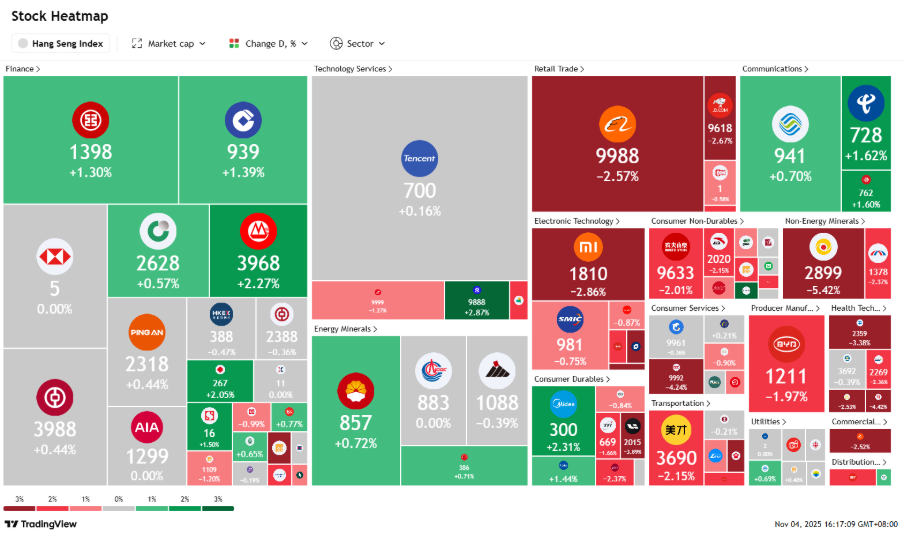

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

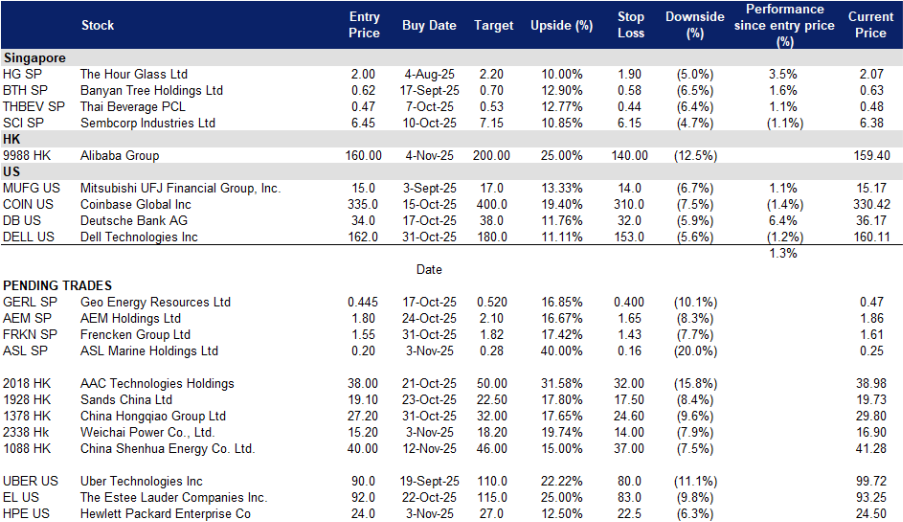

ASL Marine Holdings Ltd (ASL SP): Tuas Tailwind Fuel Further Upside

- RE-ITERATE BUY Entry – 0.20 Target – 0.28 Stop Loss – 0.16

- ASL Marine Holdings Ltd. operates as a holding company. The Company, through its subsidiaries, engages in shipbuilding, shiprepair and conversion, marine vessel chartering, marine engineering, and other related services. ASL Marine Holdings serves customers worldwide.

