Bumitama Agri Ltd. produces CPO and PK, with its oil palm plantations located in Indonesia. The Company’s primary business activities are cultivating and harvesting our oil palm trees, processing FFB from its oil palm plantations, its plasma plantations and third parties into CPO and PK, and selling CPO and PK in Indonesia.

Structural demand boost from Indonesia’s biodiesel expansion. Indonesia’s planned B50 biodiesel mandate by 2H26, building on the success of B40, represents a major policy tailwind that could tighten domestic CPO supply by as much as 4 million tonnes. This initiative enhances energy security, reduces reliance on imported diesel, and structurally underpins palm oil consumption, potentially supporting a re-rating of plantation stocks. While execution risks remain, such as subsidy funding and biodiesel blending capacity, Bumitama is well positioned to benefit from the supply-demand tightening, particularly as global trade dynamics ease with the WTO ruling in Indonesia’s favour and the upcoming EU CEPA trade pact.

Navigating short-term volatility with operational discipline. Despite structural positives, near-term palm oil prices remain exposed to seasonal demand shifts, high inventories, and fluctuations in crude oil markets. Malaysian CPO futures recently softened below MYR 4,600/ton as inventories climbed to a near two-year high, while Indian imports could moderate after festive-driven peaks. Nonetheless, Bumitama’s yield optimization, disciplined replanting strategy and cost efficiency provide buffers against cyclical pressures, enabling it to sustain competitive margins and capitalize on longer-term growth anchored by supportive export trends and biofuel-driven demand.

Palm oil spot price

(Source: Bloomberg)

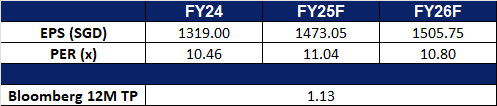

Strong earnings momentum driven by pricing power. Bumitama Agri delivered an impressive 1H25, with net profit soaring 47.8% YoY to Rp1.27tn on the back of firmer palm oil prices. Revenue climbed 28.2% to Rp9.74tn, despite marginally lower CPO sales volumes, underscoring the group’s ability to capitalise on favourable pricing dynamics. The palm kernel segment was the standout, with revenue more than doubling as higher prices and volume growth lifted profitability. EPS surged to Rp730 compared to Rp494 delivered in 1H24), enabling management to hike the interim dividend threefold to S$0.0363 per share, signalling strong cash generation and confidence in balance sheet strength.

1H25 results review. Revenue increased 28.2% YoY to Rp9.74tn from Rp7.6tn in the year-ago period. Net profit rose 47.8% to Rp1.27tn (S$100.2mn) for 1H25, above the Rp856.8bn in 1H24, translating to EPS of Rp730 in 1H25 from Rp494 in the period before.

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

Expanding renewable footprint. Sembcorp’s S$246mn acquisition of ReNew Sun Bright in India strengthens its position as one of the largest foreign renewable energy players in the country, raising its gross capacity in India to 6.9GW. With India targeting 500GW of clean energy by 2030, this deal provides Sembcorp long-term contracted cash flows under a 25-year power purchase agreement, diversifying earnings while reducing reliance on more volatile merchant markets.

Long-term revenue visibility. In Oman, Sembcorp Salalah secured a new 10-year power and water purchase agreement commencing 2027, ensuring continued offtake for its Salalah Independent Water and Power Plant. This underpins stable cash flows, reinforces strategic ties with the government procurer and adds visibility beyond the expiry of its current 15-year contract, supporting revenue resilience.

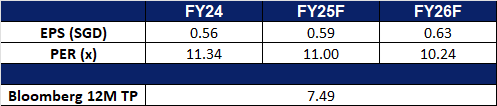

1H25 financial results. Group net profit was S$491mn, comparable to 1H24 net profit of S$489mn. Group net profit after exceptional items was S$536mn, 1% lower than S$543mn in 1H24. The Group delivered an interim dividend of 9.0 Scents per ordinary share.

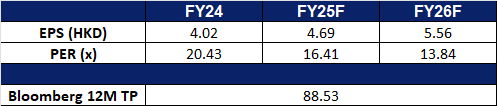

Market consensus

(Source: Bloomberg)

Kuaishou Technology (1024 HK): AI commercialisation to spur growth

BUY Entry – 83 Target – 95 Stop Loss – 77

Kuaishou Technology is an investment holding company mainly engaged in the operation of content communities and social platforms. The Company mainly provides live streaming services, online marketing services and other services. The online marketing solutions include advertising services, Kuaishou fans headline services and other marketing services. Other services include e-commerce, online games and other value-added services. The Company also develops new businesses, such as local services, Kwai Hire and Ideal Housing. The Company operates its business in domestic market and overseas markets.

International expansion via AI companions. Kuaishou is diversifying beyond China with the launch of FantaSay, its Singapore-based AI companion app. With over 500,000 downloads since launch, the app taps into a growing global market for virtual companions, where user willingness to pay for personalized, often adult-themed, interactions is high. Leveraging its proprietary AI agent platform, Keloi, Kuaishou is positioned to monetize NSFW avatars in overseas markets, capturing share in a segment where one-third of the top apps already originate from China.

