for low-power edge AI silicon and attach on connectivity and RF.

- Product moat, platform reach, and hyperscaler pull. Q4 FY25 showed QCT record revenue with Handsets $6.96B, Automotive $1.05B, and IoT $1.81B. For FY25, Automotive and IoT combined grew 27% and total QCT non-Apple revenue rose 18%. Management guided Q1 FY26 revenue to $11.8B–$12.6B with non-GAAP EPS $3.30–$3.50, indicating continued momentum while AI PCs begin to layer in. Qualcomm’s automotive design-win pipeline remains about $45B, supported by programs such as Snapdragon Ride with BMW, which broadens visibility into the late-decade model years.

- RF front-end leadership and PC attach are underappreciated levers. Independent tracking places Qualcomm as the leading RFFE vendor by market share, helped by the integrated modem-RF platform. As AI PCs proliferate in 1H26, Qualcomm’s X-series should drive incremental content across Wi-Fi 7, Bluetooth, audio, and platform power management, supporting blended gross margin resilience even as handset units normalize.

- 4Q25 results review. Revenue $11.27B, +10% YoY. Non-GAAP EPS $3.00, +12% YoY. QCT revenue mix: Handsets $6.96B (+14% YoY), Automotive $1.05B (+17% YoY), IoT $1.81B (+7% YoY). Guidance Q1 FY26: Revenue $11.8B–$12.6B, QCT $10.3B–$10.9B, QTL $1.4B–$1.6B, non-GAAP EPS $3.30–$3.50.

- Market consensus

(Source: Bloomberg)

Astera Labs, Inc. (ALAB US): PCIe 6 And CXL Adoption Accelerates, UALink Momentum, Fabric Switch Wins Broaden The TAM

- RE-ITERATE BUY Entry – 160 Target – 200 Stop Loss – 140

- Astera Labs, Inc. provides semiconductor-based connectivity solutions. The Company develops and deploys intelligent connectivity platforms built for cloud and AI infrastructure. Astera Labs serves customers in the United States, Canada, China, Taiwan, and Israel.

- Standards are breaking out, AI racks need more lanes and pooled memory. PCIe 6.0 and CXL 3.x are moving from pilots to production as AI server complexity rises. Astera is ramping PCIe 6 connectivity into deployment, while CXL memory controllers are already showcased on Microsoft Azure M series to expand addressable memory for AI and in-memory databases. The company is a promoter and board member of the UALink Consortium, which advanced the 200G 1.0 spec and highlighted real-world demos at Flash Memory Summit and OCP Global Summit. This standards cadence enlarges silicon content per rack and supports multi-year unit growth.

- Product moat, platform reach, and hyperscaler pull. Astera positions across GPUs, DPUs, NICs, storage, and memory tiers, not just a single socket. Aries 6 class retimers are designed for PCIe 6 and CXL 3.x topologies, Scorpio fabric switches target Blackwell class MGX platforms, and the Cloud-Scale Interop Lab reduces time to qualified deployment. Multi-platform support and interoperability leadership create switching costs and shorten adoption cycles as hyperscalers refresh fleets.

- Expanding solution scope and custom engagements. Management is extending the portfolio with custom connectivity solutions and gearbox offerings, which can raise average selling price and deepen customer stickiness as racks scale. UALink device road maps, together with next PCIe 6 server launches, provide additional headline catalysts.

- 3Q25 results review. Revenue $230.6M, +104% YoY, +20% QoQ, a record driven by new AI platform ramps and multiple product families. Non-GAAP operating margin 41.7%. Management cited Scorpio fabric switch design wins at several hyperscalers.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Add Nio Inc (9866 HK) at HKD 40. Take profit on Southern Copper Corp (SCCO US) at US$154 and Zijin Mining Group Co Ltd (2899 HK) at HKD 38.