- Contracted revenue step-up not fully in price. The company disclosed new ship chartering contracts of $82M over about two years, plus vessel sale contracts of $55M to advance deleveraging and streamline the fleet. The charter scope covers tugs, barges, hopper barges, and grab dredgers that support ongoing marine infrastructure works in Singapore. These contracts were announced on 27 Oct 2025, after the June year-end. As of 30 Jun 2025, the long-term shipchartering order book stood at about $38M. Pro forma, the new $82M package would more than double long-term revenue visibility for the chartering segment and underpins earnings through FY26, yet the share price reaction has been muted relative to the quantum of contracted work. This is likely because revenue will be recognised over time, and investors may still be anchored to prior declines in chartering revenue. The incremental visibility and mix shift toward longer tenors should support higher utilisation, steadier margins and better cash conversion.

- Macro tailwinds from Singapore marine works and Tuas expansion. MPA notices point to continued reclamation, dredging and port development activities, including Tuas Terminal Phase 2 and works across Tuas View and the northern coast. These projects require exactly the vessel classes ASL operates, such as hopper barges, tugs and workboats. This backdrop supports sustained demand for ship repair and chartering in local waters and adjacent routes. As activity stays elevated, repair margins should remain healthy. In FY25, group gross margin expanded to 17.3%, with ship repair gross margin at 25.8%.

- Deleveraging path and undemanding valuation. FY25 revenue was $350.1M with profit attributable to shareholders of $14.6M. Total borrowings fell to $178.9M and cash rose to $22.8M, aided by vessel disposals and refinancing. The board proposed a first and final dividend of 0.2 cents per share, signalling balance sheet normalisation. With about 988M shares outstanding, market capitalisation around the current price implies an enterprise value near $380M. On FY25 adjusted EBITDA of $83.7M, the EV to EBITDA multiple is about 4 to 5 times, a discount to regional marine services peers, given improving order visibility. Near-term one-off disruptions are possible, such as the one in Batam, but they do not change the multi-year infrastructure demand or the secured charter backlog.

- FY25 results review. FY25 revenue rose by 0.2% to S$350.1m, compared to S$349.3m in FY24. Net profit increased by 272.3% to S$14.6m in FY25, compared to S$3.9m in FY24. Basic earnings per share rose to S$0.015 in FY25, from roughly S$0.004 in FY24.

- Market consensus

(Source: Bloomberg)

Frencken Group Ltd (FRKN SP): Macro-driven semi upcycle beneficiary

- RE-ITERATE BUY Entry – 1.55 Target – 1.82 Stop Loss – 1.43

- Frencken Group Limited designs, develops, and produces complex and advanced modules and systems, based on precision mechanics, hardware and software.

- Semiconductor upcycle is intact, lifting tool makers and their tier-1 suppliers. WSTS projects the chip market to grow about 11% in 2025 to roughly $701B, with Memory and Logic leading on AI demand. Semi sales in 1H25 were up 18.9% year on year globally. This backdrop is flowing into wafer-fab equipment, where SEMI expects 2025 equipment sales to reach about $125B. ASML just reported a stronger order book on AI-related demand, a leading indicator for sub-system suppliers. Frencken’s semiconductor segment already grew 37.5% year on year to $215.7M in 1H25 and contributed about half of group revenue, showing direct leverage to the cycle.

- Supply chain diversification and local capacity expansion support multi-year programs. Customers are re-balancing production across Europe, the US and Asia, while Singapore’s electronics PMI is back in expansion. Frencken is adding capacity and capability, including a new Singapore facility, and previously entered a land lease to develop a manufacturing site. This improves throughput and qualification readiness for more complex modules.

- Results momentum and consensus support into 2H25, with room to re-rate. 1H25 revenue rose 15.7% and PATMI rose 9.9%, driven by mechatronics strength. Brokers turned constructive on 2H25, citing the semiconductor upswing, with recent targets in the $1.68 to above $2.00 range. The stock trades around mid-teens P/E on TTM, below some local equipment peers on growth-adjusted terms.

- 1H25 results review. 1H25 revenue $431.4M, up 15.7% year on year. Net profit $19.9M, up 9.9% year on year. Semiconductor segment $215.7M, up 37.5%, about 50% of group revenue. Operating cash flow $21.9M vs $8.4M in 1H24, with inventories lower by $9.3M.