AI video synergies driving growth. Kuaishou’s deep video corpus and real-time engagement data give it a unique moat in AI model training, supporting Kling AI’s monetization, recommendation accuracy and cost efficiency. The rapid scaling of Kling AI, with quarterly revenues surpassing RMB250mn, highlights how AI video generation is becoming a key growth driver alongside advertising and e-commerce, where AI tools are raising click-through rates and merchant conversion efficiency.

Capital returns signal sustainable AI-driven cash flows. Management declared Kuaishou’s first-ever dividend of HK$0.46 per share, about HK$2.0bn in total, alongside RMB 101.9bn of available funds and prior buybacks, underscoring confidence in AI-driven revenue diversification and long-term cash generation.

2Q25 earnings. Revenue rose by 13.1% YoY to RMB35.0bn in 2Q25, net profit rose RMB4.0bn to RMB4.9bn, adjusted net profit was RMB5.6bn with a 16.0% adjusted net margin and gross margin was 55.7%. Average DAUs rose 3.4% to 408.9mn and MAUs increased 3.3% to 714.8mn. H1 revenue of RMB67.7bn, up 12.0 percent, net profit was RMB8.9bn and adjusted net profit was RMB10.2bn.

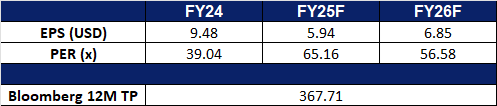

Market consensus.

(Source: Bloomberg)

China Longyuan Power Group Corp Ltd (916 HK): Policy backed growth

China Longyuan Power Group Corp Ltd is a China-based comprehensive power generation company that mainly develops and operates new energy sources. The Company operates four segments. Wind Power segment constructs, manages and operates wind power plants and produces electricity for sale to power grid companies. Thermal Power segment constructs, manages and operates coal-fired power plants and produces electricity for sale to power grid companies. Photovoltaic Power Generation segment constructs, manages and operates photovoltaic power plants and produces electricity for sale to external power grid companies. All Other segment is principally engaged in the manufacture and sale of power generation equipment, provision of consulting services, provision of maintenance and training services to wind power companies and other renewable energy generation and sales.

Structural growth tailwinds. China Longyuan Power stands to benefit from the unprecedented acceleration in renewable energy, as China added more solar and wind capacity in 1H25 than the rest of the world combined, helping renewables overtake coal for the first time in global electricity history. With Beijing targeting a sixfold increase in wind and solar by 2030 and aiming to reduce emissions 7%-10% by 2035, Longyuan’s dominant wind and solar portfolio positions it as a key beneficiary of national and global decarbonization.

Supply chain and policy benefits. China retains more than 90% control over key renewable supply chains such as solar PV and rare-earth elements used in wind turbines, underscoring Longyuan’s competitive cost advantage compared to international peers. The company also enjoys long-term policy support from China’s climate commitments, including carbon trading and mandatory renewable quotas, reinforcing predictable demand and grid priority.

Solid recovery in power generation. Longyuan Power reported notable growth in renewable generation in July. Wind output rose 6.4% YoY, while photovoltaic (PV) generation more than doubled (+106% YoY). Total power generation increased 9.4% MoM, marking a clear rebound from weaker production in 2Q25. The strong July performance highlights the company’s successful shift toward renewables and its positioning to capture peak summer demand.

1H25 earnings. Revenue rose by 3.1% YoY to RMB15.66bn in 1H25, compared to RMB15.19bn in 1H24. Net profit fell by 10.8% to RMB4.17bn in 1H25, compared to RMB4.68bn in 1H24. Basis EPS fell to 42.10 RMB cents in 1H25, compared to 48.74 RMB cents in 1H24.

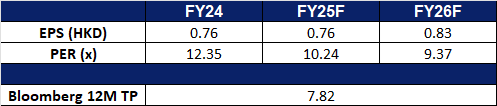

Market consensus.

(Source: Bloomberg)

IREN Ltd. (IREN US): Scaling AI infrastructure business

BUY Entry – 60 Target – 70 Stop Loss – 55

IREN Limited operates as a renewable energy company. The Company owns and manages next-generation data centers powered by renewable energy optimized for bitcoin mining, AI cloud services, and other power-dense compute. IREN serves clients in Australia.

Transition to AI infrastructure growth. IREN is transitioning from a Bitcoin miner to an AI infrastructure company, currently holding contracts for 23,000 GPUs, with a goal of achieving $500 million in operating revenue by Q1 2026. The company has signed customer contracts covering 11,000 GPUs, nearly half of its equipment, ensuring approximately $225 million in annual recurring revenue, providing strong visibility for recent AI cloud revenues.

Scale and renewable energy advantage. IREN has secured 2,910 MW of renewable power in British Columbia and Texas, with a capacity of over 100,000 GPUs. As demand for AI computing surges, IREN combines scale with sustainability, making it a cost-competitive supplier of green AI infrastructure, attracting ESG-focused hyperscale and enterprise clients.