- Market consensus

(Source: Bloomberg)

China Shenhua Energy Co. Ltd. (1088 HK): Dividend Catalyst in Focus

- BUY Entry – 40.0 Target – 46.0 Stop Loss – 37.0

- China Shenhua Energy Company Limited mines and distributes coal products. The Company produces brown coal products, bituminous coal products, hard coal products, coking coal products, and other related products. China Shenhua Energy also operates electricity generation, railway transportation, and other businesses.

- Policy keeps coal central to energy security, which anchors Shenhua’s volumes. China finalised a coal production reserve system that targets 300 million tonnes of “dispatchable” annual coal capacity by 2030, roughly 6% of last year’s output, to stabilise supply and prices for power producers. In addition, regulators approved 25 GW of new coal power in 1H 2025, keeping thermal generation available as renewables scale. National rail freight volume rose 3.4% year to date through September 2025, supporting bulk commodity flows. Shenhua’s integrated mine-to-rail-to-port-to-power chain is positioned to monetise this policy-backed throughput.

- Cash generation and dividends continue to support equity value. Operating cash flow in 1H 2025 was RMB 45.8 billion. The board approved an interim dividend of RMB 0.98 per share, payable on 24 December 2025, with Hong Kong payment translated at RMB 1 to HKD 1.096. Consistent and visible cash returns, underpinned by integrated operations, provide a valuation anchor while investors track monthly operating prints.

- Scale and integration show up in hard operating data. In 1H 2025, Shenhua produced 165.4 million tonnes of commercial coal and sold 204.9 million tonnes. Self-owned railway transportation turnover reached 152.8 billion tonne-kilometres, with unit railway cost at RMB 0.080 per tonne-kilometre. The September operating update showed a further improvement, with self-owned railway turnover at 27.0 billion tonne kilometres, up 13.4% year on year. These data points demonstrate cost-advantaged logistics and improved utilisation in the second half.

- 1H25 results review. Revenue decreased by 18.3% to RMB138.109 billion, compared to RMB169.121 billion in 1H24. Profit attributable to equity holders decreased by 14.8% to RMB26.706 billion, compared to RMB31.356 billion in 1H24. Basic earnings per share decreased by 14.8% to RMB1.344 per share in 1H25, compared to RMB1.578 per share in 1H24. Net cash generated from operating activities decreased by 11.7% to RMB45.794 billion from RMB51.890 billion.

- Market consensus

(Source: Bloomberg)

Weichai Power Co., Ltd. (2338 HK): Green trucks stealing the show

- RE-ITERATE BUY Entry – 15.20 Target – 18.20 Stop Loss – 14.00

- Weichai Power Co., Ltd. specializes in the research and development, manufacturing and sales of vehicles and parts. The Company produces engines, heavy vehicles, light vehicles, construction machinery, hydraulic products, automotive electronics, and related parts. Weichai Power markets its products across worldwide.

- Latest print shows momentum and a clear EV-truck growth driver. Q3 2025 net profit rose 29.5% year on year; for the first nine months, revenue reached RMB170.6B and net income RMB8.88B, implying a solid Q3 step-up versus 1H. Management and local media also highlighted new-energy heavy-duty truck sales up 255% YoY in 1H 2025, positioning Weichai to capture the fastest-growing profit pool in China’s truck market. Formal Q4 update and monthly NE-truck registrations; any disclosure on large orders in municipal logistics and short-haul routes will cause a re-rating of the stock. Momentum is visible in the company’s NE-truck unit growth and Q3 earnings.

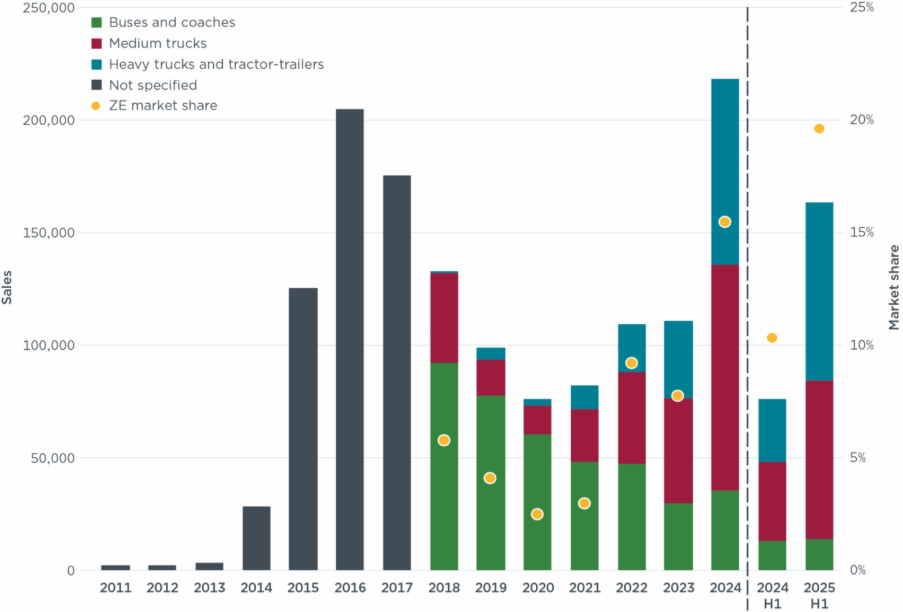

- Macro adoption curve still steep: China EV-truck share rising fast. Independent trackers show battery-electric heavy trucks reached 22% share in China in 1H 2025, with ~80k e-trucks sold in China in 1H alone — more than all of 2024 — as charging and swap networks scale. CATL guides that EVs could reach 50% of China’s heavy-truck sales by 2028, reinforcing a multi-year unit/parts & service flywheel for leading system suppliers.

Zero-emission medium- and heavy-duty vehicle market in China

(Source: ICCT)

- Balance sheet/returns and external levers backstop the equity case. Fitch affirms BBB+ / Stable, noting robust net cash and 10% 2025 EBITDA margin expectations; KION’s one-off program charges concentrate in 1H and should fade, offering a 2026 margin tailwind. On top, Weichai has an on-market buyback authorisation, and Street targets cluster in the HK$19–21 range.

- 1H25 results review. 1H25 revenue rose by 0.6% to RMB113.15B, compared to RMB112.49B in 1H24. Net profit fell by 4.4% to RMB5.64B in 1H25, compared to RMB5.90B in 1H24. Basic earnings per share decreased by 4.4% to RMB0.65 per share in 1H25, compared to RMB0.68 per share in 1H24.

- Market consensus

(Source: Bloomberg)

Hewlett Packard Enterprise Co. (HPE US): Reinventing the enterprise cloud

- RE-ITERATE BUY Entry – 24.0 Target – 27.0 Stop Loss – 22.5

- Hewlett Packard Enterprise Company provides information technology solutions. The company offers enterprise security, analytics and data management, applications development and testing, data center maintenance, cloud consulting, and business process services. Hewlett Packard Enterprise serves customers worldwide.

- AI infrastructure and networking transformation. Hewlett Packard Enterprise’s pivot toward AI infrastructure and hybrid cloud positions it at the center of enterprise digital modernization. The successful acquisition of Juniper Networks has doubled HPE’s networking business and integrated AI-native technology across hardware, software, and security, narrowing the competitive gap with Cisco. The new Cloud and AI division will enable HPE to capture the surging demand from enterprises deploying AI-driven workloads, supported by projected global AI infrastructure spending expected to reach US$758bn by 2029.

- Enhancing GreenLake market positioning. GreenLake has shifted from a simple pay-as-you-go cloud infrastructure to a higher-level hybrid cloud/edge/AI platform. As of 3Q25, the company’s ARR is approximately US$3bn, an increase of 77% YoY. GreenLake added 2,000 new customers, bringing its total customer count to 44,000.