Financial momentum and capital flexibility. The company issued $875 million in convertible notes, which increases dilution risk, but these funds support accelerated GPU expansion, aiming for revenue returns within two years on the new Blackwell GPU deployment.

4Q25 results. Total revenue was US$187.3mn, and adjusted EBITDA was US$121.9mn, rising from US$144.8mn and US$82.9mn in Q3, respectively. For FY25, revenue reached US$501mn, with net income increasing from US$28.9mn in FY24 to a record US$86.9mn. The company is nearing US$1.25bn in total annualized revenue. By December 2025, annualized revenue from Bitcoin mining is expected to exceed US$1bn, while annualized revenue from 10,900 NVIDIA GPUs for AI cloud is projected to be between US$200mn and US$250mn.

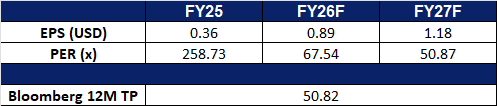

Market consensus

(Source: Bloomberg)

Coinbase Global Inc. (COIN US): Advancing crypto policy and regulation

Coinbase Global, Inc. provides financial solutions. The Company offers platform to buy and sell cryptocurrencies. Coinbase Global serves clients worldwide.

Record institutional inflows into cryptocurrency ETFs. Close to US$6bn in record inflows into cryptocurrency ETFs, led by the U.S., highlights a surge in institutional adoption, directly boosting trading volumes on the Coinbase platform. As the primary U.S. listed exchange and custodian with US$425bn in assets under management, Coinbase is poised to capture this liquidity cycle, with Bitcoin reaching record highs acting as a catalyst for sustained trading volumes and fees.

Tokenization opportunities and regulatory advantage. Coinbase’s pursuit of a national trust bank license, combined with its engagement with the SEC on tokenized securities, places it at the forefront of the projected tokenization boom expected to reach approximately US$2tn by 2030. With tokenized ETFs, equities, and stablecoins gaining traction globally, Coinbase’s credibility and regulatory engagement provide a moat as traditional finance migrates on-chain.

Ecosystem expansion amid policy tailwinds. Backed by pro-crypto U.S. policies and clarity on stablecoins, Coinbase is expanding into custody, tokenization, staking, lending and payments. Strategic partnerships with banks like JPMorgan and PNC reinforce its role as the institutional gateway to digital assets.

2Q25 results. Total revenue was US$1.5bn, down 26% QoQ. Transaction revenue was US$764mn, down 39% QoQ. Subscription and services revenue was US$656mn, down 6% QoQ. Net income was US$1.4bn and adjusted EBITDA was US$512mn. The company expects July transaction revenue to be approximately US$360mn, with Q3 subscription and services revenue estimated to be between US$665mn and US$745mn, benefiting from higher average crypto prices and stablecoin revenue. Q3 transaction expenses are expected to be in the mid-teens as a percentage of net revenue.

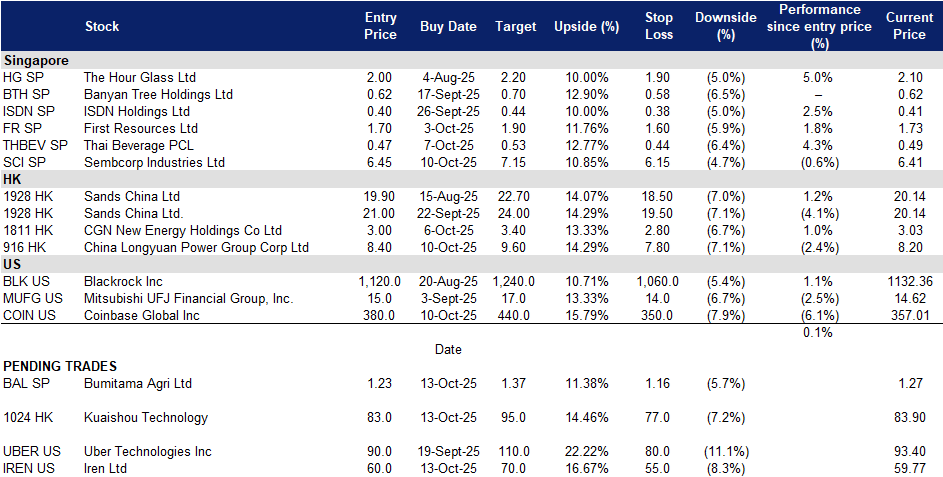

Trading Dashboard Update: Take profit on MP Materials Corp (MP US) at US$80. Add Sembcorp Industries Ltd (SCI SP) at S$6.45, China Longyuan Power Group Corp Ltd (916 HK) at HK$8.40 and Coinbase Global Inc (COIN US) at US$380. Stop loss on Seatrium Ltd (STM SP) at S$2.25, Xiaomi Corp (1810 HK) at HK$52 and Lyft Inc (LYFT US) at US$20.

(Source: Bloomberg)

(Source: Bloomberg)

(Source: Bloomberg)

(Source: Bloomberg)