- PC refresh and AI-driven edge growth. The ongoing Windows 11 refresh cycle and the rapid rise of AI-capable PCs are catalyzing new infrastructure demand that benefits Hewlett Packard Enterprise’s edge computing and data services. According to IDC, global PC shipments grew 9.4% YoY in 3Q25, with the refresh cycle expected to extend into 2026. As enterprises modernize endpoints to support AI workloads, HPE is well-positioned to capture adjacent growth in compute, storage, and network orchestration.

- 3Q25 results. Revenue increased by 3.1% YoY to US$13.9bn, with non-GAAP diluted earnings per share at US$0.75, down 10.7% YoY. During the quarter, the company returned US$400mn to shareholders in the form of dividends and share repurchases. For Q4, the company expects non-GAAP diluted earnings per share to be between US$0.87 and US$0.97. For FY25, the company anticipates free cash flow to be between US$2.6bn and US$3.0bn. Revenue for FY26 is projected to grow between 17% and 22%, compared to a forecasted growth of 17.2%. Free cash flow is expected to be between US$1.5bn and US$2.0bn, compared to a forecast of US$1.88bn.

- Market consensus

(Source: Bloomberg)

Dell Technologies Inc (DELL US): AI server shipments to double

- RE-ITERATE BUY Entry – 162 Target – 180 Stop Loss – 153

- Dell Technologies Inc. provides computer products. The Company offers laptops, desktops, tablets, workstations, servers, monitors, printers, gateways, software, storage, and networking products. Dell Technologies serves customers worldwide.

- AI infrastructure driving record growth. Dell continues to benefit from exceptional AI demand, with its Infrastructure Solutions Group (ISG) reporting record Q2 revenue of US$16.8bn, up 44% YoY, led by a 69% surge in servers and networking. The company has already shipped US$10bn worth of AI servers in 1H26 and raised its full-year AI server shipment target to US$20bn, underscoring its role as a key Nvidia partner and a core supplier for AI workloads to clients like CoreWeave and xAI. Dell now expects long-term compounded annual revenue growth of 11% to 14% for ISG above the earlier expectations of 6% to 8%, driven by accelerating AI adoption and robust data centre demand.

- PC refresh cycle to support client solutions group (CSG). According to IDC, global PC shipments rose around 9.4% YoY in 3Q25, aided by the Windows 10 end-of-support refresh and the rise of AI-enabled PCs. Dell’s CSG revenue edged up 1% YoY to US$12.5bn, with commercial demand up 2%, offsetting a 7% drop in consumer sales. As enterprises upgrade devices ahead of the Windows 11 transition and adopt AI-integrated PCs, Dell is positioned to capture incremental growth and margin recovery in its CSG revenue.

- 2Q26 results. Revenue rose 19% YoY to a record of US$29.8bn and non-GAAP diluted EPS of US$2.32, up 19% YoY. During the first half, the company shipped US$10bn of AI solutions, surpassing all shipments in FY25. Its infrastructure solutions group and client solutions group rose 44% YoY to US$16.8bn and 1% YoY to US$12.5bn respectively. In Q3, it expects revenue to be between US$26.5bn and US$27.5bn, up 11% YoY, and non-GAAP diluted EPS to be US$2.45 at the midpoint, up 11%. For FY26, it expects revenue to be between US$105.0bn and US$109.0bn, up 12% YoY, and non-GAAP diluted EPS to be US$9.55 at the midpoint, up 17%. Dell also expects compounded annual revenue growth between 7% and 9% for the next four years, up from its prior view of 3% to 4%. Dell expects long-term compounded annual revenue growth of 11% to 14% for the infrastructure solutions group, above earlier expectations of 6% to 8% and continues to expect revenue growth of 2% to 3% for its client solutions group, which includes personal computers.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Add Alibaba Group (9988 HK) at HKD$160.